![]()

Right, so Oracle. Shares took a bit of a tumble – nearly halved in six months, if you’re keeping score. Everyone was getting their knickers in a twist about AI infrastructure spending. Honestly, it’s always something, isn’t it? Like we expect tech companies to just not invest in the future. Anyway, they recently posted some decent numbers – a little shot in the arm, they called it. Which, let’s be real, is what we all live for, isn’t it? A little positive reinforcement. So, the question is, is this a blip, or could we actually see some proper growth? Because, frankly, I’ve got bills to pay.

Oracle’s Smart(ish) Infrastructure Strategy

They’re building cloud infrastructure at a frankly alarming rate. Customers are throwing money at them to run AI workloads. The backlog? $553 billion. It’s… a lot. A 325% jump in remaining performance obligations? That’s not a typo. Revenue only increased 22%, which, okay, a bit of a lag, but let’s not dwell. They’re essentially promising a lot and delivering… eventually. It’s a bit like promising yourself you’ll start that diet tomorrow.

Now, this requires funding. Naturally. Fifty billion dollars worth, to be precise. They’ve already snagged thirty billion through debt and convertible stock. It’s a bit of a gamble, borrowing to build something you hope people will use. It’s what I do every time I order takeout, to be honest. But Oracle has a cunning plan. They’re asking customers to essentially fund the build themselves – “bring your own hardware,” they call it. It’s like asking your friends to pay for the renovations on your house. Bold. And possibly brilliant. They’ve already secured $29 billion in contracts using this model. Cloud infrastructure revenue jumped 84% last quarter to $4.9 billion. Not bad. Not bad at all.

The idea is that this keeps the cash flow from completely imploding while they build out this AI empire. It’s a bit like juggling chainsaws. Risky, but if you pull it off, you look like a genius. And if you don’t… well, let’s not think about that. The demand for AI compute is insane right now, and Oracle is positioning itself to capitalize. It’s a simple equation, really. More data centers, more revenue, more… everything.

So, How Much Upside Are We Talking?

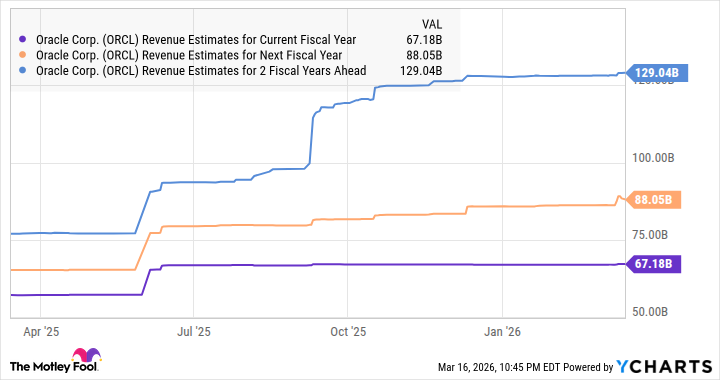

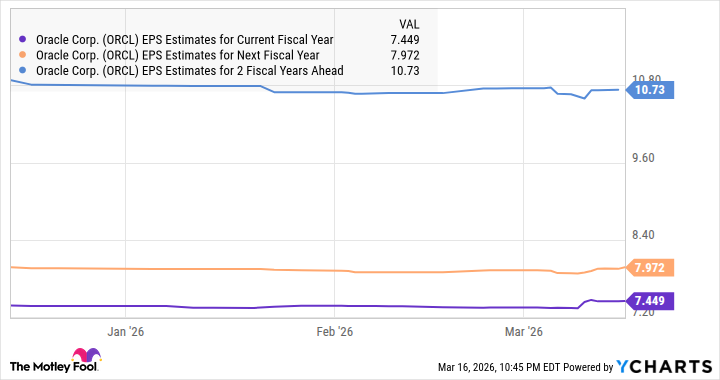

They’re predicting $67 billion in revenue for fiscal 2026. Then, a jump to $90 billion in 2027. That’s a 34% increase. They’re hinting at even bigger things in 2028. It’s… ambitious. But let’s play along. If Oracle can actually deliver on these projections, and earnings hit $10.73 per share in 2028, and the stock trades at 24.5 times earnings (which is pretty standard for a tech company obsessed with growth), then we’re looking at a potential 68% jump in the stock price. To $263. It’s enough to make a girl consider early retirement, frankly.

And, let’s be honest, it’s currently trading at only 19 times forward earnings. Which, in this market, is practically a steal. It’s not a guaranteed win, of course. Nothing ever is. But it’s a calculated gamble. And I, for one, am always up for a little bit of risk. Especially if it means I can finally afford that yacht. Don’t judge. A girl can dream.

All this makes Oracle a top AI stock to buy right now. Just don’t come crying to me if it all goes south.

Read More

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 15 Films That Were Shot Entirely on Phones

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The Best Directors of 2025

- Brent Oil Forecast

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

2026-03-20 17:24