Now, Target, you see, has been having a bit of a run – a positively ripping good thirty-one per cent leap in the last three months, which, when one considers the general market’s rather sluggish performance (a mere 1.9% incline, dashed uninspiring!), is something of a cheerful surprise. It’s as if the market, after a period of gloomy contemplation, decided that Target wasn’t quite ready for the knacker’s yard after all.

The retail giant, you see, is currently enjoying a wave of investor approval, largely based on the hopeful notion that the worst of its sales slowdown is, thankfully, behind it. And, of course, there’s the new CEO, Mr. Michael Fiddelke, whose appointment has instilled a certain degree of optimism – a bit like introducing a competent helmsman to a vessel that’s been listing dangerously. Still, one mustn’t get carried away. The shares, whilst showing a recent perk-up, remain a good twenty-five per cent down over the last three years, and a truly alarming fifty per cent off their all-time high. A bit like a promising young chap who’s had a rather unfortunate series of setbacks.

So, the question is, is it a shrewd move to acquire Target shares in March? Let’s have a bit of a look-see, shall we?

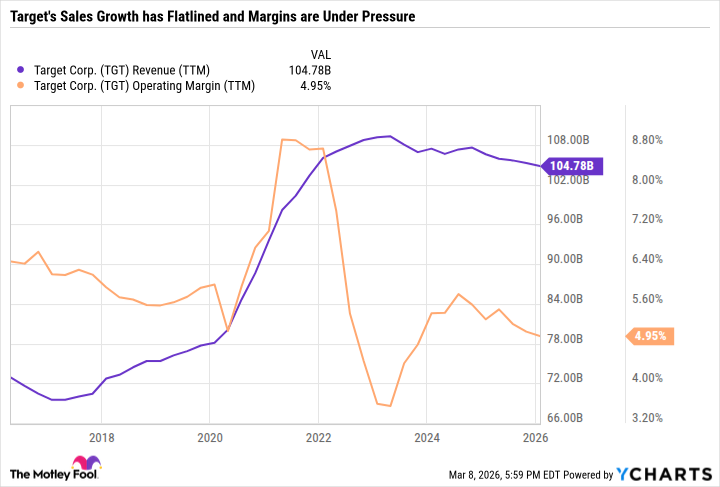

A Prolonged Period in the Doldrums

Target, you see, has been underperforming the broader market for a while now, and with good reason. Sales have been dwindling, and those all-important operating margins haven’t quite bounced back to their pre-pandemic levels. It’s a bit like a prize fighter who’s taken a few too many blows.

During the pandemic, Target rather overestimated the public’s appetite for, well, everything, and consequently found itself with a surplus of goods and a rather tangled supply chain. Adapting to the subsequent pullback in consumer spending proved, shall we say, a challenge. You see, Target can’t quite compete with the likes of Walmart or Costco on sheer price. It relies on a more…discretionary product mix and a bit of atmospheric charm. When times are good, Target offers a reasonably affordable and rather enjoyable shopping experience – a quick Starbucks, perhaps, and a few exclusive partnerships one wouldn’t find elsewhere. But when the purse strings are tightened, such fripperies tend to lose their appeal.

Target’s Bold Plans for a Revival

The previous CEO, Mr. Brian Cornell, a chap who steered the ship for over a decade, was focused on improving the stores, boosting foot traffic, and embracing that rather delightful “Tarzhay” spirit – making shopping fun, rather than a grim necessity. A dashed clever idea, what!

The new CEO, Mr. Fiddelke, is following in his predecessor’s footsteps, implementing an aggressive strategy to restore Target’s mojo. The plan involves opening over thirty new stores this fiscal year, remodelling over a hundred and thirty existing ones, and increasing capital expenditures by a substantial twenty-five per cent. A bit of a gamble, perhaps, but one can’t fault the ambition.

Interestingly, the stores still handle ninety-seven point six per cent of order fulfillment, but digitally originated sales now account for over twenty per cent of total sales – even exceeding the pandemic years of 2020 and 2021. This suggests that Target is winning with in-store pickup and drive-up – particularly through mobile orders. A modern touch, you see.

Target is also investing heavily in brand marketing, technology, and artificial intelligence. And, rather sensibly, they’ve managed to save two hundred million dollars through headcount reductions. A bit of streamlining, you see – prioritizing efficiency and productivity. A most commendable effort.

Mr. Fiddelke also recognizes the importance of the Target Circle loyalty program. Members spend three times more than non-members, and those in the “360” tier – with unlimited same-day delivery – spend a staggering seven times more. Loyal customers, you see, are a valuable asset. They also help Target determine which promotions and partnerships to pursue.

A Reliable Value Stock with a Decent Yield

Target’s strategy may take some time to bear fruit. The company is guiding for a modest two per cent year-over-year net sales growth and adjusted earnings per share of between $7.50 and $8.50. While fiscal 2025 might prove to be the nadir of Target’s turnaround, they’re still some way from regaining their pre-pandemic growth rate. So, whilst things are looking up, it’s not quite time to uncork the champagne.

Investors might be wondering why the share price has risen so much in recent months, despite the rather cautious guidance. The answer, I suspect, lies in expectations. The market, you see, dislikes uncertainty. With a new CEO and a clear game plan – albeit a slow one – investors might be willing to pay a premium for Target.

Currently, Target is trading at 15.1 times its fiscal 2026 guidance, which is roughly in line with its 10-year median P/E ratio of 15.3. Before the recent rally, the shares were rather undervalued, you see.

Just last June, Target announced its 54th consecutive annual dividend increase, boosting the quarterly payout to $1.14 per share, or $4.56 per year. They’re one of only 57 companies that have increased their dividends for at least 50 consecutive years – known as Dividend Kings. And, with a yield of 3.8%, Target offers a considerably higher return than many of its peers. A most satisfactory state of affairs.

Target Remains a Reasonable Buy

Heading into 2026, Target was so battered and bruised that even mediocre results and guidance were enough to spark a rally. The shares are still a decent buy, but they’re more fairly valued now. Lower interest rates tend to boost consumer spending, but the labor market is showing signs of weakness. Throw in the inflationary effects of higher oil prices, and the economic outlook isn’t exactly rosy. Still, the stock could be a good addition to the portfolio of long-term income investors – particularly those who believe that Target’s in-store shopping experience is a significant differentiator.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Top 20 Dinosaur Movies, Ranked

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- The Best Directors of 2025

- Silver Rate Forecast

2026-03-12 13:13