Right. So, March. The market, predictably, is being… difficult. It’s all a bit much, isn’t it? Everyone was so excited about AI, the “Magnificent Seven,” and now… well, now they’re just looking a bit peaky. All down year-to-date, even. Honestly, it’s enough to make one consider a career in alpaca farming. But, deep breaths. I’ve been staring at the numbers, fuelled by lukewarm coffee and a vague sense of impending doom, and I think I’ve identified a couple of opportunities. Or, at least, less-bad options. Units of Cryptocurrency Lost: 7. Hours Spent Refreshing Bloomberg: 11. Number of Times I’ve Considered Selling Everything and Moving to a Desert Island: 3.

Amazon: The Everything Store (Still)

Amazon. It’s just… enormous, isn’t it? It started with books, and now it’s basically running the world. E-commerce is the obvious bit, but it’s the sheer scale of everything else that’s impressive. AWS, their cloud platform, is a monster. Advertising is booming. Prime Video is… well, it’s there. And they’re tinkering with AI chips, which feels both sensible and slightly terrifying. It’s like they’re preparing for the robot uprising. I mean, good on them, really. Being prepared is key.

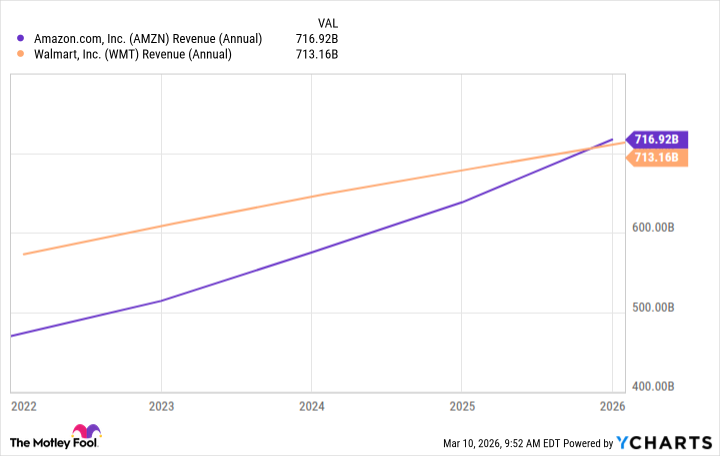

The e-commerce side is getting smarter, deploying robots to handle the warehouse chaos. AWS is seeing a resurgence, thanks to all the AI hype (which, let’s be honest, is probably 80% hype and 20% actual progress, but who’s counting?). And that advertising business is just printing money. It’s all very… efficient. It makes my attempts at organizing my sock drawer feel particularly pathetic. The important thing is, Amazon is a cash cow. A really, really big cash cow. They made $716.9 billion in revenue last year, surpassing even Walmart. It’s a bit frightening, actually. All that power in one company. But, from a purely financial perspective, it’s… compelling.

That kind of financial muscle gives them the flexibility to experiment, to take risks, to basically do whatever they want. Which is both exciting and slightly unsettling. It’s a bit like giving a toddler a flamethrower. But, you know, hopefully with better results.

Microsoft: The Sensible One

Microsoft. Now, Microsoft is different. It’s… reliable. It’s the sensible shoes of the tech world. It’s diversified, it has a massive enterprise client base, and it just keeps chugging along, regardless of whatever the latest Silicon Valley fad is. Which, frankly, is a relief. It’s a bit like having a solid, dependable friend who doesn’t suddenly decide to become a competitive hot dog eater. The focus is, understandably, on AI now, and they’re throwing a lot of money at it. But even if AI turns out to be a complete disaster (which, let’s be honest, is a distinct possibility), Microsoft will still be fine. It’ll still be bringing in billions. It’s almost… unfair.

Investing in Microsoft feels… safe. It’s like buying a really good raincoat. It might not be the most exciting purchase, but you’ll be glad you have it when the storm hits. Their products and services are embedded in businesses all over the world. They rely on Microsoft to keep things running. That’s a powerful position to be in. Businesses don’t tend to abandon their essential tools just because the economy is wobbly. Unlike, say, my attempts at learning the ukulele. That was abandoned after approximately three minutes.

From an AI perspective, Microsoft is well-positioned. They own key platforms that will benefit from AI, without being entirely dependent on it. Office, Azure, Teams, Windows… it’s a solid foundation. And they’re becoming increasingly vertically integrated, creating their own AI chips, building out their cloud platform, and leveraging their existing software. It’s all very… strategic. It makes my attempts at meal planning look particularly chaotic.

The Bottom Line (Probably)

Look, the stock prices have fallen. That’s a fact. And there’s no guarantee they won’t keep falling. I’m not a fortune teller. I’m just a portfolio manager trying to navigate a slightly terrifying market. But at current levels, Amazon and Microsoft look… interesting. Amazon’s price-to-earnings ratio is significantly lower than its historical average, and Microsoft’s is also looking attractive. It doesn’t automatically make them buys, but it’s definitely worth considering. Hours Spent Staring at P/E Ratios: 6. Number of Times I’ve Questioned My Life Choices: Too Many to Count. So, yes. Amazon and Microsoft. They’re not exciting. They’re not glamorous. But they might just be sensible. And sometimes, sensible is good enough.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- Silver Rate Forecast

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Trading Smarter: AI-Powered Execution Schedules

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

2026-03-13 23:04