Now, about this Nvidia – a name on every tongue, and a price that’d make a banker blush. They say it’s the biggest in the market, and that’s true enough, but a big horse can still stumble, you see. Folks are fretting, whispering about whether this company is built on solid ground, or just a puff of smoke and mirrors. Seems these ‘hyperscalers’ – a fancy name for fellas who build enormous calculating machines – are spending a king’s ransom on these data centers, and Nvidia’s been collecting a goodly portion of it. Some reckon that’s a precarious position, like building a castle on a sandbar.

But is it, truly? Or is this a chance to get in on the ground floor of something… substantial? Let’s unravel this a bit, shall we?

The Spending Ain’t Slowing Down, Not By a Long Shot

These investors, they worry about the spending drying up. But I’ll tell you, it’s more likely to rain than for every one of these hyperscalers to suddenly decide they don’t need more computing power. It’s a peculiar situation, really. Underspending is the real danger. Imagine a railroad baron deciding he doesn’t need any more track! Preposterous! If they hold back, they’ll be left in the dust. If they all spend too much? Well, they’ll all be equally soaked in the downpour, won’t they? A shared folly is still a folly, mind you, but a less lonely one.

Now, Nvidia itself projects these data centers will require a staggering $3 to $4 trillion annually. Sounds like a sum fit for a sultan, doesn’t it? But when you consider the scale of things, it’s not so outlandish. These four big hyperscalers alone are planning to drop some $650 billion this year. And that’s just the beginning. Don’t forget fellas like OpenAI or Oracle, who are also tossing around fortunes. China’s getting in on the game, too, and Europe, well, they’ve been a bit slow to the dance, but I suspect they’ll be waltzing soon enough when they see what everyone else is building.

And here’s a thought: these hyperscalers aren’t shrinking anytime soon. Their cash flows could easily double in the next five years, giving them even more coin to spend. That means even bigger budgets for these data centers. It’s a virtuous cycle, if you will, though I always have a healthy suspicion of anything described as ‘virtuous’ when money’s involved.

What’s more, a good deal of these budgets are currently tied up in construction and land. Building these data centers isn’t like snapping your fingers. It takes time. But that means more money will flow toward the actual chips – Nvidia’s bread and butter – in the years to come. It’s a slow burn, but a promising one. Yet, the market seems to think this growth will just… stop. As if progress has a deadline.

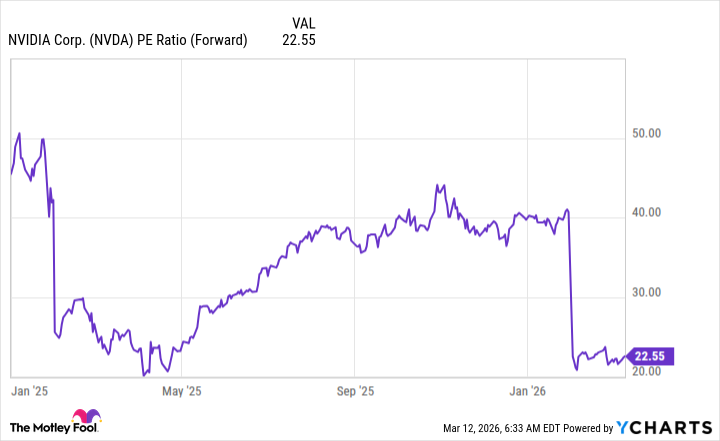

At 22.6 times forward earnings, Nvidia is priced as if it’s going to have a good year, and then… that’s it. As if the world will suddenly lose interest in calculating things! That’s a mighty short-sighted view, if you ask me. Growth is likely to continue well into the next decade, and beyond. That makes Nvidia a buy, a downright sensible investment, and those who hesitate may find themselves left behind, watching the train pull away.

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- 20 Best TV Shows Featuring All-White Casts You Should See

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- The Best Directors of 2025

- Gold Rate Forecast

- Palantir and Tesla: A Tale of Two Stocks

- How to rank up with Tuvalkane – Soulframe

2026-03-17 04:02