The market, as is its wont, has commenced its annual fit of pique. The S&P 500, that meticulously constructed monument to collective optimism and despair, has shed a respectable 5% of its illusory peak. Geopolitics, a perpetually agitated beast, sniffs at the borders of reason, and economic uncertainty, a fog as thick as Moscow in November, descends. The usual panics, naturally. One anticipates a correction, perhaps a rather more substantial one. But history, that tiresome pedagogue, reminds us that even the most dramatic declines are merely pauses in the relentless climb. Opportunities, therefore, for those with the fortitude to ignore the shrieks of the panicked masses.

And so, I acquired a stake in Sea Limited. Not, mind you, out of any particular faith in the inherent goodness of capitalism, but because the numbers, viewed through a cynical lens, suggested a temporary…misunderstanding. A Singaporean entity, it operates in the realms of commerce, digital amusements, and, most curiously, the lending of money – a practice that has, historically, rarely concluded well for anyone involved. The stock, you see, has suffered a rather undignified tumble – a decline of 56% from its recent high. A bargain, perhaps, for a vulture with a functioning calculator.

A Trifecta of Modernity

Sea owns Shopee, a platform where Southeast Asians procure goods with a zeal that borders on the religious. Thirteen point nine billion orders in 2025, they claim. A staggering sum. One imagines warehouses overflowing with trinkets and necessities, all destined for a fleeting moment of satisfaction. They are, of course, extracting revenue from the advertisements that plague the platform, and improving the logistics – a necessary evil in any commercial undertaking. Faster delivery, they boast. As if speed were a virtue in a world already hurtling towards oblivion.

Then there is Monee, their digital lending arm. A curious venture. They provide capital to merchants on Shopee, fueling their ambitions. And they offer ‘buy now, pay later’ schemes to consumers – a modern iteration of the age-old trap of debt. Thirty-seven million borrowers, they claim. A vast army of hopefuls, each burdened by the weight of their desires. Eighty percent growth in loans. One shudders to contemplate the eventual reckoning. It reminds one of a certain bureaucrat, perpetually signing promissory notes with a flourish.

And finally, Garena, their entertainment division. Responsible for such digital ephemera as Free Fire, Call of Duty: Mobile, and EA Sports FC. Games, in essence, designed to distract the masses from the inherent absurdity of existence. Six hundred and thirty-three million users, they claim. A captive audience, willingly surrendering their time and attention to the flickering screen. A modern opiate, perhaps, more effective than anything concocted in the laboratories of the East.

The Accelerating Momentum

Sea generated $22.9 billion in revenue in 2025. A record, naturally. A 36.4% increase year-over-year. The numbers, one must admit, are…impressive. Here is the breakdown, for those who insist on quantifying the unquantifiable:

| Segment | 2025 Revenue | Year-Over-Year Growth |

|---|---|---|

| E-commerce (Shopee) | $16.6 billion | 33.4% |

| Digital financial services (Monee) | $3.8 billion | 60.1% |

| Digital entertainment (Garena) | $2.4 billion | 26.1% |

The e-commerce business, while generating the lion’s share of revenue, operates on notoriously thin margins. A race to the bottom, if you will. But they have made progress, achieving $880.6 million in adjusted EBITDA. A substantial sum, though one suspects it is built on a foundation of…optimism. The digital financial services and entertainment segments, however, generate significantly more EBITDA on less revenue. A diversified portfolio, they call it. A hedge against the inevitable chaos.

Overall, Sea delivered $1.6 billion in net income. A remarkable achievement, even by the standards of modern accounting. A testament to the power of…well, one hesitates to use the word ‘innovation.’ Let us simply say, a clever manipulation of numbers.

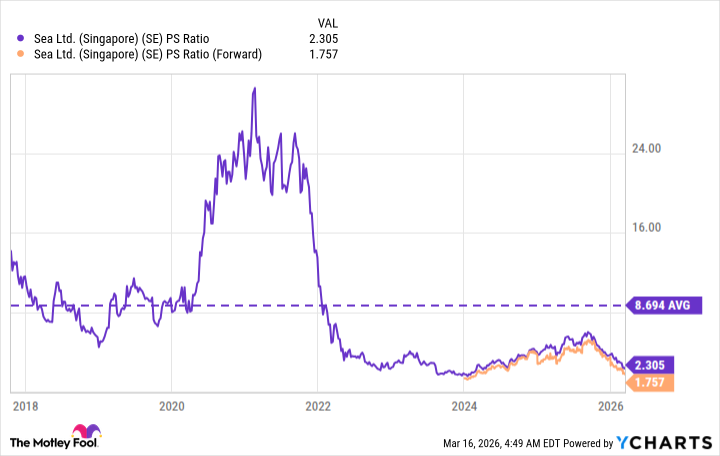

A Question of Valuation

Following the aforementioned decline, Sea stock appears…undervalued. Its price-to-sales ratio is a mere 2.3. A significant discount to its long-term average of 8.7. Wall Street, in its infinite wisdom, predicts revenue of $28.9 billion in 2026. Which places the forward P/S ratio at a paltry 1.7. A bargain, one might say. Though, of course, bargains often conceal hidden flaws.

The stock would need to soar by almost 400% to reach its long-term average P/S ratio. An unlikely scenario, perhaps. But one should never underestimate the power of collective delusion.

Finally, Sea possesses a remarkably strong balance sheet. $11.1 billion in cash and equivalents, against a mere $510 million in debt. A fortress of liquidity. A cushion against the inevitable storm. A comforting thought, in a world teetering on the brink of…well, let us not dwell on that.

Read More

- Silver Rate Forecast

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Brent Oil Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Games That Faced Bans in Countries Over Political Themes

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

2026-03-19 15:33