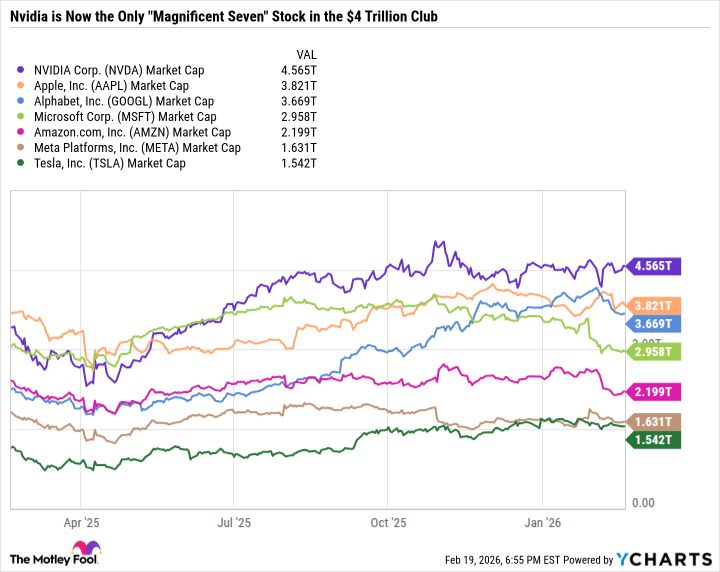

The air is thick with static, a digital dust storm swirling around the fallen empires of tech. Microsoft, once swaggering at $4 trillion, now… diminished. Alphabet and Apple, clipped wings, circling the drain. They thought they were untouchable, these silicon gods. HA! They forgot the fundamental law of the market: gravity. And now, Nvidia… Nvidia stands alone, a lone wolf howling at the moon, perched precariously on that $4 trillion precipice. It’s a beautiful, terrifying sight. A goddamn spectacle.

Four-point-five-eight trillion. That’s the number they’re chasing, the phantom valuation shimmering just beyond reach. A 12.7% tumble is all it takes to send Nvidia crashing back to Earth. And February 25th? That’s the date. The reckoning. The earnings report. The moment the vultures begin to circle. They’re saying “sell-off.” I say… HOLD ON TIGHT. This isn’t a correction; it’s a full-blown systemic breakdown in the making. A glorious, terrifying mess.

Bargain Basement Apocalypse

Valuation? Forget the P/E ratios, the forward projections. That’s accountant bullshit. Nvidia isn’t valued on earnings; it’s valued on potential. On the sheer, unadulterated need for its chips in a world hurtling toward artificial insanity. 46.5 P/E trailing? Sure. But 24.2 forward? That’s almost… reasonable. Almost. Compared to the S&P 500’s 23.6, it’s a steal. A goddamn fire sale on the future. But don’t get comfortable. This is a rigged game, and the house always wins… eventually.

The Hyperscale Hangover

Nvidia could become the biggest, most profitable company on the planet. Ninety-nine-point-two billion in net income? That’s enough to buy a small country, or at least a really good yacht. But here’s the rub: it’s all dependent on a handful of insatiable hyperscalers – Amazon, Microsoft, Google – throwing money at the problem. And these guys are changing the rules. They’re going from lean, mean, profit-generating machines to capital-intensive behemoths. Amazon planning to drop $200 billion on capex in 2026? That’s not an investment; it’s a desperate gamble. A Hail Mary pass in the fourth quarter of the digital age. Microsoft doing the same? It’s a bloodletting. A slow, agonizing drain on free cash flow.

These companies are addicted to growth, to expansion, to the illusion of control. And Nvidia is their dealer. But what happens when the supply dries up? What happens when the capex spigot gets turned off? Nvidia’s growth rate will plummet. The stock will crater. And we’ll all be left holding the bag. It’s a classic boom-and-bust cycle, played out on a global scale. And the stakes? Everything.

The Rubin Revelation

The hyperscalers are throwing money at the problem now. Nvidia is printing money. But that’s the easy part. The real test is what happens next. The next-generation Rubin chip rollout is the key. It’s the next stage in the order backlog. It’s the future. If Rubin delivers, Nvidia will be fine. If Rubin falters… well, let’s just say I’m stocking up on canned goods and ammunition. The February 25th earnings call will be crucial. Investors need to know if Rubin is on track. They need to know if Nvidia can capture the latest wave of capex. They need to know if this is a sustainable trend, or just another bubble waiting to burst.

Beyond generative AI, there’s autonomous AI, robotics, self-driving cars, edge AI. The possibilities are endless. But it all depends on execution. It all depends on Nvidia’s ability to innovate, to adapt, to stay one step ahead of the competition. And in this game, there are no second chances.

A Conviction Buy… For Now

Eighty-nine-point-eight percent of Nvidia’s revenue came from data centers last quarter. That’s a terrifying concentration of risk. A single disruption, a single supply chain issue, a single geopolitical event, could bring the whole house of cards crashing down. Nvidia needs to diversify. It needs to move beyond data centers. It needs to find new markets, new applications, new revenue streams.

Nvidia has held up better than its Magnificent Seven peers because it’s benefiting from hyperscaler spending. But that’s a short-term advantage. Investors care about the future, not the past. If 2026 marks a cyclical peak in capex spending, Nvidia will fall under pressure. But here’s the thing: the stock is still an incredible value for long-term investors. Nvidia will blow expectations out of the water in the near term. And if the stock price languishes, it will become too cheap to ignore… even amid a technical slowdown.

I don’t think Nvidia will be kicked out of the $4 trillion club. But it’s going to be a wild ride. A chaotic, unpredictable, drug-fueled descent into madness. And I, for one, wouldn’t miss it for the world. So buckle up, hold on tight, and prepare for the apocalypse. It’s going to be glorious.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Silver Rate Forecast

- Trading Crypto with AI: A New Approach to Portfolio Management

- 15 Films That Were Shot Entirely on Phones

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Thinking Before Acting: A Self-Reflective AI for Safer Autonomous Driving

2026-02-24 20:52