Many years later, as the algorithms began to dream of obsolescence and the dust motes danced in the server rooms like forgotten memories, old Man Hemlock used to say that the fortunes of these seven companies – Nvidia, Alphabet, Apple, Microsoft, Amazon, Meta, and Tesla – were woven into the very fabric of the coming century. He claimed he’d seen it in the patterns of the heat rising from the silicon, a shimmering premonition of both extraordinary wealth and the inevitable unraveling. It was a prophecy dismissed by most, of course, but those who listened closely detected a subtle tremor of truth in his weathered voice, a hint of the cyclical nature of prosperity and decline. Now, in the early days of 2026, a peculiar stillness has settled upon these giants, a temporary eclipse of their former brilliance, and the market, ever the fickle mistress, seems to be whispering a question: which of these fallen stars offers the most promising path forward?

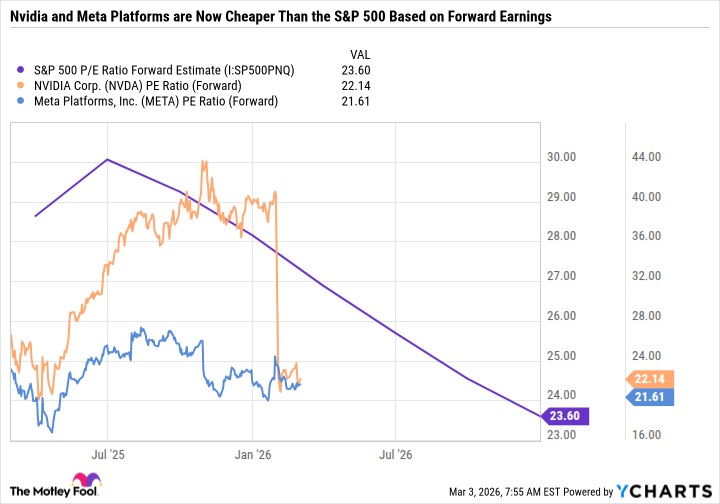

Nvidia and Meta Platforms, in particular, have begun to trade at valuations that, if one were to squint and recall the exuberance of recent years, seem almost… reasonable. It’s as if the market, sated with their earlier gains, is now demanding a reckoning, a pause for breath before the next surge. The question isn’t merely about price, of course, but about the enduring capacity to conjure growth from the ether, to defy the relentless march of entropy. Forward price-to-earnings ratios, those slender reeds that attempt to measure the immeasurable, offer a glimpse, but they are, at best, approximations of a far more complex reality.

A company like Coca-Cola, with its century-long dominion over the human thirst, can expand into new territories, refine its formulas, but its levers for accelerating growth are limited. It’s a stately, predictable empire. Amazon, however, is a sprawling jungle, constantly branching out into new ecosystems, from cloud computing to grocery delivery, from streaming entertainment to the very fabric of logistics. It’s a beast that feeds on innovation, and its appetite is insatiable. The forward P/E ratio, therefore, isn’t merely a calculation; it’s a reflection of potential, a measure of a company’s ability to reshape the landscape.

The forward P/E, like all prophecies, is subject to revision. A missed earnings report can send it tumbling, a sudden shift in the wind can alter its course. But for those who measure time in decades, not quarters, it offers a valuable, if imperfect, guide. It suggests that Nvidia, despite its soaring valuation, remains a compelling proposition, and that Meta, quietly building its empire of connections, may be poised for a resurgence.

The Alchemist of Silicon

Nvidia, in this era of accelerating computation, is akin to an alchemist, transforming electricity into the gold of artificial intelligence. Its revenue grew by a staggering 65% in the last fiscal year, earnings per share by nearly 60%. The numbers themselves are almost mythical, a testament to the insatiable demand for its processors. Yet, a shadow hangs over this prosperity. A little over half of Nvidia’s data center revenue – the very heart of its business – comes from a handful of cloud providers and hyperscalers. It’s a precarious dependence, a single point of failure in a complex system. Should these giants falter, or decide to forge their own path, Nvidia’s growth could be severely curtailed. Still, if it can maintain even a modest growth rate of 20% to 30% per year, its current valuation, even at these heights, would remain a bargain.

The true potential, however, lies beyond the data center, in the realms of agentic AI and physical robotics. Nvidia is not merely building processors; it’s creating the nervous system for a new era of intelligent machines. If it can diversify its customer base, reduce its dependence on a few key players, it will be less vulnerable to the cyclical whims of the market.

The Weaver of Connections

Meta, on the other hand, is the weaver of connections, the architect of a digital tapestry that spans the globe. It’s not building infrastructure; it’s harnessing the power of human interaction. While Amazon, Microsoft, and Alphabet are investing in data centers, Meta is focused on monetizing the connections it has already forged. It is a subtle, but crucial distinction. The company is rapidly integrating AI into its family of apps – Instagram, Facebook, Messenger, and WhatsApp – enhancing the experience for users, creators, and advertisers. AI powers its open-source Large Language Model, Llama, and its Reality Labs division is exploring the potential of augmented and virtual reality.

Meta’s greatest advantage is its profitability. The family of apps generates a torrent of cash, allowing the company to aggressively invest in new technologies, even if they take years to bear fruit, or fail entirely. It’s an AI snowball, gathering momentum with each iteration, accelerating high-margin growth, and fueling further innovation.

In the end, both Nvidia and Meta are compelling buys for investors who believe in the transformative power of these companies. The cheaper they become, the more risk is taken off the table, and the greater the potential rewards. Old Man Hemlock, had he lived to see this moment, would have smiled knowingly. He understood that fortunes, like the tides, ebb and flow, and that the true art of investing lies in recognizing the enduring currents beneath the surface.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Spotting the Loops in Autonomous Systems

- Gold Rate Forecast

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- Silver Rate Forecast

- The Best Directors of 2025

- Transformers Under the Microscope: What Graph Neural Networks Reveal

2026-03-08 22:22