![]()

Taiwan Semiconductor Manufacturing, or TSMC as it is more colloquially known, enjoyed a year of considerable ascent in the recent past. One might even say it flourished. Yet, to dwell excessively on past performance is a habit best left to those of a sentimental disposition. The market, like the seasons, moves relentlessly onward, and it is the promise of the coming year, not the memory of the last, that truly holds our attention.

The current expectation, and a reasonably assured one at that, is that TSMC will maintain its trajectory. The prevailing winds, if one may employ a meteorological analogy, are decidedly in its favor. These winds, of course, originate from the burgeoning field of artificial intelligence – a domain of immense potential, and one that demands ever-increasing computational power. It is a force, one suspects, that will not easily be contained.

The company has recently reported its quarterly earnings, and the guidance offered for the coming periods is, to put it mildly, encouraging. One might even venture to suggest that the current valuation does not fully reflect the extent of its dominance. It is a curious phenomenon, this reluctance of the market to acknowledge true strength. Perhaps it is a vestige of an older, more cautious era.

TSMC: At the Heart of the Computational Awakening

The demands of artificial intelligence are, quite simply, insatiable. It requires not merely power, but a vast, almost unimaginable quantity of it. This translates, inevitably, into a corresponding demand for the hardware upon which these calculations are performed. And within that hardware, at the very core of it all, lie the chips – those intricate, almost mystical components that bring it to life. Relatively few foundries possess the capability to manufacture these chips to the exacting standards required, and TSMC stands preeminent among them.

It is the principal supplier of logic chips to such notable companies as Nvidia and Apple. When demand for computational power surges – as it undoubtedly will in the realm of artificial intelligence – TSMC is naturally positioned to benefit. The recent quarterly results confirm this, and suggest that the current momentum is likely to continue unabated. It is a spectacle, one might say, of quiet, relentless progress.

In the most recent quarter, TSMC’s revenue increased by 26% year over year. A substantial gain, certainly, but not merely an isolated incident. The company anticipates a further increase of nearly 30% in the coming year, and projects a compound annual growth rate of approximately 25% over the next five years. Such a rate of growth, for a company of this scale, is rarely encountered. It suggests a fundamental shift in the landscape, a burgeoning demand that is reshaping the very foundations of the digital world.

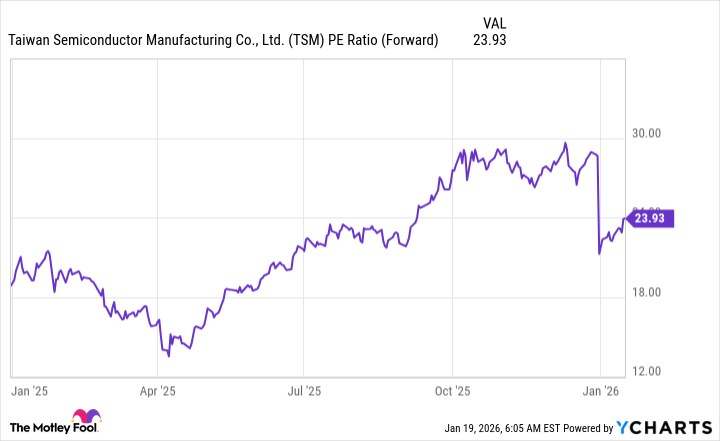

One might observe, with a touch of wry amusement, that TSMC, despite its success, remains undervalued. It is a curious paradox, this tendency of the market to overlook true potential. Perhaps it is a consequence of our inherent skepticism, our reluctance to embrace the truly exceptional.

A Discount Amidst the Rising Tide

Most large technology companies trade at approximately 30 times forward earnings. Nvidia, of course, commands a premium due to its exceptional growth. Yet, none of these companies are likely to achieve the 30% revenue growth that TSMC is poised to deliver. And yet, TSMC trades at a multiple of only 24. A discrepancy, one might say, that warrants closer inspection.

For comparison, the S&P 500 trades at 22.3 times forward earnings. While TSMC commands a slight premium over the broader market, its growth prospects are demonstrably superior. It is a situation, one might say, that presents a compelling opportunity. To acquire a stock with a clearly defined growth trajectory, at a price that appears, by any reasonable measure, to be undervalued. It is a rare occurrence, and one that should not be ignored.

It is not often that one encounters such a confluence of factors – a strong growth case, a reasonable valuation, and a dominant market position. TSMC, in this moment, appears to be precisely such a stock. It is a “picks and shovels” play, as the saying goes, for the generative AI buildout. And with AI spending expected to remain robust for the foreseeable future, it is difficult to imagine a better positioned company to capitalize on this trend. A steady bloom, perhaps, in the ever-shifting digital spring.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

2026-01-23 00:32