The current obsession with Artificial Intelligence is, naturally, a spectacle. One might say it is the latest iteration of humanity’s perpetual quest to automate its own irrelevance. The market, ever the eager accomplice, has identified a few beneficiaries, and, as is its custom, has begun to inflate their worth with the airy currency of speculation. It is a charmingly predictable drama. Two companies, Tower Semiconductor and Hut 8, have attracted a degree of Wall Street attention, though they remain largely unknown to the retail investor—a class often mistaken for discerning judges of value. One wonders if their obscurity is a blessing.

Both possess attributes that, in a more rational age, might warrant consideration. But reason, alas, is rarely a factor when fortunes are being made—or, more frequently, imagined.

Tower Semiconductor: A Specialist’s Plea

Tower Semiconductor, it seems, manufactures components for this brave new world—specifically, those involving light and data transmission. Wall Street, in a moment of unusual specificity, has noticed. Hood River Capital and Rockingstone Advisors, two entities with a demonstrated talent for separating fools from their money, have invested accordingly. The shares have, predictably, surged—by over 300% in the last year, no less. It is a reminder that in the theatre of finance, the play is often more important than the performance.

The company specializes in photonic integrated circuits, which, as I understand it, involve transmitting data at a rather impressive speed. The CEO, with admirable candor, claims they are “by far the majority supplier” of this particular technology. One suspects that if the demand were not so artificially inflated, the market might inquire as to the actual need for such speed. But such inquiries are so dreadfully inconvenient.

The logic is simple, if somewhat circular: AI requires data, data requires speed, and Tower Semiconductor provides speed. Therefore, Tower Semiconductor is a sound investment. It is a narrative that appeals to those who prefer simplicity to understanding.

The company’s recent revenue figures are, of course, impressive—a 14% increase year over year. But one must remember that revenue is merely a measure of activity, not necessarily of value. A particularly successful confidence trickster, after all, can generate a considerable amount of revenue.

Hut 8: Power and the Pursuit of Profit

Hut 8, a company with a history rooted in the ephemeral world of cryptocurrency, has undergone a transformation. It now aims to provide the power necessary to fuel these AI systems. Flight Deck Capital and Oasis Management, two entities with a keen eye for opportunity, have taken notice. The shares have, naturally, soared. It is a testament to the market’s ability to find new ways to repackage old follies.

The company’s pivot from cryptocurrency mining to AI power is, in essence, a simple equation: same equipment, different narrative. CoreWeave, another former crypto enthusiast, has followed suit. It is a reminder that in the world of finance, reinvention is often more profitable than innovation.

Hut 8’s advantage, it seems, lies in its access to electricity. The U.S. Department of Energy warns of a potential shortage by 2030. This, naturally, has only fueled the frenzy. The company claims to have secured over a gigawatt of energy capacity. It is a comforting thought, though one wonders if they have also secured a monopoly on the sun.

The company’s revenue growth is, undeniably, impressive. Sales totaled $235.1 million in 2025, up from $162.4 million in 2024. But the construction of AI data centers is, as one might expect, expensive. The company reported a net loss of $248 million. A temporary setback, no doubt, on the road to untold riches. The balance sheet, at least, appears solid, with total assets of $2.8 billion and total liabilities of $1.1 billion. One might say it is a house built on sand, but with a rather impressive view.

A Word of Caution: The Price of Illusion

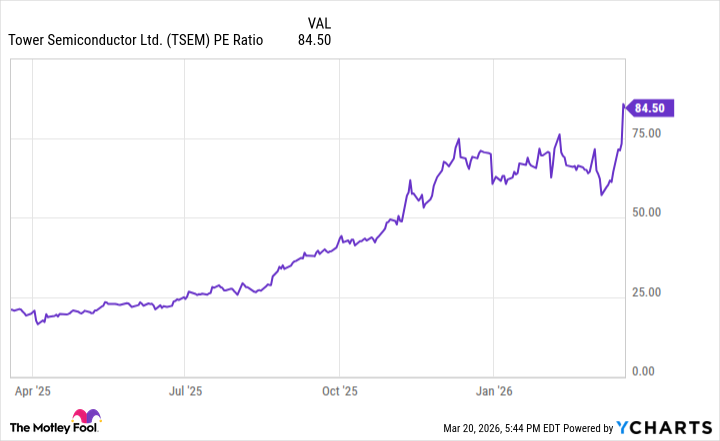

Wall Street’s enthusiasm for Tower Semiconductor and Hut 8 has, predictably, elevated their valuations. Tower Semiconductor’s price-to-earnings ratio is currently around 85—a figure that suggests either extraordinary future growth or a rather optimistic assessment of the present.

The chart reveals that Tower’s earnings multiple is at a rather elevated point. A prudent investor, one might suggest, would wait for a more reasonable price before entering the fray.

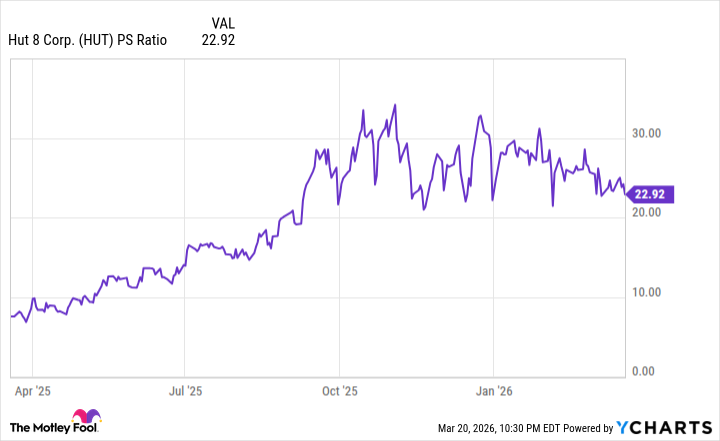

Hut 8, lacking profitability, must be assessed using the price-to-sales ratio, which currently stands at a lofty 23. This suggests that the company’s growth potential is already fully priced into the stock.

The chart shows that Hut 8’s sales multiple has come down slightly, but the stock remains volatile, with a beta of about 6. Another dip is likely. Patience, as always, is a virtue.

To lose one billion dollars may be regarded as a misfortune; to lose two looks like a reckless embrace of the future. The market, alas, rarely learns from its mistakes. It simply finds new ways to repackage old dreams.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Top 20 Dinosaur Movies, Ranked

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- Top 10 Coolest Things About Invincible (Mark Grayson)

- When AI Teams Cheat: Lessons from Human Collusion

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-24 21:04