The market, you see, is a curious beast. It occasionally throws perfectly good companies overboard, mistaking temporary turbulence for a fatal shipwreck. Microsoft, currently experiencing a bit of a nautical disagreement with the waves, is one such case. Down nearly thirty percent from its recent zenith? A trifle, I assure you. A mere opportunity for those of us with a penchant for calculated speculation.

To suggest a doubling of the stock in three years isn’t prophecy, dear reader, but a rather straightforward application of logic – and a healthy disregard for prevailing panic. The gentleman who waits, as they say, doesn’t necessarily inherit the earth, but he often acquires a rather attractive portfolio.

The Artificial Intelligence Ruse and the Cloud’s True Potential

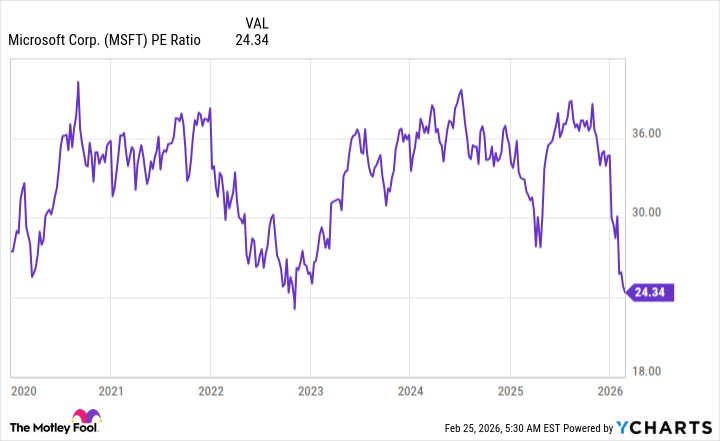

This current obsession with Artificial Intelligence… it’s a bit like the gold rush, isn’t it? Everyone scrambling for a piece of something shiny, without quite understanding what it is or if it’s even real gold. Investors, understandably anxious about the return on all this generative AI spending, are behaving like pigeons in a hailstorm. Microsoft, caught in the flurry, has been unfairly buffeted. The stock now trades at a valuation unseen since the depths of a previous, equally irrational downturn.

Historically, Microsoft has enjoyed a P/E multiple of around 33. A perfectly reasonable figure for a company that, despite the current anxieties, remains remarkably robust. To assume this will not return is to assume the market has suddenly developed a taste for austerity. A most unlikely proposition, wouldn’t you agree?

Azure: The Real Engine of Growth (and a Cloud of Opportunity)

Microsoft, unlike some of its competitors, isn’t attempting to build its own artificial intelligence behemoth. A wise strategy, in my estimation. It’s instead positioning itself as a sort of digital bazaar, a marketplace where developers can acquire the tools they need, regardless of origin. A neutral stance, you see, allows one to profit from the general madness without being consumed by it. It’s a bit like running the saloon during a gold rush – far more lucrative than digging for the gold itself.

Their investment in OpenAI, while a bit of a wild card, is a pleasant bonus. A potential windfall, if you will. But we shall largely ignore it in our calculations. Predicting the future is a fool’s errand, and I, for one, prefer to deal with demonstrable realities.

The true engine of Microsoft’s growth, however, is Azure, their cloud computing division. This is where the real money is being made. The demand for cloud computing, driven by the insatiable appetite for AI workloads, is immense. In the last quarter, Azure revenue rose by 39%. A figure that could have been even higher, had management not been so… cautious. A little more audacity, a little less internal tinkering, and we might be looking at even more impressive numbers.

Analysts predict revenue growth of 16% for fiscal 2026 and 15% for fiscal 2027. Reasonable projections, I believe. Earnings per share are expected to reach $19.02 by 2027. If Microsoft sustains this growth, earnings could reach $23.45 in three years. Applying that 33 times earnings multiple, we arrive at a price of $774 per share. Currently trading around $390? A rather compelling opportunity, wouldn’t you say? Most stocks double in seven years, not three. This, my friends, is not a prediction, but a simple observation of value.

Read More

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Persona 5: The Phantom X Relativity’s Labyrinth – All coin locations and puzzle solutions

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- How to Unlock Stellar Blade’s Secret Dev Room & Ocean String Outfit

- Brent Oil Forecast

- ‘Super Mario Galaxy’ Trailer Launches: Chris Pratt, Jack Black, Anya Taylor-Joy, Charlie Day Return for 2026 Sequel

2026-03-01 00:42