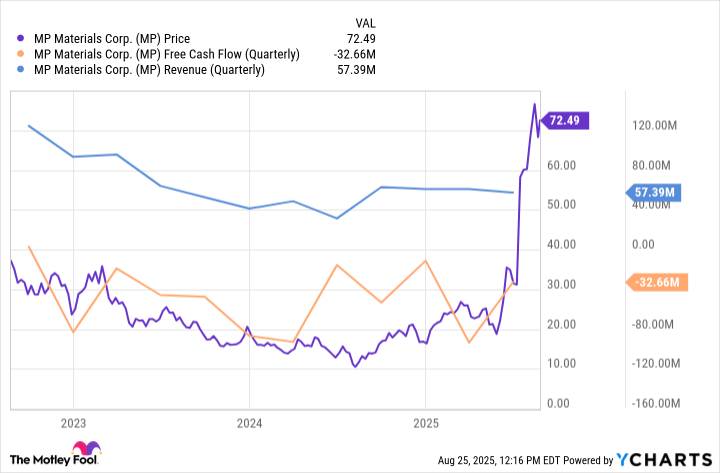

MP Materials (MP), that most improbable of equities, has enjoyed a performance in 2025 that would make a Victorian inventor weep into his monocle. A $10,000 wager placed at the year’s outset would now yield $34,300-assuming one possessed the temerity to trust a company whose primary output is a substance with the allure of wet cardboard. Yet here we are, gazing at a 343% ascent, as if the market has been seduced by the promise of neodymium.

One wonders what alchemy transmutes such a proposition into a speculative paragon. Is it the DoD’s paternalistic largesse, Apple’s newfound moral rigor, or merely the collective delusion of investors who mistake geopolitics for profit? Perhaps all three, though history suggests that those who conflate strategy with success often end up buried in their own hubris.

MP Materials: America’s Rare-Earth Champion (or Victim?)

MP Materials, proprietor of California’s Mountain Pass mine-the nation’s sole operational rare-earth facility-is a creature both singular and absurd. Its stock in trade, those “rare” elements so vital to magnets, EV motors, and the occasional missile, is less a commodity than a geopolitical talisman. One might suppose that owning a mine in such a position is akin to possessing a monocle in a world of sunglasses: an affectation of indispensability.

Rare-earth elements, despite their name, are neither scarce nor particularly rare. Their true scarcity lies in the economic absurdity of extracting them. Only a handful of nations-China, Brazil, Australia-have mastered the art of turning geology into cash, while the U.S., with its 1.9 million metric tons, remains a mere spectator in its own supply chain. A state of affairs so lamentable it would have made Waugh’s Lord Marchmain wince.

China, that industrial octopus, now controls 70% of extraction and 90% of processing. The U.S., in its infinite wisdom, imported 80% of its rare-earths in 2024, 77% from its eastern rival. A dependency so profound it reads like a satire of national self-sufficiency.

Enter the Department of Defense, with its $400 million stake in MP and a price guarantee of $110 per kilogram of NdPr oxide-a sum twice the current market rate. One imagines the Pentagon’s accountants weeping into their spreadsheets, while MP’s shareholders clinked glasses. The DoD, it seems, has become the ultimate venture capitalist, trading bullets for bonds.

Such subsidies, of course, are a double-edged sword. They provide comfort, yes, but also the illusion of permanence. A company reliant on Uncle Sam’s largesse is a company dancing on a tightrope strung between patriotism and solvency.

Partnerships: The New Alchemy

MP’s recent alliances-Apple, General Motors, and JPMorgan-read like a boardroom farce. Apple, that apostle of sleek design, now funds a mine to extract the very materials that will one day rust in its iPhones. General Motors, once the titan of Detroit, has become MP’s eager pupil in magnet production. And JPMorgan, that arch-capitalist, has pledged $1 billion to build a factory that may never yield a profit.

The Fort Worth plant, with its 1,000-ton annual capacity, is a modest beginning. Yet it pales against the orders already booked. One might compare it to a chef who promises a feast but owns only a ladle. The 10X Facility, if completed by 2028, could swell capacity tenfold-but at what cost? Capital-intensive projects are the graveyard of many a bullish forecast.

MP’s cash burn is relentless, its production capacity lagging. And then there is the matter of Shenghe Resources, that erstwhile Chinese partner, now severed like a bad engagement. A divorce, perhaps, but one that leaves MP clutching a bag of concentrate and no one to take it off its hands.

The Illusion of Certainty

MP Materials is a company teetering between promise and peril. Its tailwinds are strong-government contracts, corporate partnerships, and a world desperate for magnets. Yet its sails are made of tissue paper. Scaling up requires not just capital, but a suspension of disbelief. Can it deliver 10,000 tons by 2028? Perhaps. But can it do so without becoming a cautionary tale of overreach and underperformance?

For the investor, the question is not whether MP can succeed, but whether the market has priced in its inevitable failures. At today’s valuation, it is a bet on the impossible. To call it a “set you up for life” play is to ignore the long odds and the short memory of markets. Still, in the theater of speculation, even the most implausible acts find an audience. 🤔

Read More

- Games That Faced Bans in Countries Over Political Themes

- Gold Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Silver Rate Forecast

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- The Best Directors of 2025

- The Best Former NFL Players Turned Actors, Ranked

2025-08-28 15:33