To predict a doubling of any stock in a year is, shall we say, ambitious. To suggest the same for the largest of companies borders on the delightfully audacious. Yet, I find myself contemplating precisely that possibility with Nvidia (NVDA +2.71%). It is, after all, far more interesting to be right than to be sensible.

What, one might ask, would it take for such a feat? Surprisingly little, as fate often favors the bold – and the well-positioned.

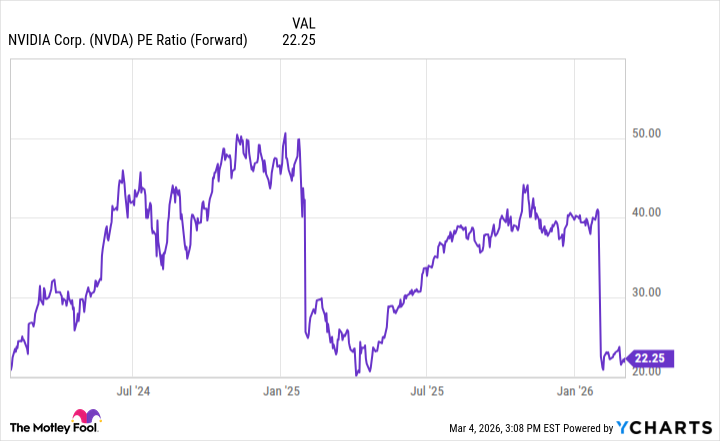

A Valuation Most Peculiar

Nvidia, you see, crafts the very engines of intelligence – those graphical processing units, or GPUs, which now underpin the burgeoning realm of artificial intelligence. Demand, as one might expect, is rather excessive, with the AI ‘hyperscalers’ – a vulgar term, but descriptive – consuming these units as quickly as they are produced. The future, therefore, appears remarkably bright – a sentiment rarely associated with financial forecasts.

Analysts, those diligent chroniclers of the obvious, project revenue growth of approximately 70% to surpass $360 billion by fiscal 2027. A profit margin exceeding 50% suggests Nvidia may soon eclipse Alphabet as the most profitable of its kind. One suspects the market, however, prefers a tragedy to a triumph.

The crucial question, naturally, concerns the longevity of this AI-driven spending spree. Various consultancies, those purveyors of expensive certainties, estimate its continuation through at least 2030. For several years, then, Nvidia’s fortunes appear secure, its products perpetually in demand. It is a most enviable position, though one rarely appreciated by the envious.

Yet, despite this promising outlook, the market seems strangely reluctant to acknowledge its worth. Over the past two years, the stock has traded between 40 and 50 times forward earnings. Currently, it languishes at a mere 22 times. A most peculiar undervaluation, wouldn’t you agree?

A doubling of the stock price requires merely a return to a valuation of 45 times forward earnings – a perfectly reasonable expectation, given the company’s prodigious growth. The difficulty, of course, lies in predicting the whims of the market – a creature far more fickle than any debutante.

The market, at present, appears rather pessimistic about the AI sector, questioning whether the vast expenditures will yield the anticipated returns. However, the ‘hyperscalers’ – those insatiable consumers of computing power – will likely continue to invest at a furious pace, recognizing that the risk of underspending far outweighs the perils of overindulgence. A most logical conclusion, though logic rarely guides the masses.

Therefore, I suspect the market will eventually rediscover Nvidia’s inherent value throughout 2026, restoring it to a more rational valuation range. This could, indeed, propel the stock to double. Even if it does not, I remain confident that it represents an excellent long-term investment – a rare opportunity to profit from both intelligence and ingenuity. After all, the truly elegant thing is to be both clever and rich.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Spotting the Loops in Autonomous Systems

- Gold Rate Forecast

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- Silver Rate Forecast

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- The Best Directors of 2025

2026-03-10 09:13