Now, Walmart. A colossal presence, isn’t it? A retail behemoth that, for decades, has reliably delivered everything from sensible shoes to, well, just about anything else you can imagine. But the world, as anyone who’s attempted to assemble flat-pack furniture will tell you, is changing. And Walmart, like all the rest of us, is having to adapt. For years, they’ve been pouring money into the digital realm, building an online presence that, frankly, would have been unimaginable to Sam Walton. The question now, as 2026 looms, isn’t whether they can sell things online – they clearly can – but whether this digital expansion will actually translate into something tangible for those of us who like to see a return on our investments.

It’s a bit like building a very large extension onto your house. You spend a fortune, endure months of disruption, and then hope it adds value. Scale, in and of itself, isn’t the point. Anyone can build something big. The trick is building something that works, something that generates a decent return.

Closing the Gap, and What That Actually Means

Walmart has certainly narrowed the digital gap with Amazon, and that’s no small feat. They’ve cleverly leveraged their existing store network, turning each location into a miniature fulfillment center. It’s a bit like realizing you already had the perfect storage space for all your online orders – you just hadn’t thought of using it that way. It avoids the colossal expense of building an entirely new logistics operation from scratch. But here’s the rub: digital retail is a notoriously tricky business. Margins are often slimmer, returns are a constant headache, and the relentless pressure to offer discounts eats into profits. Growth, it turns out, doesn’t always equal prosperity.

The crucial question for 2026 isn’t simply whether Walmart can compete, but whether their omnichannel approach – the blending of online and physical stores – will actually deliver superior economics. If they can use their store base to reduce fulfillment costs and improve efficiency, then the investment makes sense. But if they’re just spending money to stay in the same place, well, that’s a different story entirely. It’s like running faster just to avoid falling behind – exhausting, and ultimately pointless.

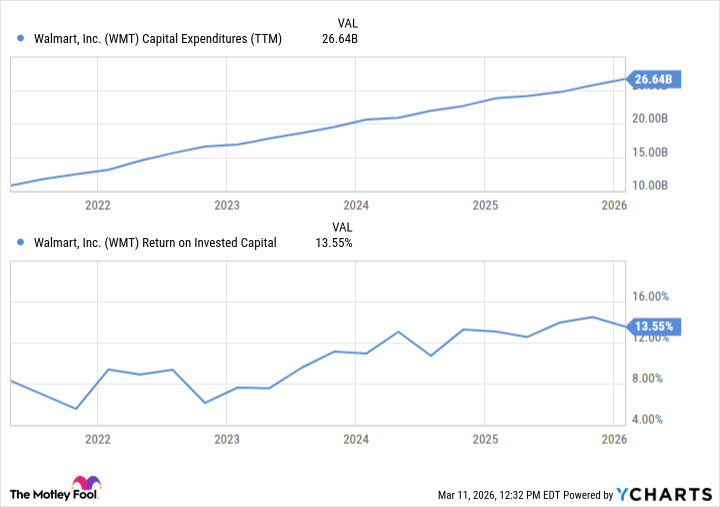

Spending to Improve – Or Just to Stay Put?

Maintaining a competitive edge in the digital world requires constant investment. Walmart is throwing money at technology and supply chain improvements, hoping to boost productivity and streamline operations. At a company the size of Walmart – with annual revenues exceeding $700 billion – even a modest increase in capital expenditures amounts to a staggering sum. They’re currently targeting around 3.5% of sales, which translates to a cool $24.5 billion. That’s enough to buy a small country, or at least a very large number of sensible shoes.

But here’s the thing: if return on invested capital remains flat while digital investment grows, shareholders are essentially funding maintenance, not improvement. It’s like endlessly renovating your kitchen without actually making it any more functional. A perfectly polished, yet ultimately unchanged, kitchen.

What Does Success Actually Look Like?

True digital success, as far as I’m concerned – and as a dividend hunter, I’m rather particular about these things – will manifest in three key areas:

- A gradual improvement in operating leverage – meaning that increases in revenue actually translate into increases in profit. A simple concept, yet surprisingly elusive.

- Stable or improving return on invested capital, despite all the digital spending. The money has to work for us, after all.

- Margin resilience, even in a fiercely competitive pricing environment. The ability to maintain profitability, even when everyone else is slashing prices.

If these conditions materialize, Walmart’s digital efforts could become a compounding advantage, a virtuous cycle of growth and profitability. Their physical footprint, combined with data and automation, could create a hybrid model that’s difficult for competitors to replicate. But if not, well, Walmart will remain a strong retailer, but one that’s investing heavily simply to hold its position. A bit like running on a treadmill – a lot of effort, but ultimately going nowhere.

For long-term investors, 2026 will be a pivotal year, a chance to clarify whether Walmart’s digital strategy deepens its competitive advantage or merely sustains it. And, naturally, a chance to see if those dividends keep flowing.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Top 20 Dinosaur Movies, Ranked

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- Silver Rate Forecast

- Gold Rate Forecast

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

2026-03-13 09:22