Author: Denis Avetisyan

A new framework directly translates financial news into trading decisions, demonstrating improved performance by focusing on the semantic meaning of events and their market impact.

Janus-Q employs reinforcement learning and large language models for end-to-end event-driven trading, achieving abnormal returns through hierarchical-gated reward modeling.

Traditional financial modeling often struggles to fully capture the impact of discrete events embedded within news flow. This limitation motivates the work presented in ‘Janus-Q: End-to-End Event-Driven Trading via Hierarchical-Gated Reward Modeling’, which introduces a novel framework that directly links financial news events to trading decisions. By unifying event-centric data construction with reinforcement learning guided by a Hierarchical Gated Reward Model, Janus-Q demonstrably improves trading performance, achieving up to a 102.0% increase in the Sharpe Ratio compared to benchmark strategies. Could this event-driven approach represent a paradigm shift in leveraging textual information for more robust and profitable algorithmic trading?

Beyond Reactive Systems: Embracing Event-Driven Intelligence

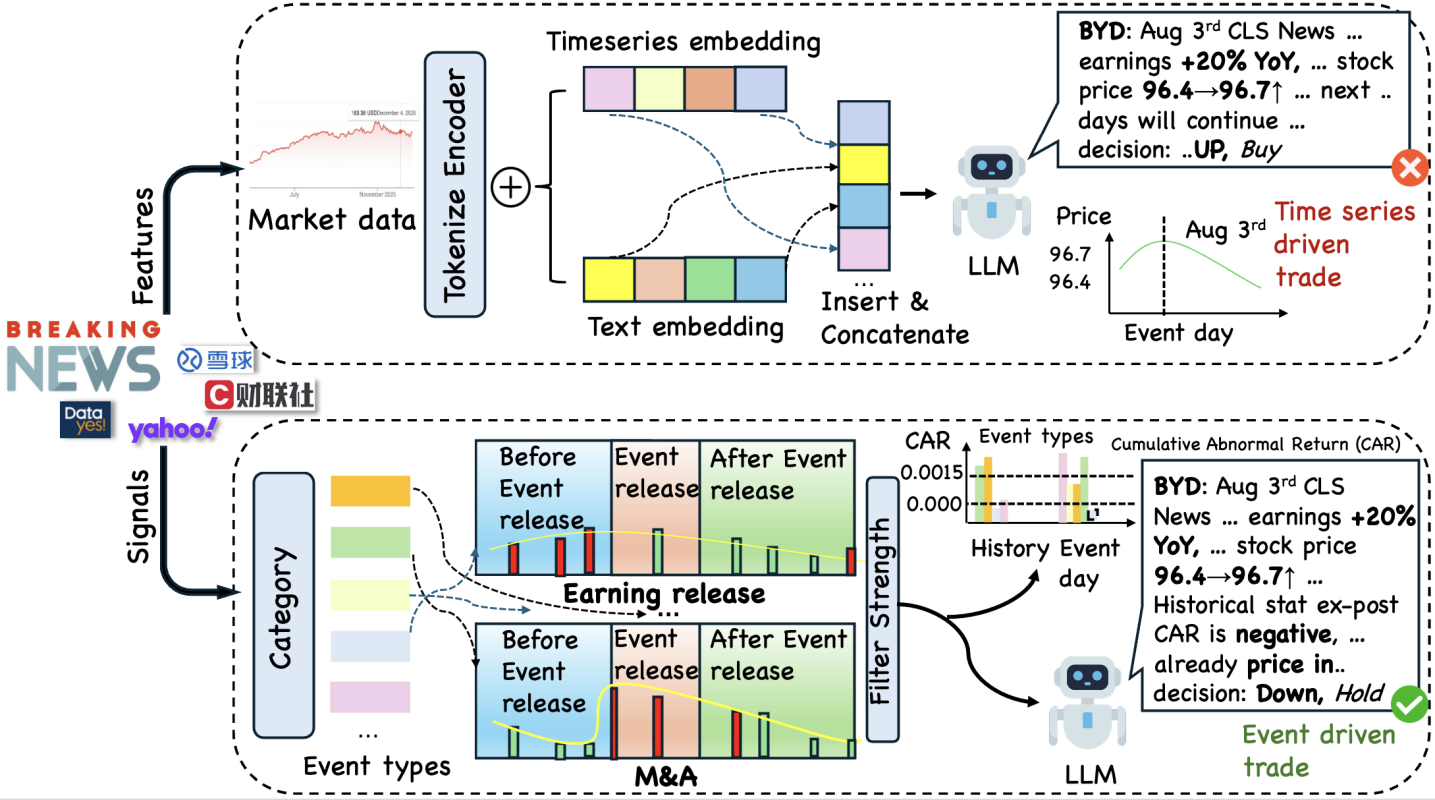

Conventional trading methodologies, heavily reliant on time-series analysis, frequently demonstrate an inability to effectively incorporate the immediate and complex data delivered by contemporary news events. These strategies excel at identifying patterns within historical price movements, but often lag when confronted with novel information-a critical shortcoming in today’s fast-paced markets. The inherent delay in processing news and quantifying its impact means that by the time a time-series model registers a change, a significant portion of the opportunity-or risk-may have already passed. This limitation is particularly pronounced during periods of high volatility or unexpected global events, where traditional indicators can provide misleading signals, hindering a trader’s ability to react decisively and capitalize on emerging trends. Consequently, a dependence on purely historical data leaves traders vulnerable and potentially unable to navigate the intricacies of a constantly evolving financial landscape.

Traditional analytical techniques frequently stumble when attempting to quantify the effects of unforeseen events on financial markets. While historical data excels at identifying patterns within established trends, it provides limited insight into the complex, often nuanced, consequences of breaking news or unexpected occurrences. This inability to accurately discern the true impact of such events leads to miscalculated risk assessments and, consequently, missed opportunities for profitable trades. Algorithms relying solely on past price movements may interpret initial market reactions as genuine signals, only to be corrected as the full scope of an event becomes clear – exposing traders to unnecessary volatility and potential losses. Ultimately, a failure to move beyond purely quantitative analysis restricts a trader’s ability to capitalize on the information-rich environment of modern financial markets.

Conventional trading methodologies, heavily reliant on interpreting historical price movements, increasingly prove inadequate in today’s swiftly evolving markets. These reactive systems operate on what has already happened, failing to anticipate the impact of unfolding events before they are reflected in price data. Consequently, opportunities are often lost, and potential risks are amplified as traders respond to consequences rather than predicting them. A successful approach necessitates a shift towards event-driven strategies – systems designed to proactively assess the likely market impact of news, announcements, and global occurrences. By focusing on the causative factors shaping market behavior, rather than simply reacting to the resulting price changes, traders can position themselves to capitalize on emerging trends and mitigate unforeseen volatility, ultimately achieving a more informed and potentially profitable trading experience.

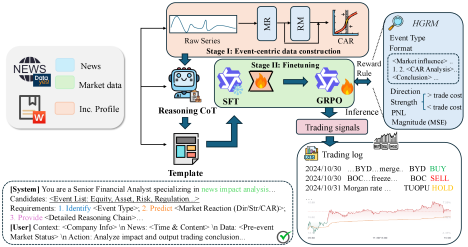

Janus-Q: An Event-Centric Framework for Financial Decision-Making

Janus-Q employs a two-stage framework that fundamentally shifts the focus of financial decision-making from traditional feature-based analysis to event-centric processing. Instead of treating news reports as supplementary data points, the system identifies and prioritizes discrete financial news events as the primary units driving investment decisions. This approach contrasts with conventional methodologies where news is often incorporated as an auxiliary feature alongside established technical indicators and historical price data. By directly analyzing the content and implications of specific events – such as earnings announcements, regulatory changes, or macroeconomic releases – Janus-Q aims to provide a more immediate and accurate assessment of market impact, enabling quicker and potentially more profitable trading strategies.

The Janus-Q framework utilizes Large Language Models (LLMs) to process unstructured financial news data, extracting key event information including event type, involved entities, and sentiment. These LLMs are employed to parse news articles, regulatory filings, and social media feeds, converting textual data into structured event representations. This process enables the system to identify and categorize events relevant to financial markets, such as earnings announcements, mergers and acquisitions, and macroeconomic releases. The rapid interpretation of this event data allows for timely assessment of potential market impact, facilitating quicker responses than traditional methods reliant on quantitative data alone. The LLM’s output serves as the primary input for the subsequent reinforcement learning stage, driving trading decisions based on real-time event analysis.

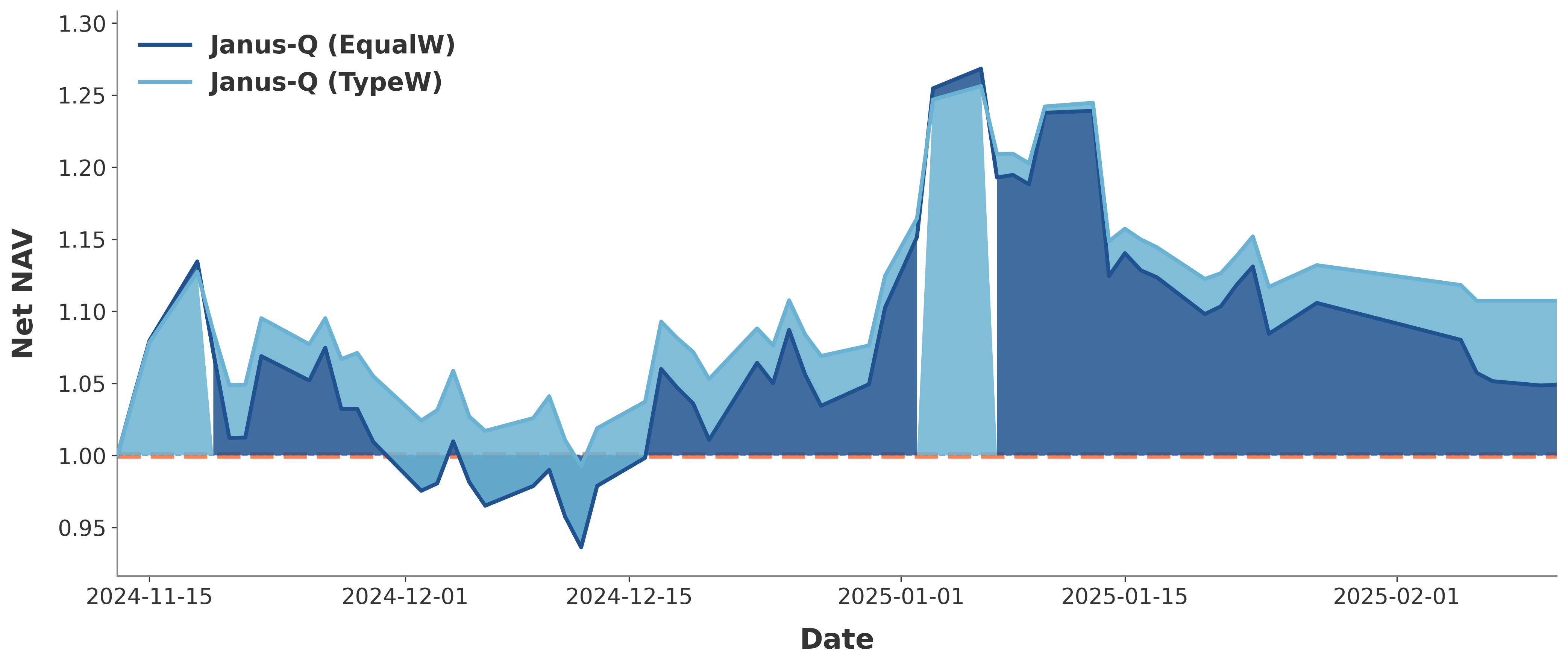

Janus-Q employs Reinforcement Learning (RL) to dynamically refine trading strategies triggered by event-driven signals. The RL agent is trained to maximize cumulative returns based on the interpreted impact of financial news events. Evaluation of the system demonstrated a Sharpe Ratio of 1.3088, a metric indicating risk-adjusted return; values exceeding 1.0 are generally considered acceptable, and a ratio of 1.3088 signifies strong performance relative to the risk undertaken. This optimization process allows the system to adapt to changing market conditions and capitalize on event-driven opportunities with a quantifiable level of efficiency.

Deconstructing Performance: The Hierarchical Gated Reward Model

The Janus-Q agent utilizes a Hierarchical Gated Reward Model to dissect overall reward signals into three distinct, quantifiable components. Event-type consistency assesses the agent’s adherence to expected event sequences within the environment. Directional accuracy measures the correctness of the agent’s chosen actions relative to optimal navigation. Finally, return-magnitude reliability evaluates the consistency and predictability of the rewards obtained following specific actions. This decomposition allows for granular feedback during training, enabling the agent to optimize each component individually and improve overall performance by identifying and correcting specific weaknesses in its decision-making process.

Supervised Fine-Tuning (SFT) serves as a critical pre-training step in Janus-Q, establishing a foundational level of reasoning capability before the application of Reinforcement Learning (RL). This process involves training the model on a dataset of expert demonstrations, allowing it to learn a policy that mimics desired behaviors. By initially stabilizing the model’s responses through supervised learning, SFT reduces the variance inherent in RL algorithms and accelerates the learning process. This stabilization is demonstrated by improved consistency in decision-making and a reduction in the exploration required to achieve optimal performance, ultimately leading to more reliable and predictable outcomes.

The agent’s performance is directly correlated to its ability to discern impactful events within a given scenario, facilitated by the refined reward system. This system enables the agent to prioritize actions based on their contribution to overall success, leading to improved decision-making and a demonstrable 17.5% increase in Direction Accuracy when compared to alternative methodologies. This improvement indicates a heightened ability to correctly identify and react to crucial environmental changes, ultimately optimizing navigational performance and task completion rates.

Validating the Approach: Performance and Event Isolation

Janus-Q’s event-driven trading strategy delivers demonstrably superior performance, as evidenced by a Sharpe Ratio of 1.3088. This metric, a key indicator of risk-adjusted return, significantly exceeds that of competing strategies; the runner-up achieved a ratio over 102.0% lower. Beyond simply maximizing returns, the system also exhibits strong directional accuracy, consistently predicting market movements following specific events. This combination of high Sharpe Ratio and reliable directional prediction underscores the effectiveness of isolating and capitalizing on event-driven abnormal returns, suggesting a robust and potentially valuable approach to automated trading.

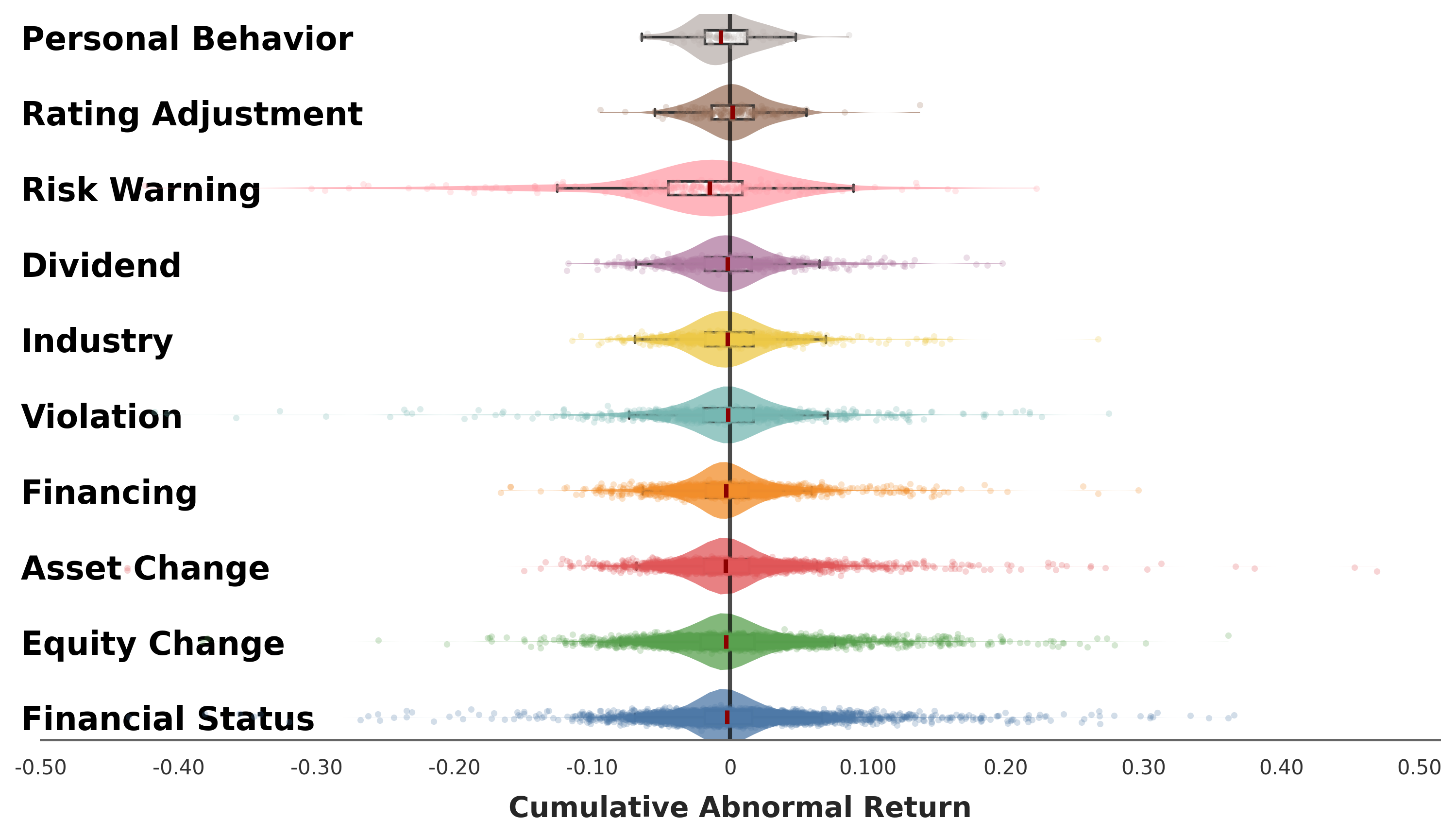

Rigorous validation of the system’s capacity to pinpoint event-driven abnormal returns involved employing sophisticated models, notably CNE5, a technique commonly used to detect nuanced shifts in complex datasets. This analysis didn’t simply confirm the presence of unusual activity following specific events; it demonstrated the system’s ability to isolate these returns from broader market noise. By leveraging CNE5, researchers could assess the statistical significance of observed anomalies, establishing that the identified returns weren’t merely random fluctuations. The successful application of this model underscores the system’s reliability in identifying genuine, event-correlated market reactions, and provides a robust foundation for capitalizing on these short-lived opportunities.

A comprehensive event dataset serves as the bedrock for understanding how markets respond to diverse occurrences, significantly bolstering the model’s predictive capabilities. Analysis reveals a marked improvement in predicting cumulative abnormal returns, demonstrated by an 18.3% reduction in Mean Absolute Error (MAE) when compared to the most effective time-aware model. This predictive power extends even further, exceeding the performance of leading financial Large Language Models (LLMs) by a substantial 50.6% reduction in MAE, suggesting the model’s nuanced understanding of event-driven market dynamics surpasses that of current benchmark approaches and establishes a new standard for accuracy in predicting market reactions.

The Future of Trading: Proactive Intelligence and Adaptive Systems

Traditional trading strategies heavily rely on analyzing historical time-series data – essentially, looking backward to predict the future. However, a shift towards proactive intelligence recognizes the limitations of this reactive approach. By incorporating diverse data streams – encompassing news sentiment, social media trends, and macroeconomic indicators – alongside advanced machine learning algorithms, it becomes possible to anticipate market shifts before they are reflected in price charts. This isn’t simply about faster reaction times; it’s about identifying causal factors and predicting potential price movements with greater accuracy. The core principle involves moving from correlation – observing that two things happen together – to causation, understanding why something happens, allowing for strategies that capitalize on emerging opportunities and mitigate unforeseen risks before they fully materialize. This proactive stance represents a fundamental evolution in trading, potentially unlocking substantial gains and improved portfolio resilience in increasingly volatile markets.

Accurate assessment of market impact stemming from diverse event types represents a paradigm shift in financial strategy. Traditional models often treat events – such as economic reports, geopolitical shifts, or even social media trends – as external shocks; however, quantifying how these events specifically reshape market dynamics allows for precise risk mitigation. This granular understanding moves beyond broad hedging strategies, enabling portfolio optimization tailored to the anticipated effects of each event. For instance, anticipating the impact of a Federal Reserve announcement on specific asset classes – rather than simply bracing for overall volatility – allows traders to proactively adjust positions, capitalizing on nuanced price movements and minimizing potential losses. Consequently, sophisticated event impact analysis isn’t merely about predicting what will happen, but understanding how it will happen, and positioning investments accordingly to achieve superior risk-adjusted returns.

The escalating velocity and interconnectedness of global markets demand a shift from traditional trading methodologies. Event-driven frameworks, such as the Janus-Q system, represent a vital progression, enabling the interpretation of unstructured data – news, social media, economic releases – and its translation into actionable trading signals. These systems don’t simply react to price changes; they attempt to understand the causal factors driving those changes, allowing for preemptive positioning and potentially superior risk-adjusted returns. Continued refinement of these frameworks, focusing on enhanced natural language processing, improved causal inference, and the ability to adapt to novel event types, is no longer simply advantageous-it is becoming essential for sustained success in an increasingly turbulent financial environment. The ability to quickly and accurately process information from diverse sources and distill it into trading intelligence will define the leading edge of financial innovation.

The pursuit of Janus-Q exemplifies how structure dictates behavior within complex systems. The framework’s hierarchical-gated reward modeling isn’t merely about processing financial news; it’s about establishing a clear mapping between event semantics and resultant trading actions. As Vinton Cerf once stated, “Any sufficiently advanced technology is indistinguishable from magic.” Janus-Q, through its integration of large language models and reinforcement learning, achieves a similar effect – transforming unstructured news events into quantifiable trading signals. The system’s performance, demonstrating abnormal returns, underscores that meticulous design, prioritizing event understanding and market impact analysis, yields emergent behavior far exceeding simpler approaches. It is the clarity of this structure that enables the ‘magic’ of automated, event-driven trading.

The Road Ahead

The elegance of Janus-Q lies in its directness – mapping event semantics to action. Yet, the market, as always, resists simple solutions. The framework’s current reliance on news events, while demonstrably effective, begs the question of informational completeness. True understanding requires acknowledging the signals not captured, the whispers beyond the headlines. Future iterations should explore the integration of alternative data streams – order book dynamics, social sentiment, even the subtle shifts in analyst reports – not as additional features, but as fundamental components of the event definition itself.

A persistent challenge remains the quantification of ‘market impact.’ Current models, including this one, approximate this effect – a necessary simplification, perhaps, but a simplification nonetheless. A more holistic view would necessitate a deeper engagement with agent-based modeling, simulating the complex interplay of heterogeneous actors and their reactions to information. If a design feels clever, it is probably fragile; therefore, the pursuit of parsimony should not preclude a rigorous examination of systemic effects.

Ultimately, the success of any trading system hinges not on outsmarting the market, but on accurately reflecting its underlying structure. Janus-Q offers a promising step towards this goal, but the path forward demands a continued commitment to simplicity, clarity, and a healthy skepticism towards overly complex solutions. The market will always find a way to expose the flaws in any model; the art lies in designing systems that reveal those flaws quickly and cleanly.

Original article: https://arxiv.org/pdf/2602.19919.pdf

Contact the author: https://www.linkedin.com/in/avetisyan/

See also:

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- Trading Crypto with AI: A New Approach to Portfolio Management

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 15 Films That Were Shot Entirely on Phones

2026-02-24 15:07