It has become a commonplace observation, in these rapidly evolving times of technological advancement, that the pursuit of novelty often outstrips a sober assessment of its true merit. The recent enthusiasm surrounding Artificial Intelligence, whilst not entirely misplaced, has, one might venture, encouraged a degree of speculation rarely witnessed even in the most excitable of financial circles. Palantir Technologies, a name now frequently upon the lips of investors, has found itself, perhaps somewhat unexpectedly, at the very heart of this discourse.

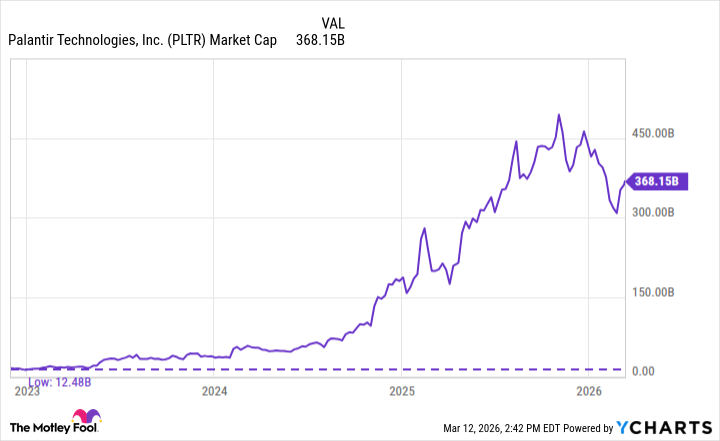

A few years past, when the company was yet to command such widespread attention, its valuation appeared, if not modest, at least proportionate to its then-established standing. To observe its current market capitalization approaching the considerable sum of four hundred billion dollars is to witness a transformation remarkable even by the standards of this volatile age. It is a circumstance which invites, nay, demands, a careful examination of the foundations upon which this considerable fortune is built.

Palantir, it is generally understood, specializes in the analysis of data. A function, it must be conceded, not entirely singular in this era of information. Many an enterprising firm now offers tools to synthesize data into neatly presented displays, a convenience which, whilst appreciated, often lacks the depth required for truly informed decision-making. The danger, one suspects, lies in mistaking a pleasing arrangement of figures for genuine insight.

It is here that Palantir distinguishes itself. Through its Foundry platform, the company constructs detailed ‘ontologies’ – a term perhaps more suited to the philosophical treatise than the balance sheet – which illuminate the intricate workings of an organization’s data. These models, moreover, are not static representations, but dynamic instruments, capable of adapting to changing circumstances and revealing the potential consequences of various actions. A most useful capability, one imagines, for those charged with the stewardship of considerable resources.

This facility has rendered Palantir a critical component for enterprises across a diverse range of sectors – from the provision of healthcare to the complexities of modern logistics, from the demands of financial services to the rigorous requirements of national defense. A testament, one might suggest, to the versatility of its design and the acumen of its creators.

The advent of ChatGPT, in late 2022, may be taken as a convenient marker for the commencement of the current wave of artificial intelligence enthusiasm. In that year, Palantir’s revenue experienced a growth of 24%, reaching $1.9 billion. The company then boasted 367 clients, a respectable number, though not, perhaps, indicative of the remarkable expansion to follow.

By 2025, revenue had surged by 56% to $4.5 billion, and the client base had expanded to 954. Such progress is, of course, gratifying to observe, but it is the nature of the contracts securing this growth which truly merits attention. The agreement with the U.S. Army, potentially worth up to $10 billion over the coming decade, is a considerable undertaking, and the company’s remaining performance obligations – exceeding $11.2 billion – represent an increase of 105% year over year. A most impressive demonstration of market confidence.

It is not surprising, therefore, that growth investors have flocked to Palantir’s standard. The question which now occupies the discerning mind is whether the shares have become unduly elevated. A high price-to-sales ratio of 87 and a price-to-earnings multiple of 241 are, at first glance, somewhat alarming. Even for a company operating in the rapidly expanding realm of software, such figures appear, one might suggest, to demand a degree of optimism bordering on the imprudent.

However, to assess Palantir solely through the lens of conventional valuation metrics is to overlook a crucial attribute. The company’s ontological approach – its ability to construct detailed models of an organization’s data – represents a genuine disruption of the established order. Whilst competitors such as Snowflake, Databricks, or Microsoft Fabric may excel in the provision of storage infrastructure, they fall short in their capacity to facilitate the creation of comprehensive data operating systems. A subtle, yet significant, distinction.

This dynamic creates unique opportunities for Palantir to expand its offerings to existing clients. A customer might begin with Foundry, and subsequently adopt Gotham or Apollo, depending on their specific needs. Against this backdrop, Palantir has cultivated a structural moat – a protective barrier against competition – which few other software providers have been able to replicate at scale. A most enviable position.

Considering the company’s robust growth over the past few years, and management’s guidance for further acceleration – anticipating a 61% increase in 2026 – one is inclined to believe that Palantir is well-positioned to continue delivering superior returns. For investors seeking to construct a durable portfolio centered around the theme of artificial intelligence, Palantir may prove to be a most suitable addition. A cautious optimism, perhaps, but one grounded in a sober assessment of the facts.

Read More

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- ONE PIECE Season 2 Confirms Sanji’s OTHER Backstory in the Live-Action

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The Best Former NFL Players Turned Actors, Ranked

- How to Do Sculptor Without a Future in KCD2 – Get 3 Sculptor’s Things

2026-03-18 22:45