Many years later, when the servers themselves had begun to whisper of digital melancholy, old Mateo, the data center custodian, would recall the peculiar stillness that descended upon the valley of silicon before the great blossoming. It wasn’t a silence of absence, but a pregnant hush, the kind that follows a fever dream, a premonition of fortunes made and lost in the blink of a transistor. He remembered the metallic tang in the air, the scent of cooling fans mingling with the distant, almost forgotten smell of rain on dry earth, and knew, with a certainty that bypassed reason, that the world was about to be remade, not in flesh and bone, but in the intricate, shimmering language of chips.

For decades, the giants of computation – the graphics processing units, or GPUs – held dominion over the burgeoning realm of artificial intelligence. They were the workhorses, the tireless engines that fueled the algorithms, the ones who could calculate the impossible with a speed that mocked the human mind. But even the most powerful of beasts must yield to the relentless march of evolution. A new lineage was rising, forged not in the fires of general purpose, but in the precision of purpose: the application-specific integrated circuits, or ASICs, the custom processors tailored to a single, demanding task. These were not merely chips; they were the digital equivalent of a master craftsman’s tool, honed and perfected for a singular, exquisite function.

The difference, whispered amongst the engineers, wasn’t merely one of efficiency – though a reported 30 to 40 percent gain in power usage was not to be dismissed lightly. It was a shift in philosophy. GPUs, like sprawling empires, could conquer many lands, but often at a cost. ASICs, by contrast, were focused, monastic in their dedication, achieving a level of performance that bordered on the miraculous within their narrow domain. It was becoming clear, even to the most skeptical among us, that the future of AI inference – the act of using intelligence, rather than creating it – lay in these specialized creations. TrendForce, those meticulous chroniclers of the digital age, predicted a surge in ASIC sales, a 45 percent increase by 2026, leaving the anticipated 16 percent growth in GPU shipments trailing like a forgotten dream.

And so, the astute investor, the one who reads the currents beneath the surface of the market, began to seek out the architects of this new era. Two names resonated with particular clarity: Broadcom and Marvell Technology, the leading contenders in the race to dominate the custom AI chip landscape. Both companies, it seemed, were poised to reap the rewards of this technological shift, but which one, if pressed, offered the more promising path to prosperity? The question hung in the air, thick with the scent of possibility.

The Blossoming of Two Fortunes

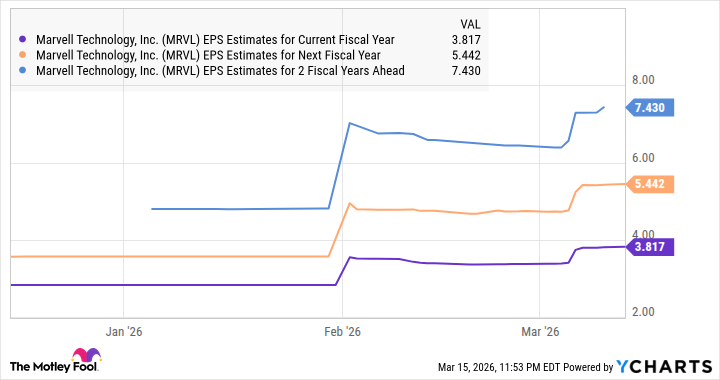

The recent earnings reports, released like ancient scrolls revealing hidden prophecies, confirmed what many had suspected: both Broadcom and Marvell were thriving in this new climate. Marvell, a company once known for its humble beginnings, reported a 22 percent year-over-year revenue increase in its fiscal 2026 fourth quarter, reaching $2.22 billion. Their adjusted earnings, a testament to their newfound efficiency, rose by an even more impressive 33 percent to $0.80 per share. The company’s data center business, invigorated by the adoption of their networking components and custom processors, was flourishing. Revenue from their custom processors had doubled in the previous fiscal year, and they anticipated a similar doubling in networking switch sales in fiscal 2027. A quiet confidence, a sense of inevitable growth, permeated their statements.

With the data center business now accounting for a substantial 74 percent of Marvell’s revenue, it was clear that the company had successfully navigated the treacherous currents of the market. They had raised their full-year guidance to $11 billion, a significant increase from their initial expectation of $9.5 billion. They were on track to ramp up production of several custom AI chip programs, a signal that their momentum was not merely a fleeting phenomenon. Marvell, it seemed, was building a fortress, brick by silicon brick.

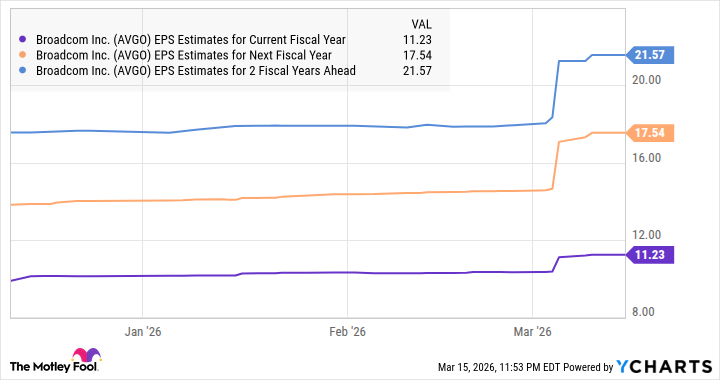

But Marvell was not alone in this endeavor. Broadcom, a name synonymous with innovation and scale, was also experiencing a surge in growth. Their fiscal 2026 Q1 results, released with the solemnity of a royal decree, revealed a 29 percent increase in revenue compared to the previous year, with adjusted earnings rising almost identically to $2.05 per share. The growth rates of the two companies were remarkably similar, a testament to the overall strength of the market. However, beneath the surface, a subtle divergence was beginning to emerge.

Counterpoint Research, those meticulous observers of the digital landscape, predicted that Broadcom would ultimately pull ahead, commanding a dominant 60 percent of the custom AI chip market in 2027. This robust market share translated into significantly faster growth in AI revenue. Broadcom reported a 106 percent year-over-year increase to $8.4 billion, dwarfing Marvell’s 21 percent growth in their data center business. They anticipated a further acceleration in AI revenue growth in the current quarter, projecting a staggering $10.7 billion, a potential increase of 143 percent. Broadcom, it seemed, was not merely building a fortress; they were constructing an empire.

Moreover, Broadcom’s commanding position in the custom chip market gave them the confidence to project at least $100 billion in AI revenue in fiscal 2027. They claimed to have already secured the supply chain needed to achieve this ambitious goal, ensuring they could serve top customers such as Anthropic, Meta Platforms, Alphabet’s Google, and OpenAI. They were, in essence, laying claim to the future of artificial intelligence.

The Choice Before Us

Both Marvell and Broadcom, it seemed, were poised to capitalize on the secular growth of the custom AI chip market. An investor could scarcely go wrong by choosing either of these two stocks. However, for the value-oriented investor, the one who seeks a bargain amidst the frenzy, Marvell might prove the more appealing choice. The charts, those silent storytellers of the market, revealed a compelling truth: Marvell traded at a cheaper valuation, offering a potentially greater upside. The market, perhaps, would eventually reward Marvell with a premium valuation, paving the way for solid gains.

Broadcom’s premium valuation, however, was not without justification. Their dominant market share in custom AI chips and the massive acceleration in growth they anticipated warranted a higher price tag. For the investor with a higher risk appetite, the one who seeks the best-of-breed stock, Broadcom might prove the more rewarding choice, even if it came at a steeper price.

The choice, ultimately, rested with the individual investor. But one thing was certain: the age of custom AI chips had arrived, and the fortunes of those who dared to invest in this new era were about to be written in the language of silicon.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Silver Rate Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- The Best Former NFL Players Turned Actors, Ranked

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 20 TV Series That Killed Their Best Character and Survived

2026-03-18 21:03