The market’s a fickle dame. Right now, it’s looking at Nvidia, and not seeing what’s right in front of its face. They’re building cathedrals of data, these hyperscalers, and Nvidia’s laying the bricks. Yet, the stock price…it’s barely a whisper. March could be the month the street wakes up, realizes this isn’t a bargain basement find, and finally pays attention. It’s a long shot, sure, but I’ve seen longer.

There haven’t been opportunities like this since the AI boom started, back in ’23. A chance to get in on the ground floor, before the whole thing gets too polished, too expensive. It’s not a guarantee, nothing ever is, but it’s a decent risk. The kind a man takes when he thinks he’s spotted something the others missed.

Nvidia’s Growth: The Numbers Don’t Lie

These hyperscalers, they’re not playing around. They’re throwing money at data centers like a sailor on shore leave. Nvidia’s the one building the engines. Last year, they spent a fortune. This year? More. They’ve announced around $650 billion in capital expenditures. That’s just the big four. The rest of the players are adding up to something substantial. By 2030, Nvidia’s betting on between three and four trillion dollars. It’s a figure that could make a man dizzy.

McKinsey & Company figures it’ll be close to seven trillion cumulative dollars by 2030. Those are the kind of numbers that stick in your gut. It isn’t a peak, it’s just the beginning. The party’s still getting started. And Nvidia’s got a front-row seat.

Investors don’t need to worry about a drop-off anytime soon. There’s enough momentum here to keep things moving for years. And who knows? Maybe the projections are low. Maybe we’ll need even more processing power than they’re predicting. That would be a good problem to have. Regardless, Nvidia’s in a sweet spot, and they’re going to capitalize on it. They always do.

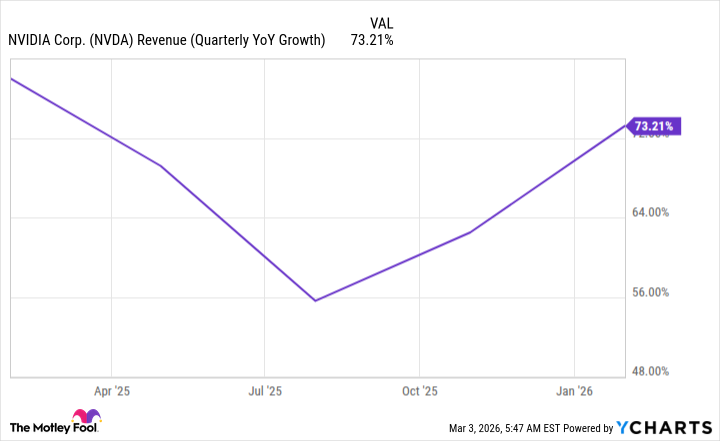

The last quarter, they saw revenue jump 73% year over year. An acceleration. The kind of growth that makes other companies envious. It’s a clean run, no smoke and mirrors. Just solid performance.

They’re projecting 77% growth for the next quarter. That’s moving fast. But the stock? It’s barely acknowledging it. It’s like the market’s got a blind spot.

Nvidia’s Stock: Still Cheap, Relatively Speaking

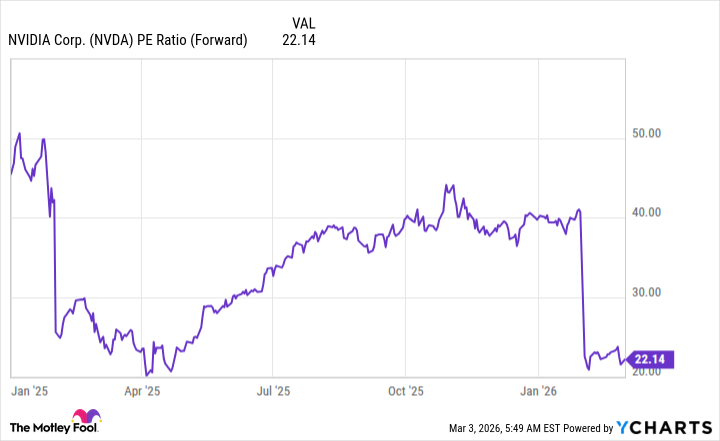

Valuing a stock is a guessing game. But the forward price-to-earnings ratio is a decent place to start. It takes future growth into account, which is important. Especially with a company like Nvidia. If growth slows down, that metric will tell you. But with this level of spending, I don’t see that happening anytime soon.

Right now, Nvidia trades at around 22.1 times forward earnings. That’s not expensive. Not for a company with this kind of potential.

The S&P 500 trades at around 21.9 times forward earnings. So, the market is valuing Nvidia like it’s just another company. That’s a mistake. A big one. And that’s why I think now is a good time to buy.

Nvidia has traded at valuations of 40 times forward earnings or more in the past. If it hits that level again this year, the stock would double. It’s a long shot, sure. But this isn’t a game for the faint of heart. This is a long-term play. And Nvidia is built to last.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Spotting the Loops in Autonomous Systems

- Gold Rate Forecast

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- Silver Rate Forecast

- The Best Directors of 2025

- Transformers Under the Microscope: What Graph Neural Networks Reveal

2026-03-09 23:14