![]()

Microsoft (MSFT 0.43%) maintains a position as a leading provider of cloud computing infrastructure, servicing a broad customer base through its Azure platform. The company’s strategic emphasis on artificial intelligence (AI) is evident in the integration of its Copilot assistant across key software suites. However, recent market performance suggests a degree of investor recalibration, necessitating a thorough examination of underlying fundamentals.

Copilot Adoption and Monetization

While Copilot is offered as a standard feature within Windows and Bing, its monetization strategy centers on subscription access within the Microsoft 365 suite. Current penetration rates, at approximately 3.7% of the 400 million 365 licenses, appear modest. Though year-over-year growth of 160% is noted, the trajectory of sustained adoption remains a key variable in assessing future revenue streams. The tripling of organizations with over 35,000 Copilot licenses, coupled with a tenfold increase in daily active users, indicates a potential for accelerating uptake within enterprise clients, contingent upon demonstrated return on investment.

Azure Growth and Capital Allocation

The expansion of Azure necessitates substantial capital expenditure in data center infrastructure. As of December 31, Microsoft reported a $625 billion order backlog, representing a 110% year-over-year increase. Over the preceding four quarters, the company invested $118 billion in expanding capacity. A significant portion of this backlog—approximately 45%, or $281 billion—is attributable to OpenAI. This concentration introduces a degree of dependency, given OpenAI’s current revenue profile and its ongoing capital requirements. While demand for Azure remains robust, with revenue growth exceeding 39% in the last three quarters, the sustainability of this pace is contingent upon effective capital allocation and the diversification of the customer base.

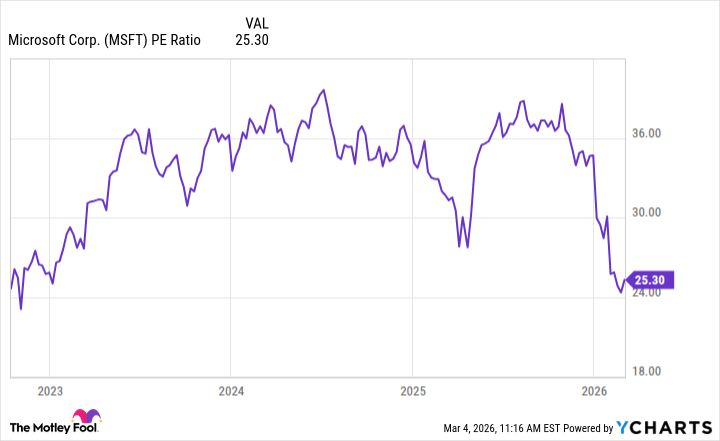

Valuation and Peer Comparison

Microsoft’s current earnings per share of $15.98 translate to a price-to-earnings (P/E) ratio of 25.3. This represents the lowest valuation in over three years. The stock is currently trading at a discount to the Nasdaq-100, which has a P/E ratio of 31.8, and is approaching the P/E ratio of the S&P 500 (^GSPC 1.33%), which currently trades at 24.7. While a premium valuation is often warranted for companies exhibiting consistent growth and profitability, the current discrepancy suggests a potential undervaluation.

A cautious approach to assessing Microsoft’s current valuation is warranted. The company’s historical performance and market position justify a degree of premium. However, the extent to which this premium is justified requires ongoing monitoring of key performance indicators, including revenue growth, profitability margins, and capital allocation efficiency.

Opportunities to acquire shares of Microsoft at a relatively attractive price are infrequent. However, investors should conduct thorough due diligence and consider the aforementioned factors before making any investment decisions.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- Silver Rate Forecast

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- The Best Directors of 2025

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

2026-03-08 12:02