The market, you see, is a most peculiar beast. It sniffs out the future, but often mistakes a shadow for substance. Everyone now speaks of Artificial Intelligence as if it were a deity descended from the silicon heavens. And while there’s undoubtedly something stirring in the ether, the true art lies in separating the prophets from the charlatans. One does not simply believe in AI; one observes its manifestations, its tributaries of profit. Three companies, at present, appear to be diverting a considerable flow. They are Nvidia, Microsoft, and Broadcom. Not, mind you, a guarantee of salvation, but a reasonable wager against the prevailing madness.

Microsoft

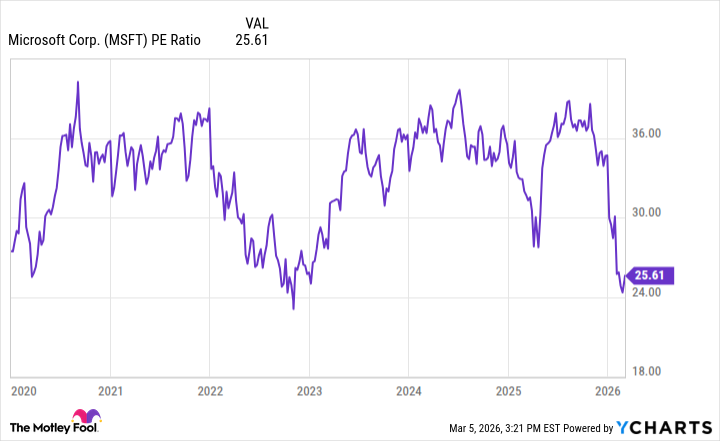

Microsoft. A behemoth, yes, but even behemoths stumble. The recent, shall we say, hesitation in its share price is a curious thing. Some fret over the expenditure on data centers – as if a kingdom can be built on thrift alone! – but I see it as a necessary indulgence. They are not merely spending money; they are constructing the cathedrals of the digital age. And, crucially, they are hosting the models of others, a subtle form of dominion. Revenue rose a respectable 17% – a perfectly adequate performance, though hardly earth-shattering. The analysts, those oracles of the obvious, predict continued growth. Yet, the price-to-earnings ratio… it’s almost as if the market has forgotten what a thriving enterprise looks like.

In late 2022, when the air was thick with recessionary fears, the same undervaluation was observed. Now, the specter of economic collapse has receded, yet the market remains… skeptical. It’s illogical, of course. The market rarely concerns itself with logic. It prefers melodrama. This, then, is an opportunity. A chance to acquire shares in a company that, despite its size, still possesses a surprising capacity for reinvention. A rather pleasant absurdity, wouldn’t you agree?

Nvidia

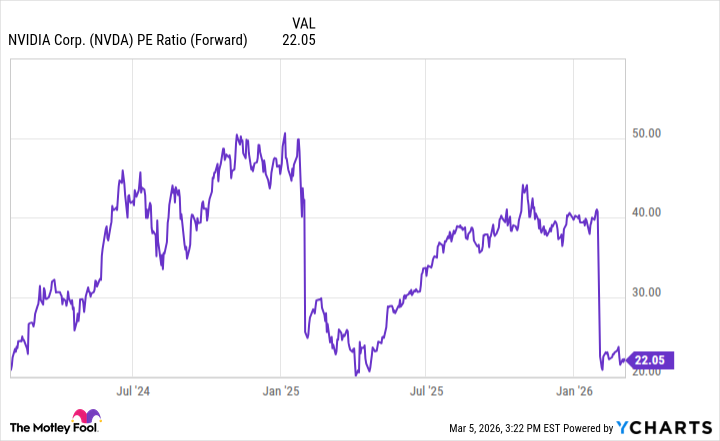

Nvidia. The name itself conjures images of power, of processing might. They have, for some time, been the primary suppliers to this AI frenzy. And yet, the market treats them with a peculiar restraint. The forward price-to-earnings ratio… it’s almost as if the market is waiting for the bubble to burst. A remarkably short-sighted perspective, given the scale of the undertaking.

At 22 times forward earnings, Nvidia appears… almost reasonable. They are growing rapidly – management anticipates a 77% surge in Q1 – yet remain undervalued compared to their peers. Some whisper of a bubble. Perhaps. But the major tech companies are already committing to substantial hardware purchases for years to come. This isn’t a fleeting trend; it’s a fundamental shift. The AI party, as they say, is only just beginning. And Nvidia, for the moment, holds a rather enviable position at the buffet.

Broadcom

Broadcom. A less flamboyant name, perhaps, but no less significant. They are crafting custom AI chips, a direct challenge to Nvidia’s dominance. Instead of offering broad-purpose GPUs, they collaborate directly with the hyperscalers, tailoring chips to specific needs. Less flexible, admittedly, but potentially far more efficient. A pragmatic approach, one might say. Like a skilled craftsman, rather than a flamboyant artist.

These ASICs won’t replace Nvidia’s GPUs entirely, but they offer a viable alternative. Demand has been strong – AI semiconductor revenue rose an astonishing 106% in Q1. Rapid growth is expected to continue. The price, at 32 times forward earnings, reflects this potential. It’s a premium, certainly, but a justifiable one. There are few companies meaningfully challenging Nvidia’s supremacy. Broadcom, therefore, warrants consideration. It’s a long shot, perhaps, but sometimes, the most interesting wagers are the ones with the highest stakes. The market, after all, is a game of illusions. And the best investors are the ones who can see through the smoke and mirrors.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- The Best Directors of 2025

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

2026-03-11 08:12