It is a truth universally acknowledged, that a company in possession of a novel cloud platform, must be in want of sustained growth. Snowflake, the creator of what is termed the Data Cloud – a repository for the valuable information of large organizations, even those scattered across the estates of Amazon Web Services and Microsoft Azure – finds itself, at present, in a position not entirely dissimilar to that of a young lady with a fortune, yet lacking a secure establishment. The ability to gather and analyze such data is, of course, of the utmost importance, and increasingly so in these times of rapid innovation.

Indeed, the unification of these disparate data sets is becoming quite essential for those engaged in the development of artificial intelligence. The more complete the picture, the more accurate the conclusions, and the more readily one might discern a profitable course. Snowflake, with its Cortex AI platform, offers a means by which businesses may both develop and deploy these intelligent systems, and has begun to assemble a suite of tools to collect, refine, and ultimately, present the results. It is a venture fraught with promise, yet not without its attendant anxieties.

The share price, it must be observed, has experienced a decline of some twenty percent in the current year, a circumstance which has caused a degree of consternation amongst investors. Yet, the overwhelming majority of those who offer counsel on such matters – those gentlemen of The Wall Street Journal – continue to recommend a purchase, none suggesting a hasty retreat. Their collective estimation of the stock’s potential suggests a considerable increase in value. One is left to ponder, therefore, whether this presents a judicious opportunity for investment.

Positioned for the AI Revolution

The Cortex AI platform, as it is termed, boasts a number of features designed to harness the power of artificial intelligence. Document AI, for instance, allows businesses to extract data from unstructured sources – contracts, invoices, and the like – with a speed and efficiency previously unattainable. Cortex Search, meanwhile, enables employees to locate critical information with ease, employing the language of natural discourse. A convenience not to be underestimated in these busy times.

The platform also hosts a collection of pre-made large language models, sourced from leading providers such as OpenAI, Anthropic, and Meta Platforms. Businesses may, therefore, plug their data into these models and create custom applications with considerably less expense than if they were to construct such models entirely from scratch. A most practical arrangement, one might observe.

As of the end of the last fiscal quarter, Snowflake boasted thirteen thousand three hundred and twenty-eight customers, of whom nine thousand one hundred were actively utilizing at least one of its AI features. A considerable increase from the previous year, suggesting a growing appetite for such technologies. It remains to be seen, however, whether this appetite will translate into sustained profitability.

Decelerating Revenue Growth and Growing Losses

Snowflake generated four and a half billion dollars in product revenue during the last fiscal year, representing an increase of twenty-nine point one percent. While not inconsiderable, this growth rate is marginally slower than the previous year. A slowing of momentum, however slight, is always a cause for careful consideration, particularly when viewed in conjunction with the company’s increasing expenses.

Operating expenses jumped by eighteen percent to a record four and a half billion dollars, driven by increased spending on marketing and research. This resulted in a net loss of one and a half billion dollars, a circumstance which cannot be dismissed lightly. One might venture to suggest that a prudent household would not conduct its affairs in such a manner.

The bottom line appeared somewhat more favorable after accounting for one-off and non-cash expenses, with Snowflake reporting an adjusted net profit of four hundred and sixty-five million dollars. However, a significant portion of this profit was derived from stock-based compensation distributed to employees. While a generous gesture, it does, inevitably, dilute the holdings of existing shareholders. A consideration which cannot be overlooked.

Investors, one imagines, expect to see a return on their investment. If Snowflake’s revenue growth were to accelerate, some of the concerns regarding its bottom line might be more easily dismissed. However, there is a distinct lack of organic growth, suggesting that a reduction in expenses – such as marketing – could further impede its progress. A delicate balance, indeed.

Wall Street is Bullish, but Snowflake Stock Isn’t Cheap

Of the fifty-two analysts who follow Snowflake, forty have issued a buy recommendation. Five others are inclined towards a bullish outlook, while the remaining seven suggest a cautious approach. None, it should be noted, recommend selling. A consensus, one might observe, which is not to be disregarded.

Their average price target is two hundred and forty-eight dollars and seven cents, suggesting a potential increase of forty-three percent over the next twelve months. The most optimistic estimate, however, places the potential upside at one hundred and eighty-nine percent. Such projections, while enticing, appear somewhat ambitious.

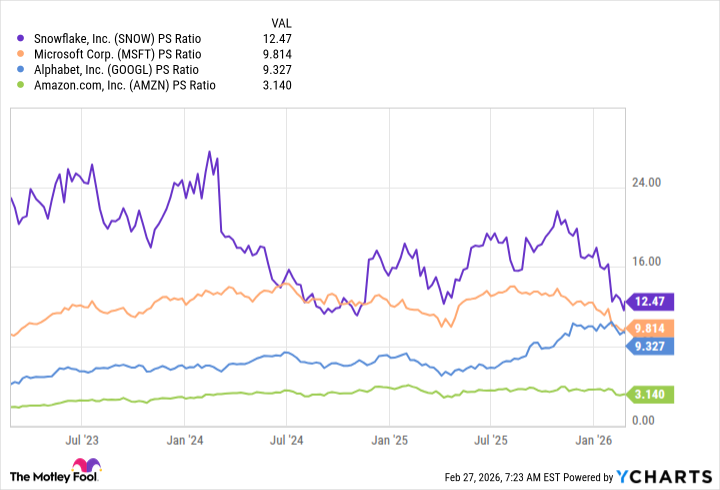

Snowflake is currently trading at a price-to-sales ratio of thirteen point two, a figure which, while near a three-year low, remains rather high. While comparisons are difficult, as few companies offer a similar portfolio of services, it is considerably more expensive than the major cloud providers. One might venture to suggest that the market has priced in a considerable degree of future success.

Amazon, Microsoft, and Alphabet operate a diverse range of businesses, making direct comparisons somewhat problematic. However, it is worth noting that Microsoft’s cloud division experienced revenue growth of thirty-nine percent in the last quarter, while Google Cloud saw an increase of forty-eight percent. Snowflake’s slower growth rate, therefore, makes its premium valuation difficult to justify. Prudent investors might, perhaps, wait for a more substantial correction before considering a purchase, regardless of Wall Street’s bullish sentiments.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

2026-03-04 23:14