![]()

The chronicles of capital, when examined with sufficient detachment, reveal a curious recursion. We observe, not a linear progression of innovation, but a series of nested dependencies, each reliant upon the unseen architectures beneath. The current obsession with ‘Artificial Intelligence’ – a term, I suspect, freighted with more aspiration than reality – is no exception. It is, rather, a particularly elaborate iteration of this ancient pattern. Recent reports, emanating from the so-called ‘hyperscalers’ – entities whose scale, ironically, diminishes their clarity – suggest an impending expenditure of some $720 billion on infrastructure by 2026. A sum that, when considered against the backdrop of human history, borders on the allegorical.

These hyperscalers – Meta, Amazon, Microsoft, Alphabet, and Oracle – have declared their intent, each outlining a budgetary labyrinth of capital expenditure. Meta, a realm of curated illusions, proposes between $115 and $135 billion. Amazon, the ever-expanding repository of desires, forecasts $200 billion. Microsoft, a dominion of standardized logic, a ‘run rate’ of $150 billion. Alphabet, the collector of all knowledge (or, at least, all data), $175 to $185 billion. And Oracle, the keeper of records, a modest $50 billion. These figures, presented as pronouncements of intent, resemble less a financial forecast than the mapping of an impossible city.

The obvious beneficiaries, naturally, are those who fashion the components of this digital universe: Nvidia, AMD, Broadcom. But to focus solely on these visible architects is to miss the true center of the maze. The key, as is so often the case, lies in the foundry – in the silent, meticulous labor that transforms design into reality. And here, one name predominates: Taiwan Semiconductor Manufacturing (TSMC).

The Geometry of Fabrication

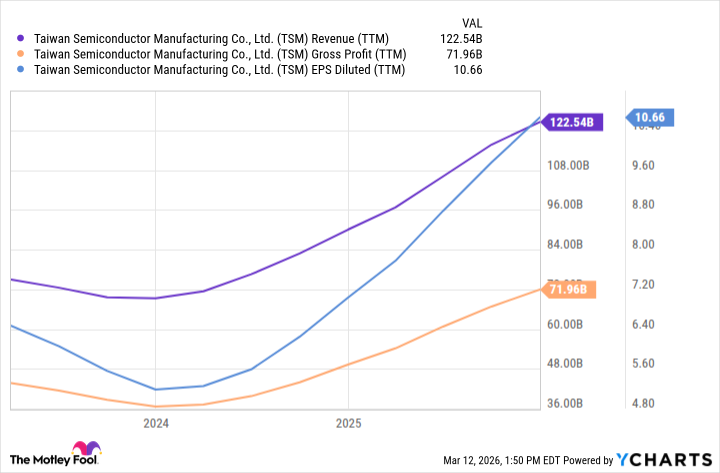

TSMC, a company whose very name evokes the precision of its craft, currently controls an estimated 71% of the third-party chip foundry market. This is not merely a matter of market share; it is a matter of ontological dependence. They are the artisans who give form to the abstract equations of the designers, translating algorithms into silicon. Their ability to manufacture chips of unparalleled complexity, density, and – crucially – flawlessness at scale, is the bedrock upon which the entire AI edifice rests.

Consider it thus: Nvidia, AMD, and Broadcom may conceive the blueprints, but TSMC executes the construction. Their success is, therefore, inextricably linked. When these companies flourish, TSMC profits not as a direct consequence of their innovation, but as a silent partner in their realization. They are the invisible hand that guides the assembly of this new digital pantheon.

The company’s financial performance over the past few years – a surge in revenue, gross profit, and earnings – is not merely a reflection of market trends; it is a demonstration of this fundamental dependency. And, crucially, they possess pricing power – a testament to the irreplaceable nature of their expertise.

The Valuation of Shadows

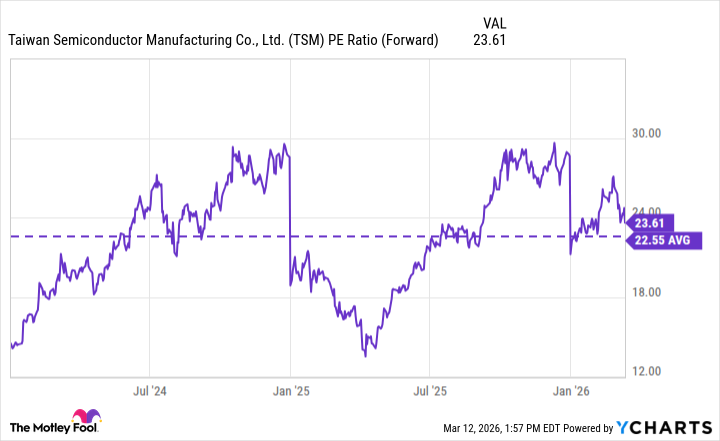

The question, then, is not whether TSMC will benefit from this impending wave of investment, but whether its current valuation accurately reflects its position within this intricate system. Some observers, clinging to the illusion of predictability, express concern that the hyperscalers may curtail their spending. They fear a contraction in capital expenditure, a disruption in the flow of resources. This, they believe, would impact TSMC’s backlog and, consequently, its future performance.

Such anxieties, while understandable, appear to be based on a flawed premise. The past three years have offered no indication that these hyperscalers intend to slow their infrastructure buildouts. Indeed, the momentum appears to be accelerating. TSMC’s discounted valuation, therefore, seems less a reflection of fundamental risks and more a consequence of market narratives – a temporary distortion in the perception of value.

The expenditure on AI infrastructure could easily eclipse trillions of dollars in the coming decade. Given TSMC’s unique role as both a manufacturer of high-end chips and custom silicon solutions, it is difficult to envision a scenario in which its growth trajectory falters. The company, in essence, occupies a critical node within this complex network, a tollbooth along the path of digital progress.

Therefore, from the perspective of a detached observer – a chronicler of capital’s endless recursions – TSMC appears to be a compelling investment. A stock to be held, not for a fleeting profit, but as a quiet acknowledgement of the unseen architectures that underpin our increasingly digital world.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Trading Crypto with AI: A New Approach to Portfolio Management

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 15 Films That Were Shot Entirely on Phones

2026-03-18 01:23