![]()

Okay, Realty Income. [O 0.34%]. Everyone’s all excited about this dividend stock. Double-digit returns, they say. It’s like they want you to forget the last few years. I mean, come on. It’s not like amnesia is a viable investment strategy. And now suddenly it’s a great buy? It feels…convenient. Like they’re trying to pull a fast one. And you know what really gets me? The monthly dividend. Monthly! Like we don’t have enough bills. Like we need another check arriving just to create more anxiety.

They call themselves “The Monthly Dividend Company.” The audacity. It’s a branding decision designed to prey on the financially insecure. And it’s working, apparently. People are falling for it. It’s just… infuriating. I checked the yield, 4.9%. Fine. But 31 consecutive years of raising the dividend? That’s not a sign of strength; it’s a commitment. A lifetime commitment. What if they get tired? What if the CFO just decides he needs a vacation and forgets to authorize the payment? Have they thought this through?

One of the Top REITs. Supposedly.

So, they’re a REIT. Real Estate Investment Trust. They buy properties, lease them out, and then give most of the money back to shareholders. It sounds…simple. Too simple. Like there’s a catch. They specialize in retail. Restaurants, stores… places that are constantly threatened by Amazon and, frankly, people just deciding to stay home. It’s a precarious business model. And they expect me to trust them with my money? I need a detailed risk assessment, a full psychological profile of the management team, and a guarantee that none of them have ever double-dipped a chip at a party.

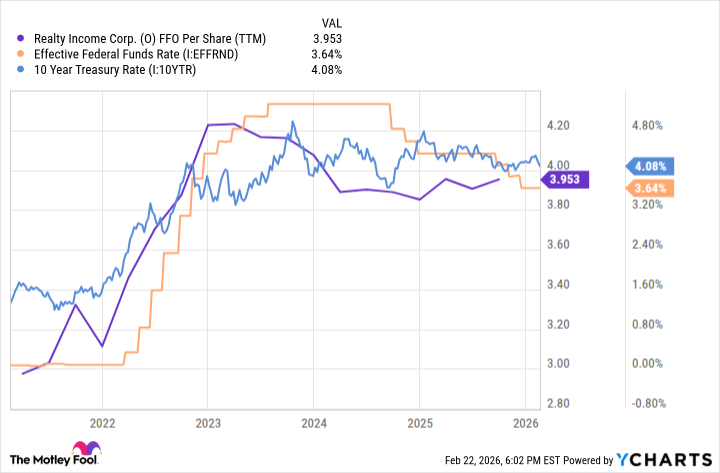

Call it a Comeback? I’d call it…something.

Pandemic hits. Of course. Everything went sideways. Tenants couldn’t pay rent. It’s not exactly breaking news. But Realty Income, they “sustained and raised the dividend.” They want a medal for doing the bare minimum? I mean, good for them, I guess. But let’s not pretend it was some heroic act of financial wizardry. Then, inflation. Naturally. The Fed starts hiking rates. Makes borrowing expensive. Like anyone needed another thing to worry about. And now per-share growth is “ticking up.” Ticking up? That’s the best they can do? It’s like they’re admitting they were in a bit of a jam and are now just… slowly recovering. It’s not a comeback; it’s a gradual crawl back to mediocrity.

Why Realty Income is Still a Long-Term Buy? I have questions.

The dividend. It’s always about the dividend, isn’t it? It’s the shiny object they dangle in front of us. 76% payout ratio. A- credit rating. Sounds…responsible. But what about the long-term viability of the entire operation? What happens when all the retail spaces are converted into self-storage units? Have they considered that? They’re expanding into casinos and data centers now? That’s like a chef suddenly deciding to become a plumber. It feels… disjointed. And Europe? Really? Europe has its own problems. They don’t need Realty Income adding to them.

15 to 16 times funds from operations. Reasonable valuation, they say. Fine. But “room for upside”? That’s just vague optimism. Reinvest the monthly dividend, they suggest. Compounding. It sounds… exhausting. It’s like they want you to become a financial workaholic. Look, I just want a little peace of mind. Is that too much to ask? I’m starting to think a savings account might be a better option. At least then I wouldn’t have to worry about some REIT making questionable decisions with my money. It’s just…a lot.

Read More

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Silver Rate Forecast

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- The Best Former NFL Players Turned Actors, Ranked

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- ONE PIECE Season 2 Confirms Sanji’s OTHER Backstory in the Live-Action

2026-02-25 12:34