The pursuit of quantum computation, a realm of shimmering possibility, holds a certain allure. It whispers of solutions to problems that vex even the most powerful of our current machines—a promise of unlocking new frontiers in science and, perhaps, even in the quiet accumulation of wealth. One envisions, in these nascent stages, a digital landscape reshaped, though whether for the benefit of the discerning investor remains, alas, a question fraught with uncertainty.

The very notion of superposition—the ability of a quantum bit, or qubit, to exist in multiple states simultaneously—is, in its way, a marvel. It suggests a capacity for parallel processing that dwarfs the capabilities of our familiar binary systems. Yet, it is a capacity hampered, at present, by a frustrating fragility. The error rates, even in the most meticulously constructed devices, remain stubbornly high, rendering practical application a distant, almost ethereal, goal. And within this field, Rigetti Computing, a company striving to tame these elusive forces, presents a case study in ambition and, one might venture, a certain degree of imprudence.

The shares of Rigetti, having already relinquished a considerable portion of their former value—a decline of two-thirds from their recent zenith—still bear a valuation that seems, to a practiced eye, rather… optimistic. It is a situation not uncommon in the feverish pursuit of novelty, where the promise of tomorrow often overshadows the realities of today. One is reminded of the fortunes built on railroads that never quite reached their intended destinations, or the dreams of gold miners who found only dust and disappointment. A careful assessment suggests that further decline is not merely possible, but, in the sober light of reason, rather probable.

The Long Road to Substance

Founded in 2013, Rigetti has, with considerable effort, constructed an end-to-end supply chain, encompassing chip fabrication, a bespoke quantum programming language called Quil, and a cloud platform for accessing their computational resources. This vertical integration is, on the surface, a prudent strategy, allowing for greater control and, potentially, faster innovation. However, it also represents a substantial capital commitment in a field where the very foundations are still shifting beneath one’s feet. The company boasts the Cepheus-1-36Q, currently the largest multi-chip quantum computer, and a gate fidelity of 99.5%. A commendable achievement, certainly, but one must remember that even a 99.5% accuracy translates to one error for every two hundred operations. In the realm of complex calculations, this is a burden that few systems can bear.

The classical computer, for all its limitations, operates with a reassuring certainty. Each bit is either a 0 or a 1, a simple truth that underpins the entirety of our digital world. The qubit, in contrast, exists in a state of flux, a superposition of possibilities. It is a beautiful concept, yet one that demands an extraordinary level of precision. Rigetti has recently achieved a gate fidelity of 99.9% in testing, a promising step forward, but one that remains confined to the laboratory. The translation of these results to a commercial setting is expected to take another three years, a considerable span in the rapidly evolving world of technology. The company plans to release a system with 99.7% fidelity by year’s end, a modest improvement that, while welcome, does little to alter the fundamental challenges.

Even at 99.9% fidelity, one error per thousand operations remains a significant impediment. It is akin to a cartographer meticulously charting a vast territory, only to discover a single, uncorrectable error in every thousand measurements. Such a discrepancy, while seemingly minor, can render the entire map unreliable. This underscores the distance that remains between the current state of quantum computing and its widespread adoption.

The Weight of Expectations

Unfortunately, the market for computers that offer limited practical utility is, shall we say, somewhat constrained. Rigetti generated a mere $7.1 million in revenue during the past year, a decline of 34% from the previous period. This paltry sum, when juxtaposed with a market capitalization approaching $6 billion, reveals a valuation that is, to put it mildly, disconnected from reality. One is reminded of a grand estate built on a foundation of sand—impressive to behold, perhaps, but ultimately unsustainable.

The construction of quantum systems is, unsurprisingly, an expensive undertaking. Rigetti incurred operating expenses of $86.7 million last year, with a staggering $61.3 million devoted to research and development. This relentless pursuit of innovation, while admirable, has resulted in an operating loss of $84.6 million and a net loss of $216.2 million. Even when adjusted for non-cash expenses, the company still lost $50.5 million. Such figures, while not necessarily fatal, raise serious questions about the long-term viability of the enterprise.

Fortunately, Rigetti possesses a substantial cash reserve of $443.5 million, providing a temporary buffer against these losses. However, with minimal revenue trickling in, management will inevitably face difficult choices—drastic cost-cutting measures or the dilution of existing shareholders through further equity offerings. Both options are unpalatable, and neither guarantees success.

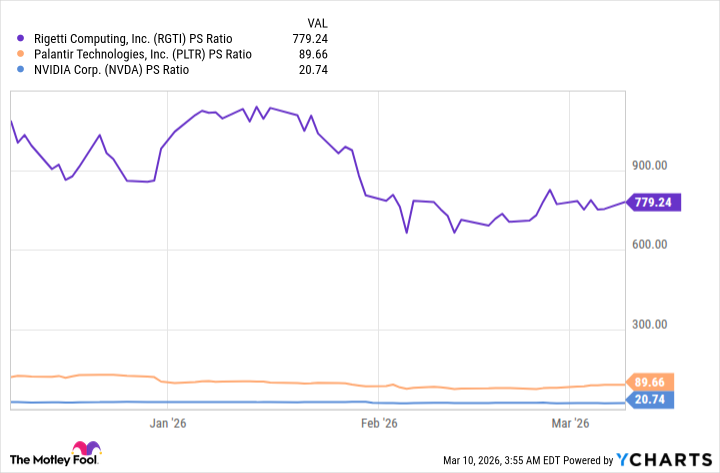

A Valuation Steeped in Hope

Rigetti’s stock has already experienced a decline of 25% this year, and a total of 62% from its previous peak. Yet, its price-to-sales ratio remains an astonishing 779. Such a figure is simply unsustainable, a testament to the boundless optimism that often pervades the technology sector. For comparison, Palantir Technologies, often considered one of the most richly valued large-cap stocks, trades at a P/S ratio of 89. Nvidia, the leading supplier of AI data center chips, trades at a mere 20. The disparity is striking.

Rigetti’s stock would need to plummet by 88% from its current price just to align with Palantir’s valuation, and even then, one might still consider it expensive. Furthermore, if the company’s revenue continues to shrink, its P/S ratio will actually increase, fueling further arguments for downside. It is a precarious situation, reminiscent of a traveler teetering on the edge of a precipice, with no clear path forward.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Top 20 Dinosaur Movies, Ranked

- Silver Rate Forecast

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- Gold Rate Forecast

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Games That Faced Bans in Countries Over Political Themes

2026-03-13 12:32