Now, SoundHound AI ([SOUN 2.45%]) – a name that sounds suspiciously like a dog with indigestion – is peddling conversational artificial intelligence. They claim their software whispers sweet nothings into the ears of cars, restaurants, and all sorts of businesses. Apparently, it’s quite the clever contraption, this ‘AI’, though I suspect it’s mostly just a very polite answering machine. Their customers, a gaggle of giants, are throwing money at it. Or at least, they were.

Last year, their revenues doubled, a rather boisterous boast. Management, those optimistic chaps, predict another year of growth. But the stock market, a beast with a particularly fickle appetite, has decided it doesn’t like the taste. It’s plummeted, first by a hefty 49%, and now, as we speak, is down another 19% this year. Seems investors finally noticed the valuation was puffed up like a prize-winning pumpkin. They’re now attempting to find a price that doesn’t require a ladder to reach.

The stock isn’t cheap, not by a long chalk, but there’s a glimmer of opportunity, a tiny speck of hope for those who enjoy a gamble. Let’s see what might unfold.

Conversational AI: A Bit of a Fuss

This ‘conversational AI’ is causing quite a stir. Restaurants, like Jersey Mike’s, Panda Express, and IHOP, are using it to take orders – presumably so they can fire the perfectly adequate humans. It’s a voice, you see, that never complains about sticky tables or grumpy customers. They even have an ‘Employee Assist’ – a voice-activated helper for the staff, which sounds suspiciously like a way to avoid proper training. Imagine a world where robots tell chefs how to boil an egg!

Car manufacturers are also getting in on the act, fitting these AI assistants into their vehicles. They can answer almost any question, which is all very well until someone asks it to explain the national debt. The manufacturers can choose from pre-made personalities, or concoct their own. A gruff, no-nonsense assistant for a pickup truck, perhaps? A prissy, overly polite one for a luxury saloon? The possibilities are endless…and slightly terrifying.

SoundHound is frantically adding new ‘solutions’ – a polite way of saying they’re throwing everything at the wall and hoping something sticks. They’ve signed over 100 new customers recently, which is impressive, though one does wonder if they’ve checked the references.

Revenue Rises, Losses Linger

Last year, SoundHound raked in a record $168.9 million – a 99% increase, they trumpet. They’re predicting between $225 million and $260 million this year. All very impressive, but let’s not forget the bottom line. They still lost $14 million, despite all the revenue. A rather large hole in the pocket, wouldn’t you say?

They claim this loss is smaller than last year’s – a staggering $351.1 million. A bit of accounting trickery helped, involving the ‘fair value’ of some liabilities. A complicated explanation, designed to confuse and bamboozle. They also managed to narrow their adjusted net loss by 22%, which is something, I suppose. Though it’s still a loss, naturally.

They have a healthy $248 million in the bank, which means they can keep losing money for a few more years. But investors, those demanding creatures, will want to see a profit eventually. Otherwise, they might need to raise more money, diluting the shares and leaving existing investors with a smaller slice of the pie. A rather unpleasant prospect.

A Price Too Steep?

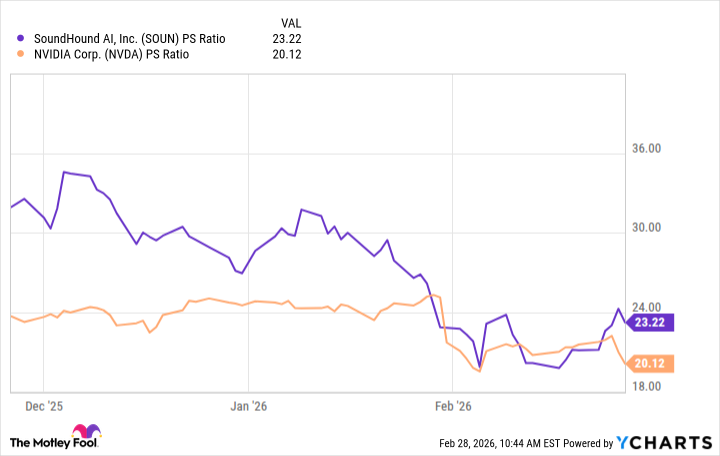

Despite the stock’s recent tumble, it’s still trading at a rather extravagant price-to-sales ratio of 23.2. That’s even more expensive than Nvidia, a company that actually makes things, and generates a proper profit. Nvidia is a solid, reliable beast. SoundHound, on the other hand, is a bit like a wobbly tower of building blocks.

Nvidia makes the chips that power all this AI nonsense. SoundHound just sells the voice. A slightly different business model, wouldn’t you say? I suspect investors are realizing this, which explains the recent decline. It’s a bit like realizing you’ve paid a fortune for a beautifully decorated cardboard box.

If we assume SoundHound’s revenue comes in around $242.5 million this year, the forward price-to-sales ratio drops to 14.9. That’s still a bit rich, but perhaps not entirely outrageous. There might be some upside later this year, after they report their first and second quarter results. By then, we’ll know if management’s predictions are realistic. Or if they’re simply whistling in the wind.

So, the downtrend in SoundHound’s stock might continue for a while. But it could also present a buying opportunity for those who enjoy a gamble. Just be prepared to lose your shirt. After all, in the world of high technology, fortunes are made and lost with alarming speed.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

2026-03-05 21:52