The current excitement surrounding artificial intelligence has, predictably, caused a ripple effect through the semiconductor industry. Nvidia, Broadcom, and Taiwan Semiconductor Manufacturing have seen their stock prices swell to frankly improbable levels – each now comfortably a member of the so-called “trillion-dollar club.” One ought to remember that such valuations are built on expectation, a notoriously unreliable foundation.

The hyperscalers – Microsoft, Alphabet, Amazon, Meta Platforms, and OpenAI – are, of course, pouring capital into infrastructure. Initially, the focus was on graphics processing units. Now, however, the demand is shifting, or rather, broadening. High-bandwidth memory (HBM) is becoming increasingly crucial, and the companies that can supply it are finding themselves in a position of considerable leverage.

Sandisk, spun off from Western Digital approximately a year ago, has experienced a surge in its share price – a 1,750% increase, to be precise. Such a rapid ascent invites skepticism. The question is not merely whether this growth is sustainable, but whether it was ever justified in the first place. Investors, it seems, are often more interested in the story than the substance.

The Source of the Surge

The headlines are filled with pronouncements of breakthroughs in generative AI. Large language models, touted as the future of everything from search queries to software coding, are becoming embedded in enterprise workflows. The practical value of many of these applications remains debatable, but that does not deter the investors. AI, it is claimed, is more than a productivity enhancer; it’s a revolution. Such language should always be met with a degree of caution.

The development of robotics, autonomous systems, and advancements in life sciences are, undeniably, driving demand for increased processing power. As these next-generation services begin to scale, the need for supporting infrastructure – data centers, GPUs, and, crucially, HBM – is intensifying. Sandisk, it appears, is benefiting from this trend, having successfully adapted its memory solutions from consumer electronics to meet the demands of enterprise workloads.

Is the Opportunity Already Past?

Understanding the importance of the HBM market is one thing; determining whether Sandisk’s share price accurately reflects its future prospects is another. Wall Street, it seems, is generally bullish, projecting revenue of $15.5 billion for the current fiscal year, with earnings per share of $39.76. Forecasts for next year are even more optimistic: sales are expected to grow 65% to $25.5 billion, with EPS doubling to $81. These figures, however, are projections, not guarantees.

The memory chip market is cyclical, and such optimistic forecasts should be viewed with a critical eye. Nevertheless, Sandisk’s business appears to have considerable upside potential. The crucial question remains: has the stock already priced in that potential?

Where Might Sandisk Be Headed?

Assessing a company’s investment prospects solely on the basis of its stock price is a flawed approach. Sandisk’s recent surge might suggest that the opportunity has passed, but focusing solely on percentage gains reveals little about the underlying valuation. The market, after all, is driven by sentiment as much as by fundamentals.

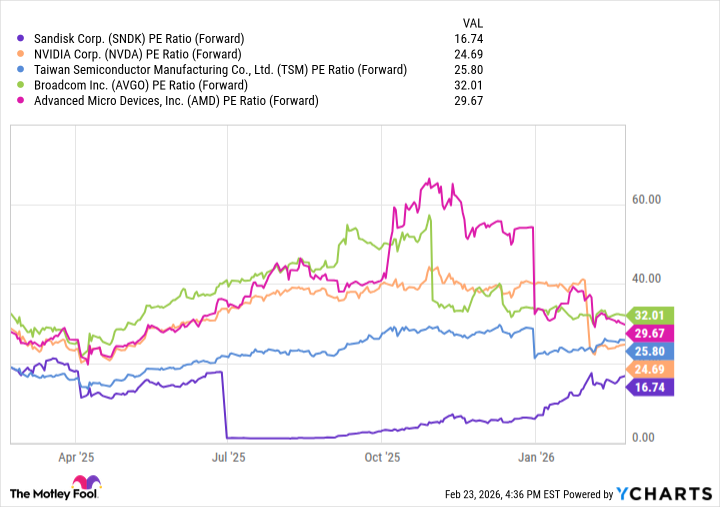

As the chart above illustrates, Sandisk is currently valued at a discount relative to other leading AI chip stocks, based on forward price-to-earnings multiples. This does not necessarily mean that the stock is undervalued; it simply means that the market is currently assigning a lower multiple to Sandisk’s earnings.

Nvidia, Advanced Micro Devices, Broadcom, and Taiwan Semiconductor Manufacturing are all different companies with different roles in the AI chip value chain. They are also more diversified than Sandisk, making them less vulnerable to cyclical headwinds and changes in hyperscaler budget allocations. This diversification comes at a cost, of course, but it also provides a degree of stability.

Nevertheless, Sandisk’s valuation, relative to its growth profile, appears muted. Reaching a forward earnings multiple of 20 is realistic, given its role in the HBM market. Should the company trade in that range, shares could climb to roughly $800, implying a 20% upside from current levels. This is a speculative projection, but it highlights the potential for further appreciation.

Predicting future price targets is a fool’s errand. However, given Wall Street’s bullish outlook and the company’s modest valuation, Sandisk appears well-positioned to continue rallying. The current enthusiasm, while perhaps excessive, is not entirely unfounded. It remains to be seen whether the company can deliver on its promise, but the conditions are, at least, favorable. And in the current climate, that is a significant advantage.

Read More

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 15 Films That Were Shot Entirely on Phones

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The Best Directors of 2025

- Brent Oil Forecast

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

2026-02-27 00:34