![]()

The semiconductor realm, a modern-day fever dream of progress and speculation, has indeed offered succor to the discerning investor of late. The relentless hunger of those constructing these digital cathedrals – the hyperscalers, as they are called – for ever more chips, is a spectacle both fascinating and… unsettling. It suggests a need that may never be truly quenched. But let us not be swept away by the current; let us observe where the true value lies, where the yield might blossom amidst the silicon and the shadows.

One notes, with a certain melancholy, that the masses flock to the obvious – Nvidia, AMD – chasing the fleeting illusion of exponential growth. Their valuations, already stretched thin, resemble towers built on sand. A mere correction, a whisper of doubt, could bring them crashing down. They are preoccupied with the spectacle of artificial intelligence, while we, the more contemplative among us, seek the substance.

Micron Technology, however, presents a different case. A surge of 255% since mid-August? Such exuberance is rarely born of pure logic. Yet, beneath the surface, there lies a quiet strength, a fundamental necessity. Memory and storage – the very foundations upon which these digital empires are built. It is not glamorous, no, but it is essential. And in the essential, we often find the most enduring value.

Let us delve, then, into the labyrinthine complexities of this market, and attempt to discern whether this surge is merely a fleeting mania, or a harbinger of something more substantial.

The HBM Void: How Large is the Appetite?

Micron’s management speaks of a $35 billion market for high-bandwidth memory in 2025, swelling to $100 billion by the decade’s end. These figures, of course, are mere projections, dreams woven from data. But the underlying trend is undeniable: the demand for memory is increasing, and increasing rapidly. The question is not if it will grow, but how – and who will ultimately reap the greatest benefit.

The field is dominated by a triumvirate: Samsung, SK Hynix, and Micron. A dangerous oligopoly, perhaps? Or simply the natural order of a highly specialized industry? One cannot help but ponder the moral implications of such concentrated power. But let us remain focused on the financial realities. Competition, while fierce, is not necessarily a detriment. It forces innovation, efficiency… and ultimately, higher returns for those who can navigate the treacherous currents.

What Does Wall Street Foresee? The Illusion of Certainty.

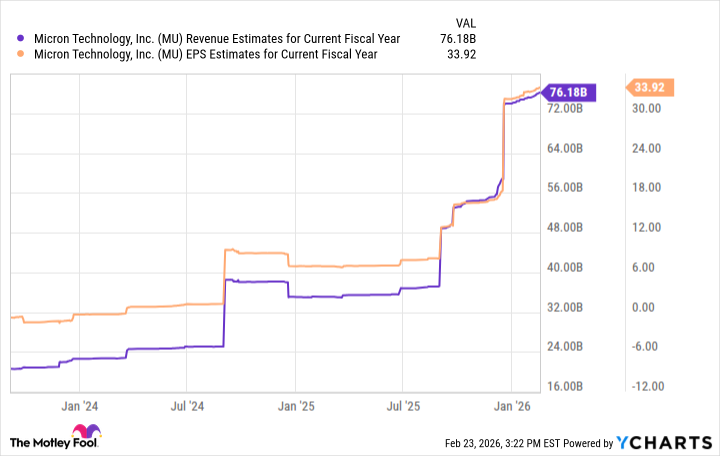

The whispers from Wall Street speak of a revenue forecast of $76 billion for Micron in fiscal 2026, a staggering 103% increase. Earnings per share are expected to quadruple. Such optimism is… unnerving. Analysts, like prophets of old, often mistake the present for the future. They extrapolate trends, ignoring the inherent unpredictability of human behavior – and the market, of course, is a mirror of our collective anxieties and aspirations.

Yet, the underlying logic is sound. A shortage of dynamic random access memory (DRAM) and NAND solutions, coupled with the insatiable demand from big tech, allows Micron to command pricing power. It is a temporary reprieve, perhaps, a fleeting moment of dominance. But in the relentless struggle for profit, even a moment can be enough.

The End of 2026: A Glimpse into the Abyss?

Even after its impressive ascent, Micron trades at a modest price-to-earnings multiple of 12.3. A pittance, compared to the lofty valuations of its peers. Nvidia, AMD, Taiwan Semiconductor Manufacturing, Broadcom – all command multiples ranging from 25 to 37. The disparity is… striking. It suggests that the market has yet to fully appreciate Micron’s potential.

If Micron were to trade at a more reasonable multiple of 20, its shares would soar to $660, implying a 57% upside. A substantial return, to be sure. But it is not merely the potential for capital appreciation that attracts me. It is the underlying stability, the quiet strength, the promise of a consistent yield.

Each semiconductor company, of course, occupies a different niche, faces different challenges. But the macro takeaway is clear: Micron is undervalued, overlooked, and ripe for exploitation. For those with the patience to navigate the turbulent waters, the rewards could be substantial. I foresee continued valuation expansion throughout 2026, driven by the relentless acceleration of AI infrastructure investments. And in that expansion, a yielding abyss, perhaps, but one worth contemplating.

Read More

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Brent Oil Forecast

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

2026-02-27 15:53