The artificial intelligence (AI) chip sector has become a battleground for investors seeking growth and income. While Nvidia, AMD, and hyperscalers dominate headlines, a critical player operates beneath the surface: Taiwan Semiconductor Manufacturing (NYSE:TSM). This analysis examines TSMC’s structural advantages in the AI revolution and its potential as a dividend-generating compounder.

Foundry Dominance: The Infrastructure Dividend Play

- TSMC controls approximately 70% of global semiconductor foundry capacity, positioning itself as the indispensable manufacturing partner for AI chip developers.

- Its client roster spans both established GPU providers (Nvidia, AMD) and custom silicon innovators (Amazon’s Trainium, Alphabet’s TPUs).

- This agnostic position insulates the company from winner-takes-all dynamics, ensuring revenue stability across AI chip architectures.

The company’s manufacturing expertise creates a self-reinforcing cycle: leading-edge process technologies (3nm, 2nm) attract high-volume orders, which in turn fund R&D for next-generation nodes. This virtuous loop strengthens TSMC’s moat against competitors like Samsung and Intel.

Structural Demand Drivers for Dividend Sustainability

Three key trends underpin TSMC’s long-term revenue visibility:

- AI Infrastructure Expansion: Hyperscalers allocated $120B+ to data center modernization in 2023, with 45% of capex tied to AI-specific silicon.

- Process Node Complexity: Advanced packaging technologies (CoWoS, 3DFabric) require $20B+ in fabrication facility investments, creating high barriers to entry.

- Geopolitical Realignment: U.S. CHIPS Act subsidies and European semiconductor initiatives reduce regional concentration risk for TSMC’s manufacturing footprint.

Valuation Framework and Dividend Prospects

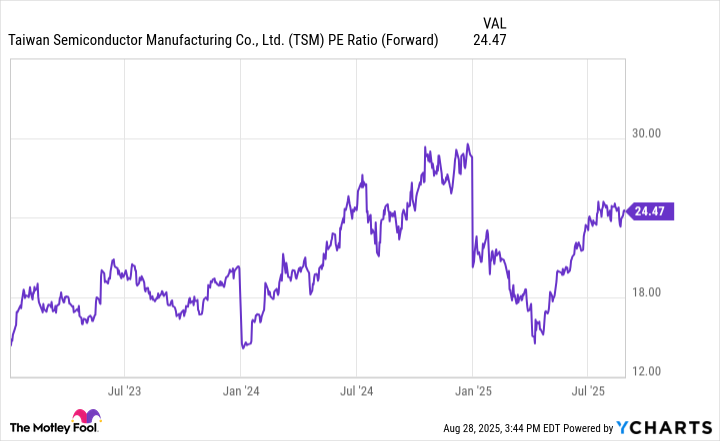

TSMC’s current 24x forward P/E multiple reflects market recognition of its strategic importance. However, several factors suggest valuation expansion potential:

- EBITDA margins consistently above 50%, driven by pricing power in advanced nodes

- Free cash flow yield of 5.2%, supporting both dividend payments and R&D reinvestment

- Debt-to-equity ratio below 0.2, enabling financial flexibility in cyclical downturns

The company’s dividend history demonstrates commitment to shareholder returns, with consecutive annual increases since 2010. Current yield of 1.8% offers modest immediate income, but the structural demand case suggests dividend growth potential of 10-12% annually through 2030.

Risk Considerations for Income Investors

- Geopolitical exposure: 60% of revenue originates from North America

- Technological disruption risk from alternative materials (GaN, SiC)

- Valuation sensitivity to AI adoption curve timing

While not without challenges, TSMC’s combination of technological leadership, diversified client base, and pricing power creates a compelling case for dividend-oriented investors seeking exposure to AI infrastructure growth. The company’s role as the semiconductor industry’s “tollkeeper” positions it to generate reliable cash flows across market cycles.

For dividend hunters prioritizing both income stability and long-term growth, TSMC merits consideration as a core holding in technology portfolios 📈.

Read More

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- TV Shows That Race-Bent Villains and Confused Everyone

- Top 10 Coolest Things About Invincible (Mark Grayson)

- Unmasking falsehoods: A New Approach to AI Truthfulness

- Palantir and Tesla: A Tale of Two Stocks

- Smarter Reasoning, Less Compute: Teaching Models When to Stop

- How to rank up with Tuvalkane – Soulframe

- Gold Rate Forecast

2025-08-31 19:02