The American energy landscape, one might observe, is undergoing a peculiar transformation – a quiet, insistent turning towards the atom. The relentless appetite of data centers, those modern cathedrals of information, demands an ever-increasing flow of electricity. Recent pronouncements, echoes of ambition from a prior administration, speak of quadrupling nuclear capacity by mid-century – a grand, if somewhat distant, vision. It is in this unfolding drama that two companies, NuScale Power and Constellation Energy, find themselves positioned – one a fledgling, brimming with promise, the other a seasoned veteran, bearing the weight of years.

Both, undeniably, offer a pathway into this burgeoning sector, yet their characters, their prospects, diverge considerably. To discern which merits a place in a discerning portfolio requires a closer examination, a weighing of potential against the immutable realities of the market.

A Tale of Two Approaches

Constellation Energy, a name steeped in the history of power generation, presents itself as a comprehensive provider, a diversified estate encompassing nuclear, gas, geothermal, wind, hydro, and solar. Its recent acquisition of Calpine further solidifies its position as a dominant force, boasting a capacity exceeding fifty-five gigawatts. These are the established reactors, the familiar turbines humming with the predictable rhythm of conventional nuclear fission.

NuScale Power, in contrast, represents a different order of things – a venture into the realm of Small Modular Reactors, or SMRs. These are not the colossal structures of yesteryear, but compact, scalable units, promising faster construction, reduced costs, and greater flexibility. It is a technology still in its infancy, granted regulatory approval, but yet to fully blossom. NuScale, in essence, is a seed, while Constellation is a mature tree, its roots deeply entrenched.

NuScale: The Allure of the New, and its Shadows

It is, perhaps, natural to be drawn to the promise of innovation. NuScale, with its relatively modest market capitalization, possesses the potential for exponential growth. Yet, such potential is invariably accompanied by a corresponding degree of risk. The company, still years from meaningful revenue, is currently engaged in a protracted dance with reality. Its initial contract – six SMR modules for a Romanian facility – will not bear fruit until 2033, a date that seems to recede further with each passing season. The agreement with the Tennessee Valley Authority, while promising, remains shrouded in the vagueness characteristic of long-term infrastructure projects.

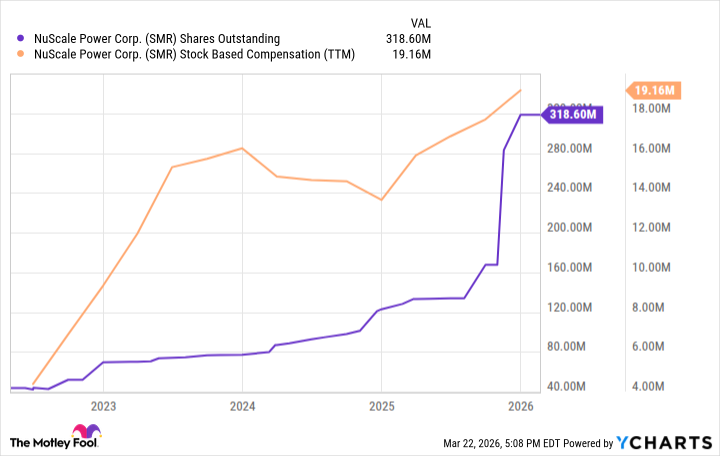

The nuclear industry, one must remember, operates on a timescale far removed from the frenetic pace of the digital world. Red tape, regulatory hurdles, and the sheer complexity of the technology conspire to slow progress to a glacial crawl. Furthermore, NuScale, in its pursuit of growth, is resorting to the familiar practice of diluting shareholder value through stock-based compensation and continued operational losses. The recent sale of nearly forty million shares, while raising significant capital, casts a long shadow over the company’s future prospects. One cannot help but wonder if the initial enthusiasm will give way to a more sober assessment of the challenges ahead.

The valuation, while not exorbitant, is not entirely comforting either. NuScale remains years away from generating substantial revenue, and the path to profitability is fraught with uncertainty. The company must not only become a leader in the nuclear industry but also justify the current level of risk, a task that seems increasingly daunting.

Constellation: The Steadfast Anchor

In contrast to NuScale’s speculative allure, Constellation Energy offers a degree of stability that is increasingly rare in the modern market. The company has already built its nuclear fleet, navigated the regulatory labyrinth, and established a solid foundation for future growth. It can not only maintain its existing reactors but also upgrade, expand, or even revive those that have fallen into disuse – a process that is likely to be far faster and more efficient than building entirely new facilities.

The recent agreements with Microsoft and Meta Platforms to supply electricity for their data centers are a testament to Constellation’s reliability and its ability to meet the demands of a rapidly growing market. These contracts, scheduled to come online by 2028, provide a clear indication of the company’s future revenue stream.

Unlike NuScale, Constellation is already a profitable, entrenched business. Analysts predict annual earnings growth of 15% over the next three to five years, a respectable rate that suggests a degree of stability and predictability. Furthermore, the company pays a dividend yielding 0.6%, with plans to increase it by 10% annually – a rate that would double dividend income every seven years. A modest return, perhaps, but one that is grounded in reality.

All things considered, investors can reasonably expect steady dividend growth and double-digit annualized total returns from Constellation Energy over the long term. It will not deliver overnight riches, but it offers a degree of security and predictability that is increasingly rare in the modern market.

While NuScale’s early lead in SMR design is undeniably appealing, it is difficult to justify the opportunity cost of holding a risky, speculative stock over a proven, reliable leader like Constellation Energy. The allure of the new is strong, but the wisdom of experience should not be underestimated.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Top 20 Dinosaur Movies, Ranked

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Gold Rate Forecast

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

- Top 10 Coolest Things About Invincible (Mark Grayson)

- Celebs Who Narrowly Escaped The 9/11 Attacks

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

2026-03-25 00:34