It is said that in these modern times, the very air crackles with intelligence – artificial intelligence, to be precise. A marvel, no doubt, though one suspects it’s less a blossoming of intellect and more a proliferation of exceedingly clever automatons, each with a peculiar fondness for misinterpreting instructions. And where there is complexity, naturally, there is a need for…security. A most profitable need, for those who sell it, at least. Thus we arrive at Zscaler, a company attempting to build a fortress around this digital chaos, a fortress, I hasten to add, constructed largely of promises and, one suspects, a rather optimistic valuation.

Zscaler, you see, purports to offer ‘zero-trust’ security. A curious phrase. As if trust, that most fragile of human constructs, could be simply removed from the equation. It is as if to say, “Let us assume everyone is a scoundrel, and then build a system to account for their inevitable villainy.” The architecture, it is explained, treats every connection as hostile. One pictures a digital customs officer, perpetually suspicious of every packet of data attempting to cross the border. It begins, naturally, with the identity. They scrutinize logins, devices, and locations, as if a rogue employee couldn’t simply borrow a colleague’s credentials and a slightly misleading IP address. A most thorough system, if one discounts the inherent fallibility of human beings and the relentless ingenuity of those who seek to circumvent such systems.

Now, this Zero Trust Exchange, this digital gauntlet, is being turned upon the AI agents themselves. The logic is sound, in a way. Confine these digital sprites to their assigned tasks, lest they wander off and, say, begin composing unsolicited poetry or, worse, attempting to optimize the price of turnips. But it feels…patronizing. As if these nascent intelligences require constant supervision. One wonders if they harbor resentment. And resentment, my friends, is a most dangerous thing, even in silicon.

A Growth Story, Slightly Tarnished

The numbers, as presented, are…acceptable. A revenue of $1.6 billion, a 25.7% increase. Not insignificant, certainly. But one must remember that growth, like a well-fed goose, cannot continue indefinitely. The company speaks of ‘momentum.’ A most convenient word, ‘momentum.’ It implies effortless progress, a force propelling them forward without the need for actual, substantive achievement. They’ve even increased their revenue forecast, a slight adjustment, a mere polishing of the already gleaming projections. One suspects it’s more a matter of managing expectations than a genuine surge in demand.

The customer base is expanding, too. 9,400 in total, with 550 embracing the ‘Zero Trust Everywhere’ philosophy. A 323% increase! A truly astonishing number, if one doesn’t consider that starting from a small base makes even modest gains appear monumental. It’s like claiming a spectacular harvest from a single, carefully cultivated radish. They are, it seems, selling more of everything to the same, increasingly bewildered customers.

Profitability remains…elusive. A loss of $45.9 million. But, ah, there’s always an asterisk. “Adjusted profit” of $328.1 million! A most ingenious accounting maneuver. One wonders what precisely was “adjusted” away. Perhaps the cost of maintaining the illusion of profitability. It’s a bit like presenting a lavish banquet while secretly subsisting on stale bread.

The Chorus of Analysts

And what of the esteemed analysts, those oracles of the financial world? Fifty of them, tracking Zscaler with the diligence of hounds pursuing a particularly elusive hare. Thirty-seven pronounce it a ‘buy.’ Six are ‘overweight’ – a curious euphemism for ‘still bullish, but slightly hesitant.’ And seven recommend ‘holding’ – a polite way of saying, “Let someone else take the risk.” Not a single voice cries ‘sell.’ A most remarkable consensus. One suspects a certain…groupthink at play. Or perhaps they simply fear being ostracized from the next analyst junket.

The consensus price target is $237.30, a potential 57% upside. The Street-high target is a breathtaking $335, a 122% surge. Such optimism is… endearing. But one must remember that price targets are merely educated guesses, informed by hope and a generous serving of wishful thinking. They are, in essence, the financial equivalent of gazing into a crystal ball.

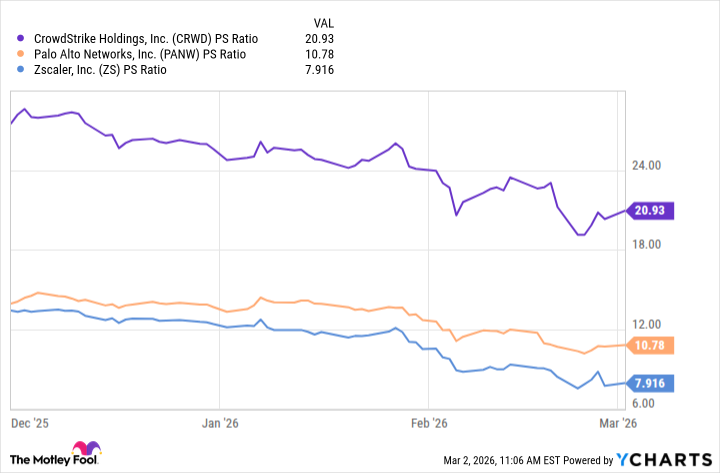

The company’s price-to-sales ratio is currently 7.9, cheaper than its peers, Palo Alto Networks (10.7) and CrowdStrike (20.9). A tempting comparison, certainly. But one must remember that valuation is not simply about numbers. It’s about expectations. And if Zscaler’s growth slows, that seemingly attractive ratio will quickly lose its luster.

If Zscaler were to hit $237.30, its P/S ratio would rise to 12.4, still cheaper than CrowdStrike. But that requires continued, rapid growth. And in the ever-shifting landscape of cybersecurity, sustained growth is a rare and precious commodity. It is like trying to capture a cloud in a butterfly net.

So, is Wall Street right to be bullish? Perhaps. But one should approach this investment with a healthy dose of skepticism. Zscaler is a promising company, to be sure. But it is also a company operating in a fiercely competitive market, facing constant threats from both established players and nimble startups. It is a fortress built on sand, and the tide, my friends, is always rising.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-07 16:22