The present state of the market offers a peculiar spectacle. Though headline figures suggest unprecedented heights, a closer inspection reveals a disquieting unevenness. Several of the larger technology companies, those entities once considered impervious to downturn, now trade noticeably below their recent peaks. Such opportunities, when available, are rarely accompanied by rational sentiment. The current climate, where optimism persists despite these valuations, is therefore worth noting.

Three stocks warrant consideration: Microsoft (MSFT 2.17%), Amazon (AMZN +1.04%), and Meta Platforms (META 1.29%). Each has experienced a recent decline, and a pragmatic assessment suggests they may represent reasonable, if not exceptional, purchases at present prices.

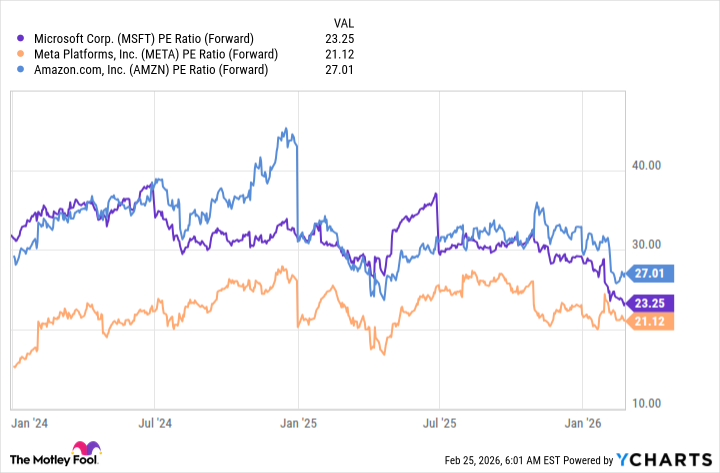

Recent Valuation Adjustments

All three companies attained record valuations within the past year, before succumbing to a corrective phase in 2026. Microsoft has suffered the most significant decline, currently trading nearly 30% below its previous high. Meta and Amazon exhibit similar, though slightly less pronounced, reductions, each down approximately 20%.

Historical patterns suggest these established firms often experience unpredictable rallies. Consequently, acquiring shares of these entities at a discount, when such opportunities arise, has frequently proven advantageous. The present moment appears to fit this pattern. Each stock, while not necessarily cheap in absolute terms, trades at a forward price-to-earnings ratio that deserves scrutiny.

Microsoft, in particular, appears relatively undervalued compared to its recent performance. At 23 times forward earnings, it is not substantially different from the broader market, as represented by the S&P 500, which trades at 21.9 times. A more relevant comparison might be with the technology-heavy Nasdaq-100 index, currently at 25.3 times. Regardless, Microsoft’s stock, given its position, warrants consideration.

Meta Platforms presents an even more compelling valuation, trading at 21.1 times forward earnings. This places it below the S&P 500’s multiple, a surprising discrepancy given Meta’s current growth trajectory.

Amazon, trading at 27 times forward earnings, historically commands a premium valuation, and this remains the case. However, its current price is comparable to the lows experienced during the 2025 tariff-related sell-off, which ultimately proved to be a profitable entry point. A similar rationale applies today. Should the market regain favor with these three companies, a recovery is likely.

These three stocks, in my assessment, represent reasonable investments at present. Prudent investors should consider taking advantage of these prices while they persist.

Read More

- Games That Faced Bans in Countries Over Political Themes

- Gold Rate Forecast

- Silver Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- The Best Directors of 2025

- Brent Oil Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

2026-02-28 08:02