Palantir Technologies, or PLTR as the chaps on Wall Street insist on abbreviating it, has been having a bit of a wobble, hasn’t it? A perfectly predictable one, naturally. One observes these tech valuations soaring to ridiculous heights, then gently descending – or, more often, plummeting – with a sort of weary inevitability. The first few months of 2026 haven’t been kind, and the market, in its infinite wisdom, appears to be questioning whether the price tag was ever justified. Rather tiresome, really.

Monday saw a rally, inching towards the $150 mark. Last year it dared to peak at over $200, a fleeting moment of optimism. Is it a ‘no-brainer’ buy below that figure? One suspects the phrase is rather overused. Let’s just say it requires a degree of…optimism, shall we?

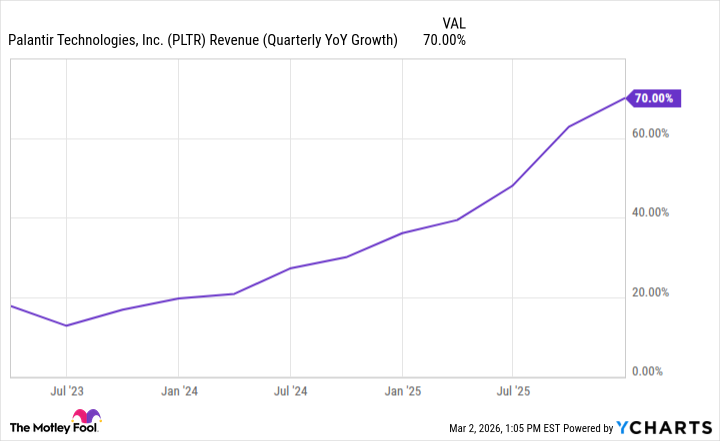

A Growth Beast, They Say

Palantir enjoys cozy relationships with the U.S. government – a most useful arrangement – and has been rather adept at leveraging artificial intelligence to make its data analytics platform more…efficient. The result? Spectacular growth, apparently. It’s become the ‘go-to’ AI stock for growth investors. One wonders if they’ve actually looked at the numbers, or are simply swept along by the prevailing hysteria.

With growth like this, the buying has been…enthusiastic. Not only have they been generating impressive numbers, but the rate of growth is accelerating. Most unusual, particularly given the rather gloomy state of the economy. Palantir has managed to distinguish itself. One must concede that. Though whether it justifies the current valuation is another matter entirely.

Cheaper, But Still Exceedingly Expensive

Palantir’s start to 2026 has been, shall we say, challenging. While cheaper than a few months ago, that doesn’t equate to a bargain. Not by a long shot. Currently, it trades at around 230 times its trailing earnings. An obscenity, frankly. It has traded at even more ludicrous multiples – 400 or 600 times earnings – but that hardly makes it sensible.

The multiple is coming down, admittedly, but it remains eye-watering. Investors should think twice. Investing at such a premium effectively prices in perfection. Any slowdown in growth – and one can’t grow at these rates indefinitely – could trigger a rather unpleasant correction. One anticipates it will, eventually.

The company has generated $4.5 billion in sales over the past year, yet its market capitalization is around $350 billion. A discount, you say? Hardly. The price would have to fall significantly further to resemble a deal. An exceedingly expensive stock, leaving one with virtually no margin for error. One suspects the market will eventually remind everyone of that simple truth.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Top 20 Dinosaur Movies, Ranked

- Silver Rate Forecast

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Top 10 Coolest Things About Invincible (Mark Grayson)

- When AI Teams Cheat: Lessons from Human Collusion

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- Unmasking falsehoods: A New Approach to AI Truthfulness

2026-03-02 23:07