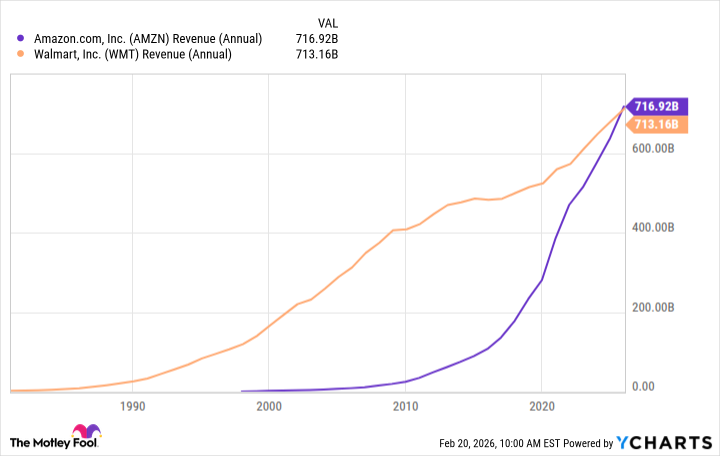

Walmart. A name synonymous with, well, practically everything. For decades, it’s been the retail behemoth, the place where one could find anything from aardvark food (if aardvarks were more popular) to zinc oxide. And, crucially, it reliably printed money. A truly impressive feat, when you consider the sheer logistical undertaking of moving that much stuff. But things, as they invariably do, are shifting. For the first time in a very long time – since 2009, to be precise – Amazon has edged ahead in the revenue stakes. $716.9 billion for Amazon, against Walmart’s $713.2 billion. It’s a difference of less than half a percent, mind you, but in the world of multi-billion-dollar corporations, that’s rather like being slightly taller than the average giraffe.

Should One Be Alarmed?

Probably not. Amazon has been on a tear for some time, and its growth rate was always going to eventually overtake Walmart’s. It’s a bit like watching a cheetah race a tortoise. The tortoise is perfectly respectable, mind you, and will likely outlive the cheetah, but in a straight sprint… well, you get the idea. Walmart’s revenue still rose a respectable 4.7%, but Amazon managed a rather zippy 12.4%. It’s not a disaster for Walmart, just a gentle nudge that the retail landscape is evolving.

At Walmart’s scale, maintaining growth is a bit like trying to steer an ocean liner. It’s not exactly nimble. Smaller companies can pivot and zoom around, but Walmart is a vast, complex organism, and change happens at a more… deliberate pace. It’s a bit like trying to teach a walrus to tap dance. Possible, perhaps, but requiring a significant amount of patience and specialized instruction.

More Than Just Aisles and Price Tags

Walmart’s core business remains, unsurprisingly, selling things in stores. But they’ve been quietly expanding into other areas, and it’s beginning to pay off. Their membership program, Walmart+, is a direct competitor to Amazon Prime, and while it’s unlikely to ever match Prime’s scale (Prime seems to have a membership card for every man, woman, and child on the planet), it’s a solid attempt. And their advertising platform, Walmart Connect, is growing at a truly impressive rate. It’s the company’s fastest-growing segment, with revenue up 41% year-over-year. Who knew that people were so eager to see ads for discounted toilet paper?

But perhaps Walmart’s biggest advantage is its physical footprint. They have stores everywhere. This allows them to offer same-day delivery in about 95% of the United States, using their stores as mini-fulfillment centers. It’s a clever move, and it gives them a significant edge over Amazon, which relies more heavily on warehouses and delivery drivers. It’s a bit like having a network of secret agents strategically positioned throughout the country, ready to deliver your groceries at a moment’s notice.

It feels like Walmart is undergoing a genuine, if somewhat slow-motion, pivot. It’s a bit like watching a large ship carefully change course. It takes time, but when it finally does, it’s a rather impressive sight.

A Pricey Proposition

Now, let’s talk about the stock price. As of February 20th, Walmart is trading at around 41.3 times its projected earnings. That’s… not cheap. It’s no longer priced like a traditional retail stock; it’s priced like a high-growth tech company. In fact, only Tesla is more expensive (at a truly eye-watering 198.2 times earnings), and even Apple is comparatively reasonable at 30.7. It doesn’t mean Walmart isn’t a good long-term investment, but it’s worth remembering that a high price can sometimes limit upside potential, or at least make the stock a bit more volatile. It’s a bit like buying a rare stamp. It might be worth a fortune, but it’s also a bit nerve-wracking to keep it in a drawer.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- Gold Rate Forecast

- Building Agents That Learn and Improve Themselves

- 15 Films That Were Shot Entirely on Phones

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Games That Faced Bans in Countries Over Political Themes

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

2026-02-24 01:13