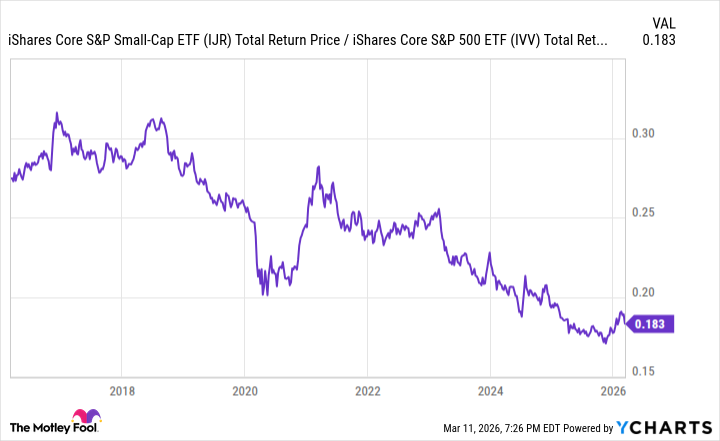

For years, the towering edifices of megacap technology have cast a lengthening shadow across the American equity landscape, absorbing capital and attention like a planetary force. Small capitalization stocks, once considered a necessary diversification, a scattering of seeds against the monoculture, have languished, their potential stunted. Since 2021, they have known only the slow erosion of relative performance, a decline measured against the ever-ascending benchmark of the S&P 500. The chart, a silent testament to this imbalance – depicting the iShares Core S&P Small Cap ETF against its larger cousin – reveals not merely a divergence, but a quiet expropriation of opportunity.

The prevailing narrative speaks of earnings growth, a metric treated as immutable law. The S&P 500, for eleven consecutive quarters, has offered a steady stream of positive year-over-year results, a testament to efficient extraction and relentless optimization. Six quarters have seen double-digit increases, a pattern of accumulation that borders on the predictable. Yet, consider the S&P 600 Small Cap Index. For the same period, it endured six consecutive quarters of earnings contraction – a negative ten percent or worse – a sustained winter of discontent. Only recently, in the second quarter of 2025, did a tentative thaw begin.

But the inertia of the past is not destiny. A shift, subtle yet potentially profound, may be underway. The current forecasts, if realized, suggest a convergence, a reckoning in the making.

A Flicker of Independence

The projections for the fourth quarter of this year indicate that the S&P 600 may generate 29% year-over-year earnings growth – nearly matching the 28% anticipated for the Nasdaq-100, the very citadel of megacap dominance. This is not merely a statistical coincidence, but a signal, however faint, that the smaller enterprises are beginning to stir, to reclaim a portion of the prosperity that has flowed so disproportionately to the few.

This matters profoundly because the valuation of these small-cap entities has been suppressed, burdened by the weight of subpar earnings. The iShares Core S&P Small Cap ETF currently trades at a price/earnings ratio of 18, while the iShares Core S&P 500 ETF commands a ratio of 28. A disparity understandable, perhaps, when earnings growth favored the larger firms, but unsustainable in a landscape where the seeds of renewal are beginning to sprout. The discount, a lingering vestige of neglect, has not adequately adjusted to the shifting conditions. It has not yet been recalibrated to reflect the promise of forward earnings.

To expect parity in price/earnings ratios would be naive. But to dismiss the inherent value within the S&P 600 as illusory is to ignore the evidence. This submerged potential, once unlocked, could trigger a sustained period of outperformance – a restoration of balance in a system long skewed towards concentration.

Over the coming years, the discerning investor may find greater reward in the resilience and adaptability of these smaller enterprises. In the American equity category, the better bet, the more prudent wager, may well lie with the small cap.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- 15 Films That Were Shot Entirely on Phones

- Trading Crypto with AI: A New Approach to Portfolio Management

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

2026-03-18 14:12