The prevailing notion that software, delivered as a subscription, is somehow impervious to the vicissitudes of fashion appears, at last, to be undergoing a necessary correction. The current panic concerning Artificial Intelligence – a term, one suspects, employed with more enthusiasm than comprehension – has, predictably, sent tremors through the valuations of the sector. One observes a distinct chill settling upon the previously overheated enthusiasm for Salesforce and its brethren. The market, belatedly, is applying a modicum of common sense.

Oracle, naturally, proclaims itself immune. Indeed, the company has, with a boldness bordering on the reckless, positioned itself not as a victim of this algorithmic upheaval, but as its very architect. A curious claim, considering its origins lie in the rather prosaic business of databases, but one must concede, they have, with considerable expenditure, built themselves a cloud. A rather large cloud, as these things go.

The transition has been… expensive. From licensing software to peddling subscriptions, and now to providing the very infrastructure upon which these digital fantasies are built, Oracle has demonstrated an admirable, if somewhat desperate, appetite for reinvention. The numbers, on the surface, are encouraging. Cloud revenue, they report, has increased by a respectable 44%. A figure which, naturally, requires a degree of scrutiny. One suspects a liberal application of accounting ingenuity.

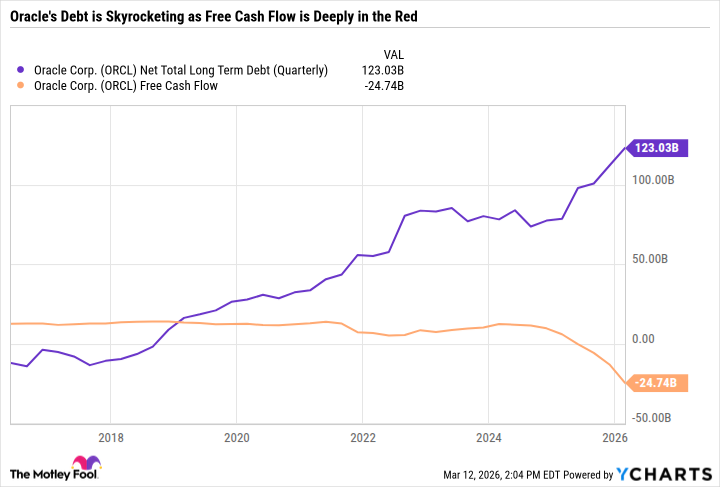

The relentless pursuit of this cloud, however, has resulted in a rather alarming accumulation of debt. Capital expenditure has soared, while free cash flow has… evaporated. A situation which, one imagines, is causing a few sleepless nights in the finance department. They speak of future revenues, of a projected $90 billion in fiscal 2027. One can only hope they are not relying on the continued gullibility of the investment community.

Oracle’s Bold Bet Comes at a High Price

The company now insists it is embedding these so-called ‘AI agents’ directly into its applications. A clever marketing ploy, certainly, but one which rather begs the question: what, precisely, do these agents do? Mike Sicilia, a co-CEO, proclaims this will not spell the death of SaaS, but rather enhance their position. A statement which, while undoubtedly intended to reassure, possesses a distinctly desperate quality. He argues these features are included as part of quarterly upgrades. A generous gesture, perhaps, or simply a means of justifying the exorbitant price tag.

The fundamental flaw in this entire narrative, as one perceives it, is the assumption that technology, in and of itself, is a panacea. Oracle has built a remarkable infrastructure, and they are adept at selling subscriptions. But the true test will be whether they can generate sufficient cash flow to service their debts and justify their extravagant ambitions. The risk, as always, is not the technology itself, but the hubris of those who wield it.

The investment thesis, therefore, hinges not on the promise of Artificial Intelligence, but on the rather more mundane matter of financial discipline. Those willing to gamble on Oracle’s ability to restore order to its balance sheet may find the stock an attractive proposition. Others, possessed of a more cautious disposition, may prefer to observe from a safe distance. One suspects a great deal of turbulence lies ahead.

Read More

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- The Best Former NFL Players Turned Actors, Ranked

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- ONE PIECE Season 2 Confirms Sanji’s OTHER Backstory in the Live-Action

2026-03-19 00:14