The firm of Muddy Waters – a name suggestive of both diligence and, shall we say, a certain earthiness – has recently deposited upon my desk a report concerning SoFi, a digital bank aspiring, it seems, to be all things to all borrowers. They present a most curious case, a labyrinth of financial engineering that would make even the most seasoned bureaucrat blush. SoFi, you understand, pitches itself as a one-stop emporium for all financial needs, targeting those with pockets sufficiently lined to avoid the common inconveniences of life.

They offer loans of every stripe – personal, student, even mortgages, should one desire a roof over their head – alongside online brokerage services, and the usual depositories for one’s hard-earned (or, more often, borrowed) funds. They even own a business dedicated to the technology of banking, a curious nesting doll of a venture, providing the very gears and levers for other financial institutions. A most ambitious undertaking, indeed.

Muddy Waters, with a perspicacity I confess I initially underestimated, alleges a certain…impropriety in SoFi’s accounting practices. Not outright fraud, mind you – that would be far too vulgar – but a series of adjustments, estimations, and off-balance-sheet transactions so complex they resemble a particularly tangled ball of yarn favored by a mischievous kitten. They claim SoFi’s reported performance is, shall we say, generously embellished.

The core of this contention lies in the fair value marks assigned to their loans. SoFi, it appears, prefers to estimate the worth of these debts, rather than simply observing what the market will bear. This estimation, naturally, involves a series of assumptions – weighted average yields, default rates, prepayment speeds, and a discount rate to account for the passage of time. A delicate dance of numbers, easily swayed by a biased hand.

The Fair Value Illusion

The majority of SoFi’s revenue, it seems, originates from lending – specifically, unsecured personal loans. They originate these loans, then swiftly dispatch them to investors, including those with a penchant for private credit. SoFi holds these loans on its balance sheet for a few months, a fleeting moment in the grand scheme of things, before passing them on.

For several quarters now, these fair value adjustments have been…positive. Astonishingly so. They’ve accumulated to over $1.1 billion on the personal loan book and over $723 million on the student loan book. A veritable windfall, if one were to believe the numbers. Muddy Waters, however, suggests these adjustments are based on inputs that are…optimistic, to put it mildly. The charge-off rate – the expected losses – and the discount rate, they claim, are suspiciously low.

Consider the charge-off rate. SoFi reported a rate of 2.80% in the fourth quarter of last year. However, Muddy Waters points out that this figure does not include loans sold before they’ve officially become delinquent. It’s as if one were to declare a building sound while conveniently ignoring the cracks in the foundation. Nor does it account for charge-offs occurring in those mysterious off-balance-sheet entities – variable interest entities, they’re called. A convenient place to hide one’s blemishes, wouldn’t you agree?

SoFi admits that, had they included those delinquent loans, the charge-off rate would be 4.4%. Still, that’s not the whole story. There are loans sold to these variable interest entities, loans that SoFi continues to service. A curious arrangement, indeed.

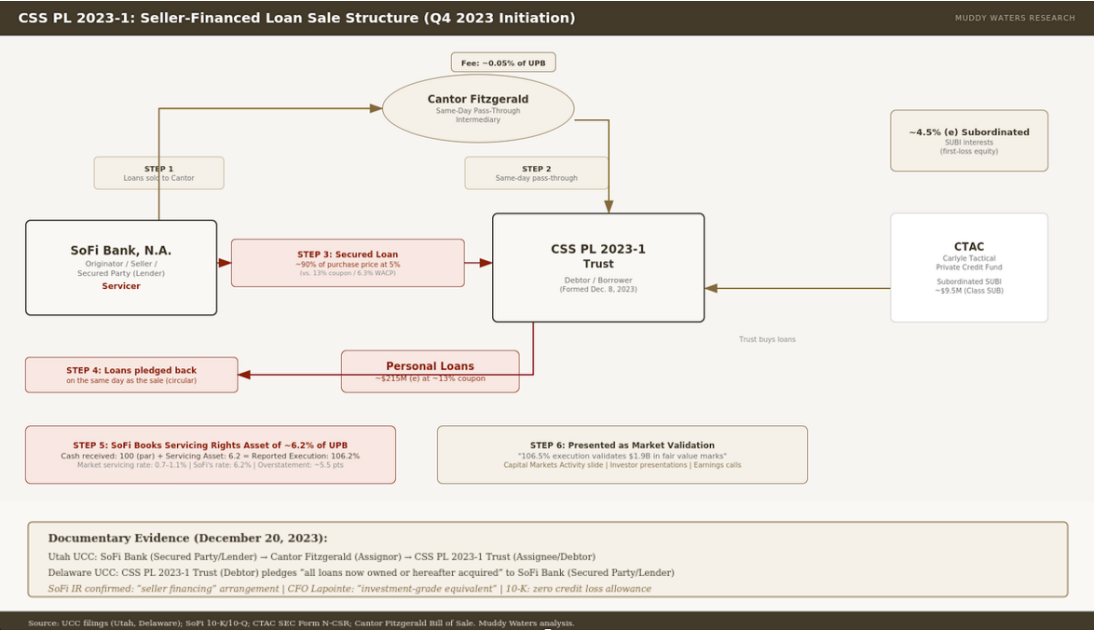

According to Muddy Waters, SoFi sells these loans to a pass-through entity – Cantor Fitzgerald, they allege – then extends a loan to a third party – a trust, typically – at a rate below market value. The trust then uses this loan to purchase the loans from Cantor, and pledges them back to SoFi as collateral. A circular transaction, reminiscent of a particularly convoluted Russian novel. SoFi then books a premium on the servicing asset, justifying the fair value marks. It’s a system of such exquisite complexity, one almost suspects it was designed to confound even the most diligent analyst.

If one were to include the charge-offs from these variable interest entities, Muddy Waters claims, SoFi’s charge-off rate would be closer to 6%. They also point to data from rating agencies, Fitch and DRBS, which have been revising their default assumptions for SoFi’s asset-backed securitizations upwards in recent years. A troubling sign, wouldn’t you agree?

The Servicing Rights Mirage

The servicing rights asset – the premium SoFi takes for managing these loans – is also, according to Muddy Waters, inflated. The rates they’re using – 6.2% for personal loans and 2.9% for student loans – are significantly higher than market rates. It’s as if they’re claiming to possess a secret formula for loan servicing, a formula that eludes all other practitioners.

Furthermore, the servicing rights asset in SoFi’s loan platform business – a business where they originate loans on behalf of third parties – is much lower than the premium they take on loan sales. A discrepancy that raises eyebrows, to say the least.

Other Peculiarities

The loan platform business and these off-balance-sheet transactions, Muddy Waters alleges, require significant capital. SoFi must provide loss protection to attract investors. These secured loans are also capital-intensive. This explains, perhaps, why they raised billions of dollars last year, increasing their diluted shares outstanding by about 30%. A necessary maneuver, perhaps, or a desperate attempt to stay afloat?

And then there’s the discount rate. Last year, SoFi used a rate of 3.89% to calculate the fair value marks for their student loan portfolio – 27 basis points below the 10-year Treasury yield. It’s as if they’re implying that student loans are less risky than U.S. government bonds. A bold claim, indeed.

They also capitalized $194 million in marketing costs, allegedly to boost their adjusted EBITDA. A maneuver that smacks of desperation, wouldn’t you agree? And then there’s the $312 million of unrecorded debt in the loan platform business.

If one were to adjust for these factors – higher charge-off rates, lower discount rates, lower servicing rights assets, and unrecorded liabilities – Muddy Waters claims SoFi’s adjusted EBITDA would be revised down by 90% – to about $103 million. A rather dramatic reduction, wouldn’t you say?

And all this, they allege, is being done to enrich management. While they haven’t sold any stock, CEO Anthony Noto and CFO Chris Lapointe have extracted over $58 million through prepaid variable forward contracts – a complex financial instrument that allows them to tap the liquidity of their stock while deferring taxes. A clever arrangement, perhaps, or a blatant display of self-interest?

A Word of Caution

SoFi, understandably, is not pleased with this report. They’ve dismissed it as inaccurate and claim it demonstrates a fundamental lack of understanding of their financial statements. They’ve also threatened legal action. And Mr. Noto has purchased about half a million shares of SoFi stock, a gesture of confidence, perhaps, or a desperate attempt to prop up the price?

This report is, admittedly, complex. While I cannot independently verify the off-balance-sheet allegations, I do find several aspects of SoFi’s business concerning. The fair value marks have been a red flag for some time, as several analysts have noted. SoFi uses more favorable inputs than its peers, even though it makes similar loans. Its competitors often report selling loans at a discount to fair value, taking negative fair value marks.

Personal lending is a high-loss business, and I see no indication that SoFi is any better at it than anyone else. The reports from rating agencies support this argument. And the cyclicality of the personal loan business should not be ignored.

In a high-rate environment, institutional loan buyers face higher costs of capital, demanding higher returns. This effectively prices many borrowers out of the market. A high-rate environment or a recession can also send loan buyers to the sidelines, worried about deteriorating credit.

SoFi has the ability to hold loans on its balance sheet, but a difficult environment for loan buyers would hit the loan platform business hard, leading to a significant decline in revenue.

Muddy Waters has received some criticism for stating its intention to cover most, if not all, of its short position. But I suspect this is because it’s difficult to short stocks with such a loyal following.

At face value, SoFi’s valuation has become more attractive. The stock trades at 29 times forward earnings, 14 times adjusted EBITDA, and 5 times forward adjusted revenue. But I would be wary of what could happen to adjusted EBITDA if Muddy Waters’ claims prove true.

I confess, I’ve never fully understood the fascination with SoFi. It runs many commoditized businesses, and customers simply choose based on who offers the most competitive rate. While management frequently discusses the advantage of being a purely digital bank, most banking products are now offered online.

I wouldn’t necessarily short the company, given the stock’s loyal following. But I wouldn’t buy it either.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Top 20 Dinosaur Movies, Ranked

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Gold Rate Forecast

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- Top 10 Coolest Things About Invincible (Mark Grayson)

- Celebs Who Narrowly Escaped The 9/11 Attacks

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-25 01:04