For six decades, Warren Buffett has been the guiding spirit of Berkshire Hathaway, a titan amongst holding companies. Now, the mantle has passed to Greg Abel. It is not merely a change in leadership, but a transfer of responsibility, a burden of expectation. The numbers, of course, are staggering – a compound annual return of 19.7%, eclipsing the S&P 500’s more modest gains. A thousand dollars invested in 1965 bloomed into an almost unconscionable $48.4 million by the close of 2025. Yet, figures alone tell a hollow story. They fail to capture the peculiar alchemy of Buffett’s success, the intuitive grasp of value, the almost preternatural ability to discern opportunity amidst the chaos. One wonders, can such a gift be…inherited?

Berkshire’s evolution is itself a curious tale. From the near-moribund textile manufacturer it once was, it has risen – or perhaps, been reborn – as a behemoth, a conglomerate of such scale that its very existence seems to defy the laws of economic gravity. A trillion-dollar empire built not on innovation, but on…prudence. A strange virtue in our age of reckless abandon. It owns insurance companies, railways, utilities…a vast network of enterprises, each humming with the quiet energy of accumulated wealth. And, of course, the stock portfolio. Apple, a particularly weighty obsession, representing a significant portion of the whole. The gradual shedding of Apple shares, a pragmatic decision, perhaps, but one tinged with a subtle melancholy. To relinquish even a portion of such a lucrative holding feels…almost like a confession of fallibility.

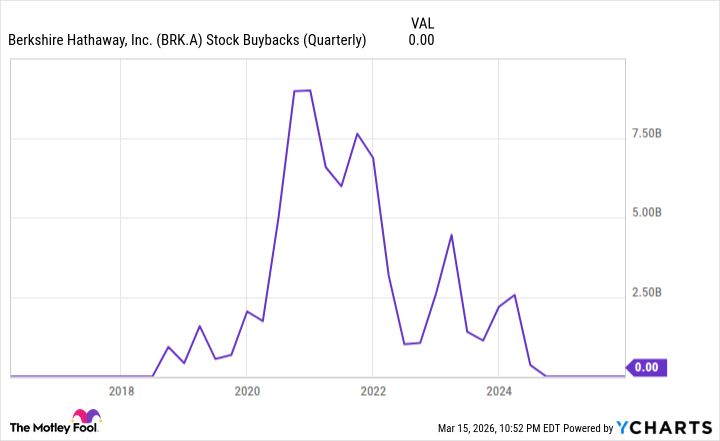

The accumulation of capital, however, presents its own peculiar anxieties. What does one do with such a vast fortune? To simply hoard it feels…morally suspect. To invest it requires a constant vigilance, a ceaseless search for opportunities worthy of such a substantial commitment. And so, Buffett, in his final years, turned to stock buybacks. A curious practice, really. Returning capital to shareholders, rather than reinvesting it in growth. A tacit acknowledgement, perhaps, that the landscape of opportunity is…shrinking? Abel has now resumed this practice, a signal, perhaps, that the search for truly compelling investments continues to prove…fruitless. The sheer scale of Berkshire’s cash reserves – $373 billion – is almost…terrifying. So much potential, yet so little to apply it to. Nearly 477 companies in the S&P 500 are worth less than this single sum. The irony is almost unbearable.

Buybacks, then, are not merely a financial maneuver, but a psychological one. A way to alleviate the pressure, to quiet the anxieties that come with such immense wealth. They offer a degree of control, a way to manipulate the market, to bolster share prices. And yet, even this feels…incomplete. A temporary reprieve from the inevitable uncertainties of the future. Buffett understood this, of course. He understood that even the most carefully constructed financial empire is ultimately built on sand. He has bequeathed not just a fortune to Abel, but a profound sense of responsibility. A weight that will undoubtedly grow heavier with each passing year. The question is not whether Abel will succeed, but whether he can bear the burden. Whether any man can, in the face of such…infinite possibilities, and infinite risks.

Abel’s decision to resume buybacks is a logical step, a pragmatic response to the current market conditions. It will, undoubtedly, please shareholders. But it does not resolve the underlying dilemma. The true test of his leadership will not be measured in quarterly earnings or stock prices, but in his ability to navigate the treacherous currents of the global economy, to preserve the legacy of Berkshire Hathaway, and to find meaning in the relentless pursuit of wealth. A task, I suspect, that will consume him entirely.

Read More

- Silver Rate Forecast

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Brent Oil Forecast

- 15 Films That Were Shot Entirely on Phones

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Games That Faced Bans in Countries Over Political Themes

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

2026-03-19 15:03