Recent surveys indicate a prevailing negative sentiment towards the current economic landscape, with approximately 72% of respondents expressing unfavorable views. A further 40% anticipate a deterioration in economic conditions over the coming year. While predictive accuracy remains elusive, historical valuation metrics suggest a heightened degree of vulnerability within equity markets.

Elevated Valuation Multiples: A Cause for Prudence

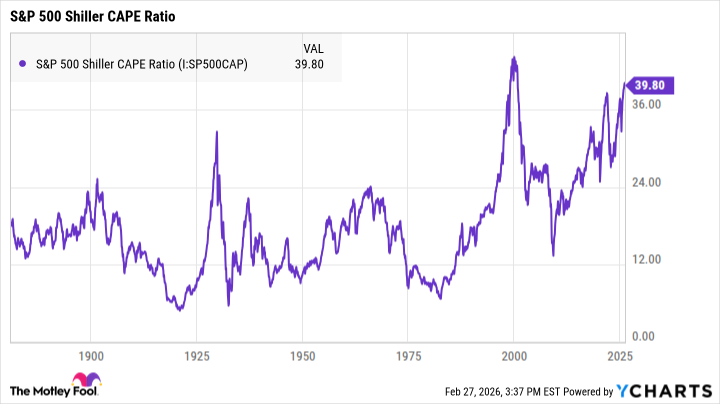

The Cyclically Adjusted Price-to-Earnings (CAPE) ratio, calculated using the S&P 500, currently stands at approximately 40. This represents a significant premium to its historical average of around 17, and approximates levels observed during the late stages of the 1999 technology bubble. Such elevated multiples suggest a diminished margin of safety for investors. The historical record demonstrates a tendency for market corrections following periods of extended valuation expansion.

The S&P 500 CAPE ratio reached a peak of 44 in 1999, preceding the dot-com correction. A subsequent peak was observed in late 2021, preceding the bear market experienced throughout much of 2022. While correlation does not imply causation, the convergence of these historical patterns warrants careful consideration.

The Buffett Indicator: A Broader Perspective

Complementary to the CAPE ratio, the Buffett Indicator—a ratio of total U.S. equity market capitalization to U.S. Gross Domestic Product—provides an alternative valuation benchmark. This metric, popularized by Warren Buffett, offers a broader assessment of market overvaluation. A rising ratio suggests that equity valuations are expanding relative to the underlying economic output.

The Buffett Indicator currently registers at approximately 219%, exceeding levels observed during the 1999 technology bubble and significantly above its historical average. Mr. Buffett himself, in prior commentary, indicated that ratios approaching 200% should be approached with caution, suggesting an increased probability of market correction.

Strategic Considerations for Portfolio Management

While no single metric can reliably forecast short-term market movements, the convergence of elevated valuation multiples—as indicated by both the CAPE ratio and the Buffett Indicator—suggests a heightened degree of risk within equity markets. Predictive accuracy remains elusive, and the market may continue to exhibit upward momentum for an indeterminate period.

However, prudent portfolio management necessitates a focus on downside risk mitigation. Consider the following:

- Emphasis on Quality: Prioritize investments in companies with robust fundamentals, sustainable competitive advantages, and demonstrable earnings power.

- Diversification: Maintain a diversified portfolio across asset classes to reduce concentration risk.

- Valuation Discipline: Adhere to a rigorous valuation framework, avoiding investments with excessive price multiples.

- Long-Term Perspective: Maintain a long-term investment horizon, recognizing that market corrections are an inherent part of the investment cycle.

A disciplined approach to portfolio construction, focused on quality, diversification, and valuation discipline, may provide a degree of protection against potential market volatility and position investors to capitalize on long-term growth opportunities.

Read More

- Games That Faced Bans in Countries Over Political Themes

- Gold Rate Forecast

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- The Best Directors of 2025

2026-03-02 01:02