For nearly all of the last sixteen years, the U.S. stock market has operated on what could only be described as a relentless march-or perhaps a drunken stagger-towards the clouds. Aside from a brief sneeze called the COVID-19 crash, which evaporated faster than a magician’s rabbit, and the 2022 bear market, which lasted just shy of a quarter of a year, investors have been enjoying a prolonged party, convinced that the bull’s horns were fixed firmly in place.

This year, the major indices-namely the broad-based S&P 500 (^GSPC +0.54%), the growth-fueled Nasdaq Composite (^IXIC +0.65%), and the venerable Dow Jones Industrial Average (^DJI +0.61%)-charged to heights last seen only in stories told by Wall Street’s grandfathers. These ascents have been powered by artificial intelligence (a phrase that now sounds like a weather forecast), hopeful anticipation of lower interest rates (which, if you think about it, are just the economy’s way of begging for a loan), and corporate earnings that seemed to dance just above their actual worth with a will of their own.

Marketing gurus and day traders alike gaze skyward and whisper, “The limit,” not realizing they’re just one puff of bad news away from being the crew of the Titanic-just with more zeroes in their spreadsheets. Yet, as any discerning market watcher with a taste for history’s ghost stories must admit, the past has a way of sneaking up just as shadows lengthen at sunset.

While the stock market’s gains boast the highest average annual returns since the invention of financial instruments-more or less-the road to these treasures has been paved with potholes, collapsible bridges, and the occasional landmine. As these indices vicariously ascend toward valuation heights that would make Ponce de León’s explorer’s hat spin, the question remains: How long can the market keep defying gravity before gravity-or perhaps some unseen goblin-pulls the rug out?

To the untrained eye, Wall Street’s current valuation reflects a confidence so robust it could perhaps be mistaken for foolhardiness. The market’s valuation measures are trying to keep pace, attempting to justify the dizzying heights, almost as if they too are caught in the thrill of the climb. However, history offers a sobering warning: Just once since 1871 has Wall Street been this “pricier” than usual-an occasion marked by scars, tears, and lessons learned the hard way.

The Valuation Games of the Olden Days (And Why They Matter)

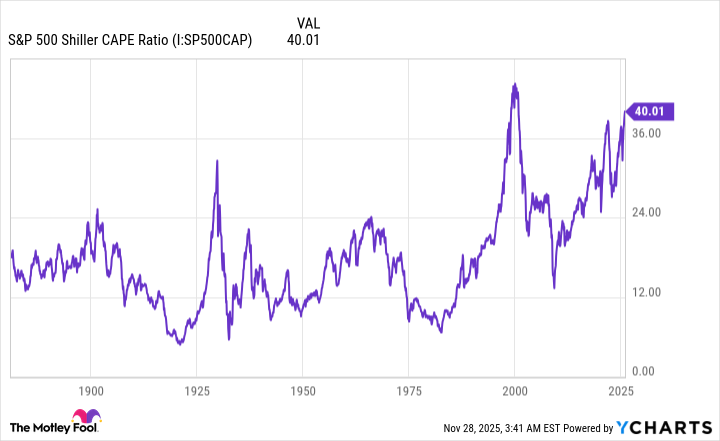

Before diving into the story of the Shiller Price-to-Earnings (P/E) ratio-also known as the cyclically adjusted P/E ratio, or CAPE, for those who enjoy tongue-twisters-the importance of context cannot be overstated. There exists no crystal ball, no magic amulet, no wizard who can predict short-term movements in stocks based solely on immediate data. Had such a device existed, it would now be hoarded in a vault as secure as Fort Knox and probably used to stockpile gold bars to fuel additional stock market schemes.

Yet, history-a mischievous old fellow-tends to rhyme, often whispering clues about the future through patterns and episodes. Some of these episodes, well-placed and carefully noted, become the forewarnings that keep market watchers awake at night, clutching their charts and muttering about cycles and crashes.

In the realm of valuation, everyone has its own yardstick-some prefer traditional measures, others are partial to the newest fad. Nonetheless, the Shiller P/E ratio stands somewhat apart, like the venerable wizard of valuation, based on a decade’s worth of inflation-adjusted earnings. Unlike the simplistic trailing P/E, which can be knocked askew by shocks-like the sudden appearance of a synthetic spider in a data center-the Shiller version remains relatively steady, a dependable if somewhat dull old lighthouse on the foggy coast of investing.

Back in the days when the internet was just a fancy word for a series of tubes, and civilizations hadn’t yet realized the infinite abundance of cat memes, the Shiller P/E was born in the late 1980s, but it was only back-tested to 1871. Over that impressive span, the average multiple sat around 17.31-until, of course, modernity and greed pushed that number skyward, much like a balloon tied to a doghouse during a summer picnic.

As of the last trading bell on November 26, the S&P 500’s Shiller P/E read a notably lofty 40.20, flirting dangerously close to the peak of 41.20 in late October during this current bullish saga. The last times we saw such exalted valuations-44.19 during the dot-com boom, or a few hundredths shy of 40 just before the 2022 crash-history was quick to remind us that such peaks tend to be followed by sharp descents.

In fact, since 1871, the Shiller P/E has cracked the 40 mark only twice-numbers that coincided with significant market corrections, ranging from the 1999 bubble to the pre-2022 overreach. And during most of these times, the indices switched from their upward tango to a downward slump, with declines ranging from 20% to the staggering 89% during the Great Depression-more or less the universe’s way of knocking the wind out of the inflated sails.

Based on the lessons of the past, the conclusion is inescapable: It’s not a question of “if” but “when” Wall Street’s indexes will endure a sizable tumble-an elevator ride down that no amount of financial engineering can prevent.

When the Market Gets Nervous, It Often Opens the Door for Steady Hands

Most investors aren’t exactly eager to see their portfolios shrink by 20% or more-an event that would turn any trader’s smile into a grimace. Emotions, those unruly gremlins of Wall Street, tend to push prices downward in a panic-an elevator plummeting without warning, whose doors are too slow to close.

Yet, as history demonstrates with the patience of a gardener tending an overgrown hedge, crashes and corrections tend to open a rare window-an opportunity for those who can resist the siren song of panic and plant their capital in fertile ground while the ground is trembling.

It must be acknowledged that Wall Street, in its infinite capacity for irony, prefers to zigzag rather than glide in a straight line. Corrections, bear markets, and the occasional catastrophic event are as much a part of its DNA as the urge to find the next big thing. No amount of Fed policy or legislative sorcery can guarantee immunity from these periodic bouts of chaos.

What is fascinating, however, is the stark contrast in the lifespan of these downturns versus the durations of bullish advances. Recent data from the sharp minds at Bespoke Investment Group remind us that, since the Great Depression, bear markets have rarely lasted beyond a mere nine and a half months, whereas bullish periods tend to stretch their legs for over three years. This longevity gap signals that patience, coupled with a dash of luck, can turn a market slump into a golden opportunity if one keeps calm and carries on.

While there’s no psychic device to pinpoint the exact moment the next downturn starts or ends, history-ever the wise old storyteller-confirms that trusting in the long game and pouncing during those inevitable dips can be the secret to turning market chaos into profit. Perhaps in the end, the best investors are those who understand that patience is, after all, the most undervalued asset of all. And so, the game continues, quieter and more patient than the noise suggests, promising that even in chaos, there is opportunity-if you’re willing to see it.

Read More

- Gold Rate Forecast

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

- 15 Films That Were Shot Entirely on Phones

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Biogen’s Jolly Good Showing

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

- Monster Hunter Stories 3 Complete Side Stories Guide & What Do They Unlock

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

2025-11-30 17:52