Alphabet & Leverage: A Peculiar Dance

![]()

The fund now holds about 2.42% of GGLL’s assets. Which, in the grand scheme of things, isn’t much. But enough to make a ripple. The top holdings, as of the filing, looked like this:

![]()

The fund now holds about 2.42% of GGLL’s assets. Which, in the grand scheme of things, isn’t much. But enough to make a ripple. The top holdings, as of the filing, looked like this:

Let us examine the evidence, presented with a clarity befitting discerning minds:

For years, the Perseverance rover, a diligent wanderer in the ochre wilderness, has been collecting fragments of another world—air, soil, rock—holding them as one might hold precious memories. These samples, cradled within metallic test tubes, await a messenger, a return passage to Earth. MSR was to be that messenger. But the cost, a sum that echoes the vastness of space itself—eight to eleven billion dollars—proved a burden too great for the current fiscal climate. It is a familiar story: the grand vision colliding with the mundane realities of accounting.

And so, we find ourselves in the early days of 2026, with this particular bull market continuing its improbable journey. It’s a bit like watching a particularly determined snail attempt to circumnavigate the globe – statistically unlikely, but happening nonetheless. (One assumes the snail has a good travel agent.) However, even in this optimistic climate, a rather persistent fact lingers: markets, unlike certain politicians, do not ascend in a perfectly straight line. A downturn will occur. The question isn’t if, but when, and whether 2026 will be the year of reckoning.

The numbers themselves are… staggering. 7% climb this past week, according to those people who track these things (S&P Global Market Intelligence, if you’re keeping score). 3.58 billion daily active users. That’s… a lot of people scrolling. It makes me anxious just thinking about it. I tried to explain to Aunt Carol that a stock surge doesn’t necessarily mean the lizard people are thwarted, but she just kept talking about Dale’s beets.

![]()

The impact, one is assured, is minimal. The fund’s overall position saw a decrease of $50.69 million, but frankly, in the grand scheme of things, it’s hardly a cause for alarm. As of December 31st, VFLO accounted for a mere 1.0486% of Annex’s 13F AUM. One pictures the portfolio managers barely noticing its absence.

![]()

He scooped up 55,677 shares, you see, on January 22nd, 2026. A tidy sum. It’s the first time he’s bothered with this particular ETF, which is a bit like a fussy eater finally trying a new vegetable. And it represents 1.06% of his entire pile of U.S. equity sweets. A small slice, perhaps, but a promising one.

Thus, a rival enters the scene, Broadcom, a company of a different cut. Rather than offering a versatile instrument for all manner of digital feats, they propose a specialized tool, a bespoke creation tailored to a singular purpose. A curious strategy, one might think, to forgo the broad appeal for a more concentrated effort. But as any discerning theatre manager knows, a well-crafted prop, though limited in scope, can prove far more effective than a sprawling, ill-defined set.

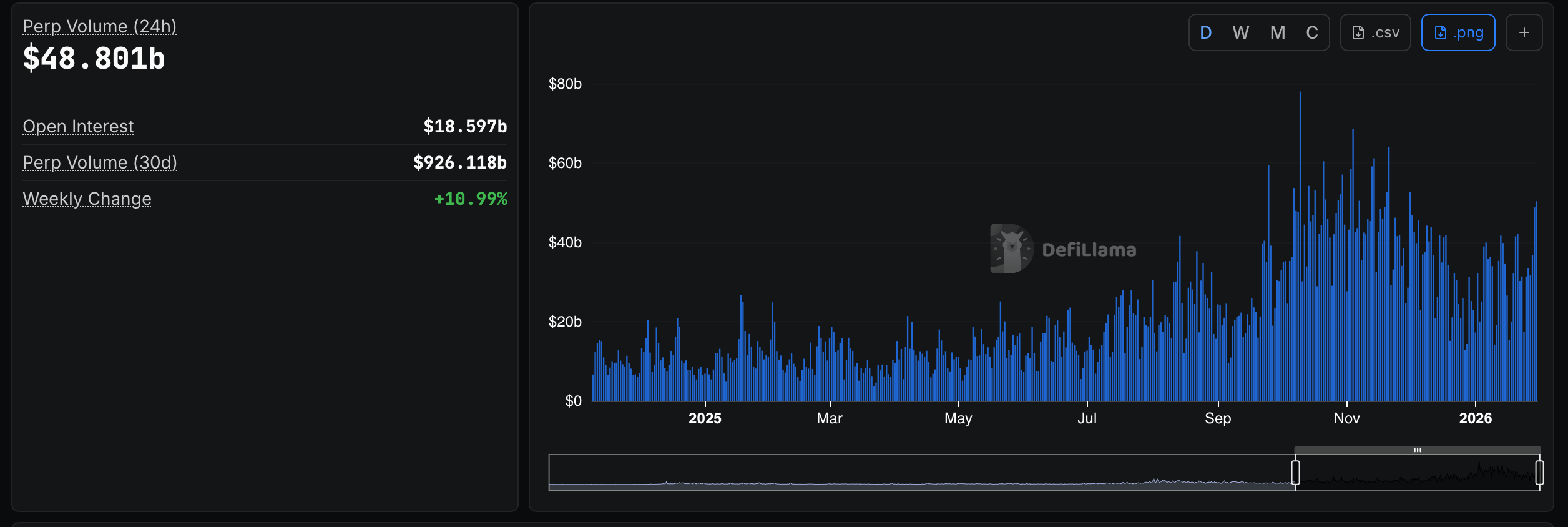

These perp DEXes, the bastard children of DeFi, allow traders to speculate on the price of assets like bitcoin and ether without the tedious formality of ownership. Imagine gambling on a racehorse’s speed without ever laying eyes on the beast-a truly modern indulgence.

![]()

Figures don’t lie, they just don’t tell the whole story. The weighted average price came in around $15.09, according to the filing. Market close on the 26th gave it a slightly different sheen. Details. They always are.