Ten American enterprises now stand as monuments to scale, their valuations exceeding a trillion dollars. Yet, only three – Nvidia, Alphabet, and Apple – have breached the rarefied atmosphere of a three-trillion-dollar market capitalization. Microsoft, a long-standing member of this exclusive company, has recently retreated, a reminder that even the most formidable positions are subject to the currents of the market.

One observes, with a degree of quiet anticipation, the trajectory of Amazon. It seems, to this observer, that the company is poised to join this select group. Artificial intelligence, that restless spirit of our age, is indeed fueling growth within Amazon Web Services, its cloud division. And the e-commerce business, once characterized by a relentless pursuit of volume, is exhibiting a welcome increase in profitability, a testament to the efficiencies now woven into its logistical network.

Currently valued at $2.25 trillion, Amazon presents, to a discerning eye, a potential return of at least 33% should it ascend to the $3 trillion mark. A consideration, perhaps, for those who seek not merely growth, but a measured and sustainable return.

The Expanding Realm of Amazon Web Services

Amazon Web Services, the dominant force in cloud computing, began as a simple provider of digital storage. It has since blossomed into a comprehensive ecosystem, offering a multitude of solutions for businesses navigating the complexities of the digital age. Its current focus on artificial intelligence, with an expanding portfolio of computing capacity, foundational models, and specialized software, is particularly noteworthy.

The development of artificial intelligence, naturally, resides within the confines of data centers, those modern cathedrals of computation, powered by advanced chips from suppliers like Nvidia. Amazon, while a significant customer of Nvidia, has wisely chosen to cultivate its own capabilities in chip design. The Trainium series, particularly the latest iteration, Trainium2, offers a compelling price-performance ratio, and the recently launched Trainium3 promises a further, and welcome, improvement. It is a prudent strategy, to rely not solely on others, but to forge one’s own path.

AWS Bedrock serves as a conduit, granting businesses access to pre-built foundational models, accelerating their development of artificial intelligence applications. It hosts models from esteemed third parties, alongside Amazon’s own Nova family, which offers a degree of customization seldom found elsewhere. This flexibility is crucial for building highly specialized applications and, increasingly, intelligent agents.

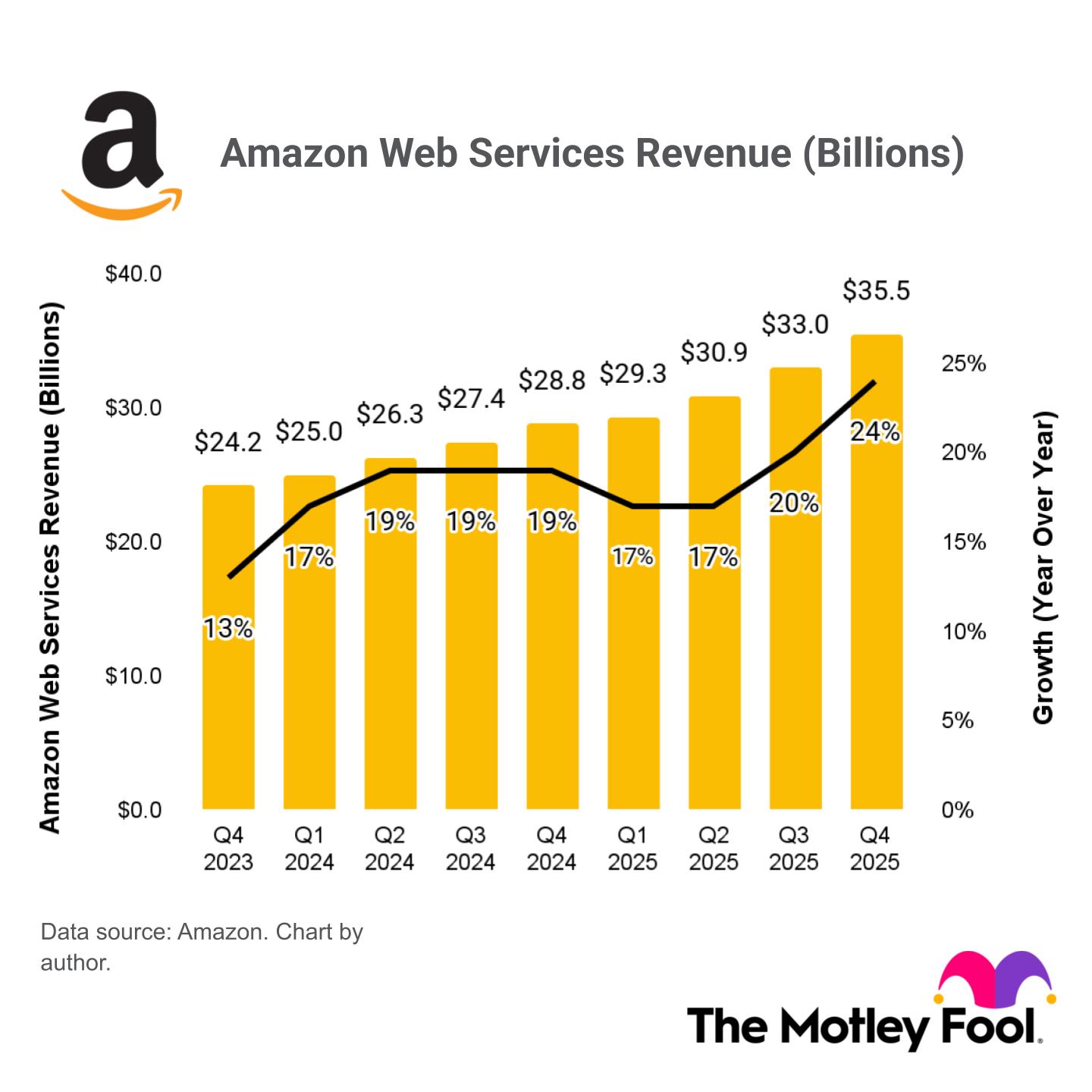

During 2025, AWS generated $128.7 billion in revenue, with momentum building steadily throughout the year. Revenue growth accelerated from 17% in the first quarter to 24% by the fourth, largely driven by the burgeoning demand for artificial intelligence services.

Perhaps even more significant is the staggering $244 billion in orders currently awaiting fulfillment, a testament to the platform’s success and the need for expanded infrastructure. Amazon plans to invest $200 billion in 2026 to address this demand, a considerable undertaking, but one that seems justified by the potential rewards.

The E-Commerce Business: A Quiet Transformation

While Amazon Web Services contributes a significant portion to the company’s overall revenue – 18% of the $716.9 billion total in the last fiscal year – it is responsible for a disproportionate share of the company’s operating income – 57% of the $79.9 billion total. The e-commerce business, while remaining Amazon’s largest revenue source, historically operated on thin margins, prioritizing volume over immediate profit.

However, in recent years, Amazon has undertaken a significant overhaul of its U.S. logistics network, shortening delivery distances and reducing fulfillment costs. In 2025, the company delivered a record 8 billion packages to Prime members in America either on the same day or the next, a 30% increase year over year. A quiet triumph, perhaps, but one that speaks volumes about the effectiveness of these improvements.

Combined with the growth from AWS, these efficiency gains are driving a significant increase in Amazon’s overall profitability. The company reported $77.6 billion in net income for 2025, a 31% increase over the prior year, translating to earnings of $7.17 per share. A respectable performance, indeed.

A Path to Three Trillion Dollars

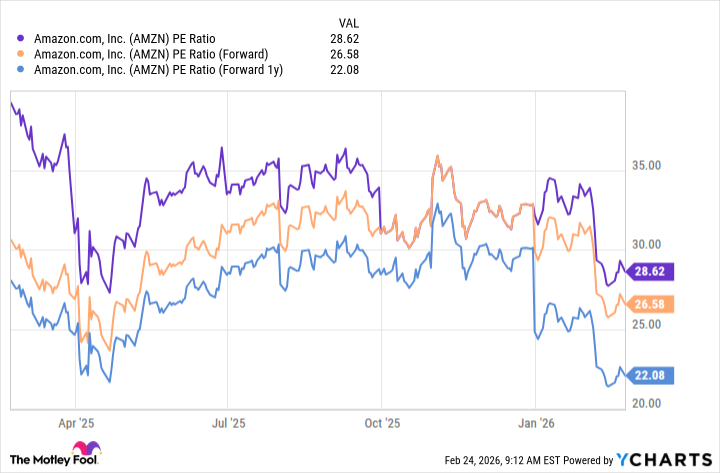

Recent market fluctuations have caused Amazon’s stock to retreat by 19% from its all-time high. This, combined with the company’s strong earnings growth in 2025, has resulted in a price-to-earnings ratio of just 28.6, a discount compared to the Nasdaq-100 index, which trades at a P/E ratio of 31.6. Amazon, therefore, appears undervalued relative to its peers.

Furthermore, Wall Street analysts anticipate Amazon’s earnings to grow to $7.75 per share in 2026, and $9.39 per share in 2027. This places the stock at forward P/E ratios of 26.6 and 22.1, respectively.

In essence, if these estimates prove accurate, Amazon’s stock would need to increase by 29.4% by the end of 2027 merely to maintain its current P/E ratio of 28.6. This alone would push its market capitalization to $2.85 trillion. However, should Amazon’s stock trade in line with the Nasdaq-100’s P/E ratio of 31.6, its valuation would soar to $3.14 trillion.

Considering Amazon’s P/E ratio exceeded 35 just six months ago, such an outcome appears entirely plausible. As a result, Amazon could indeed join the exclusive $3 trillion club within the next two years. A measured ascent, perhaps, but a significant one nonetheless.

Read More

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Brent Oil Forecast

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

2026-02-27 02:32