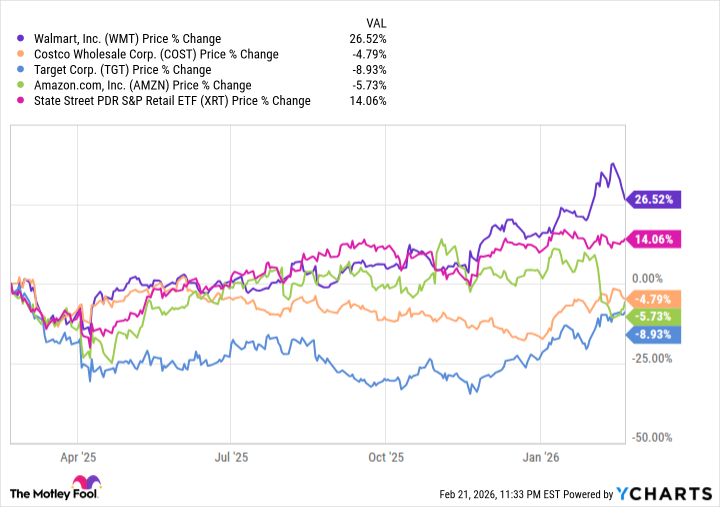

The numbers tell a story, of course. Twenty-seven percent gain for Walmart (WMT 0.54%) in the last year. A quiet strength, while others – Costco Wholesale (down 4.8%), Amazon (down 5.8%), even Target (down 8.9%) – have felt the shift of the winds. It’s a performance that stands apart, a solidness in a time when so much seems built on sand. The State Street SPDR S&P Retail ETF, a broad measure of the sector, has climbed 14%. Walmart isn’t merely keeping pace; it’s pulling ahead, a sturdy oak among saplings.

The question isn’t simply why this has happened, but whether it will endure. The markets are fickle, prone to sudden enthusiasms and equally swift disillusionments. But beneath the surface of quarterly reports and stock tickers, there’s a deeper current at work, a return to the fundamentals of value and necessity.

A Giant’s Slow Growth

It began, as so many things do, with a humble ambition in the Arkansas countryside. A single store, a promise of lower prices. Now, nearly 11,000 locations stretch across the land, employing over two million souls. It’s a scale that can feel impersonal, a vastness that can be intimidating. But behind the sheer size lies a relentless focus on efficiency, a mastery of the supply chain, a quiet determination to offer goods at prices ordinary families can afford. It’s not glamour, it’s practicality.

Growth at this scale isn’t explosive; it’s incremental, a steady accumulation of small gains. Yet, in the last quarter, Walmart reported revenue of $190.7 billion, up 5.6% year over year. Operating income rose by 10.8%, and adjusted earnings per share climbed 12.1%. For the full fiscal year, revenue reached $713.2 billion, with a gross profit rate of 24.2%. These aren’t the numbers of a company resting on its laurels; they’re the numbers of a company still striving, still building.

Fifty-three years of consecutive dividend increases – a testament to a commitment that runs deeper than quarterly earnings. It’s a stability that appeals to those who seek a safe harbor in turbulent times.

Beyond the Grocery Aisle

For decades, Walmart was defined by its groceries, its household goods, the necessities of daily life. But the world has changed, and Walmart has had to change with it. Amazon, the tech giant, has become the benchmark, the company to beat. It’s a different kind of giant, built on algorithms and logistics, on a promise of convenience and speed.

Walmart isn’t trying to become Amazon; it’s forging its own path. E-commerce sales rose 24% in the last quarter, and advertising income jumped 37%. Partnerships with Alphabet and OpenAI suggest a willingness to explore the possibilities of artificial intelligence. They’ve even developed “Sparky,” an AI shopping assistant, which reportedly increases average order value by 35%. It’s a gamble, a bet on the future, but it’s a necessary one.

Some worry about the price-to-earnings ratio of 45, higher than the tech-heavy Nasdaq-100‘s 32.7. It’s a fair concern, a reminder that no stock is immune to the forces of gravity. But for those who value steady dividends and believe in Walmart’s ability to adapt, this could be a worthwhile investment. It’s not about chasing the next quick fortune; it’s about building a solid foundation for the years to come.

The market, like the land, favors those who are patient, those who are willing to nurture and sustain. Walmart, for all its size and complexity, understands this simple truth.

Read More

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 15 Films That Were Shot Entirely on Phones

- Silver Rate Forecast

- Top 10 Coolest Things About Jared Leto

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

2026-02-25 22:33