The pronouncements of those who have accumulated substantial capital are, naturally, observed. Not for any inherent wisdom, perhaps, but because their errors are, at least, executed on a scale sufficient to be instructive. It is a peculiar form of education, learning from the wreckage of others’ fortunes. Each quarter, a ritualistic declaration of holdings is made to the Securities and Exchange Commission – Form 13F – a document less about transparency and more about the bureaucratic necessity of acknowledging what is, in any case, already known. We sift through these filings, not in the hope of revelation, but to chart the subtle shifts in the prevailing despair.

Ole Andreas Halvorsen, a custodian of $37 billion at Viking Global Investors, has recently adjusted his portfolio. A diversified collection, naturally, spanning the predictable spectrum of industries – technology, finance, healthcare – a testament to the futility of seeking true isolation in a fundamentally interconnected system. He emerged, some years ago, from the now-legendary Tiger Management, a breeding ground for those who believe they can predict the unpredictable. He is now categorized as one of the “Tiger cubs,” a designation which implies both lineage and, inevitably, a degree of inherited delusion.

His recent acquisitions are not, strictly speaking, investments in growth, but rather wagers on the possibility of avoiding further decay. Two entities, in particular, warrant our attention, not for their promise of prosperity, but for the curious fact that they have, thus far, managed to postpone their inevitable collapse.

Leaders in Their Designated Decline

Halvorsen has dispersed funds across various sectors, a gesture of diversification that merely serves to distribute the risk, not eliminate it. Two purchases stand out: Carnival, the world’s largest cruise operator, and UnitedHealth Group, a dominant force in the American health insurance landscape. Both are, in their respective domains, leaders – not in innovation or progress, but in the art of maintaining a precarious equilibrium.

The details, as if such precision matters in the face of entropy:

- 14,061,827 shares of Carnival, constituting just over 1.1% of the portfolio – a rounding error in the grand scheme of things, yet a significant commitment to a vessel perpetually on the verge of sinking.

- 1,197,273 shares of UnitedHealth, representing 1% of the holdings – a stake in a system designed to profit from illness, a particularly cynical form of investment.

Let us examine each, not with optimism, but with a detached curiosity.

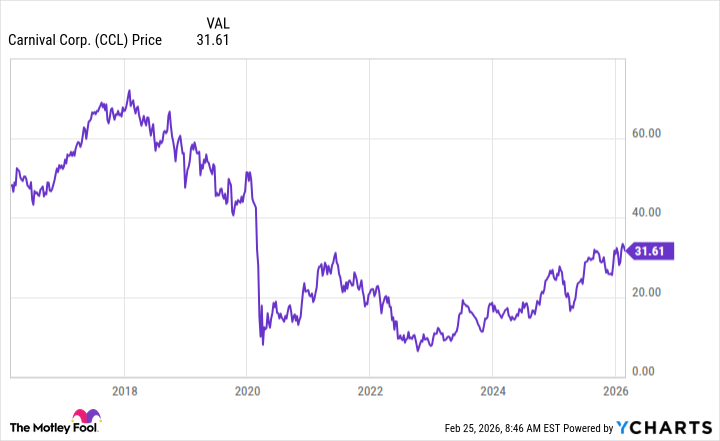

Carnival has experienced a temporary reprieve, climbing over the past year, yet remaining far below its former heights. The company briefly flirted with insolvency during the pandemic, its vast fleet rendered immobile. It has since managed to restart its engines, but the journey remains fraught with peril.

Revenue and operating income have reached record levels, but this is merely a temporary surge, a final gasp before the inevitable decline. Demand for cruises remains high, driven by a desperate need for escapism, a futile attempt to outrun the anxieties of modern existence.

A Low-Risk Exercise in Prolonged Suffering

Carnival is, admittedly, further along its path to recovery than many, but it remains burdened by debt. The shares are reasonably priced, but this is merely a reflection of the market’s tacit acknowledgment of its precarious position. It is a less risky bet, perhaps, but only in the sense that a slow descent is preferable to a sudden plunge.

UnitedHealth, on the other hand, is still grappling with its own internal contradictions. Higher-than-predicted healthcare costs, coupled with a probe into its billing practices, have weighed on earnings and depressed the stock price. The company has responded with cost-cutting measures and price adjustments, a futile attempt to patch a fundamentally flawed system. It now speaks of “focus and execution,” as if bureaucratic jargon can somehow alter the laws of economics.

The shares trade at a modest valuation, but this is merely a consequence of the market’s growing disillusionment. It is a cheap stock, but cheapness does not necessarily equate to value.

Should one follow Halvorsen into these troubled waters? The answer, predictably, depends on one’s tolerance for uncertainty. Carnival is further along its path to oblivion, a relatively safe bet for the cautious investor. UnitedHealth, however, is still in the midst of its struggle, a more speculative wager for those willing to accept a higher degree of risk. It is a gamble, of course, but in the grand scheme of things, are any of us not merely rolling the dice?

Read More

- Silver Rate Forecast

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Brent Oil Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Games That Faced Bans in Countries Over Political Themes

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

2026-02-27 13:23