MSFT”>

During the earnings call, Microsoft’s CFO, Amy Hood, rather delicately pointed out that investors seem to be drawing a “direct correlation” between capital expenditure and Azure’s revenue. A diplomatic way of saying they’re questioning the return on investment in all this AI infrastructure. One can hardly blame them. Throwing money at a problem rarely solves it, though it does provide employment for accountants.

A Buying Opportunity, Perhaps?

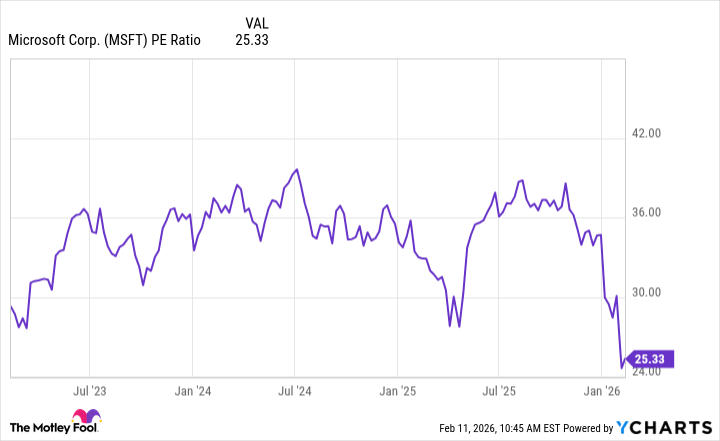

From a purely valuation perspective, Microsoft hasn’t looked this… accessible since the dawn of this AI mania. A price-to-earnings multiple of 25 is hovering near a three-year low. One might even call it a bargain. Though, naturally, one wouldn’t want to appear too enthusiastic.

And the consensus price target amongst the sell-side analysts is $596, implying a rather substantial 48% upside. Wall Street, it seems, remains bullish on Microsoft’s AI ambitions. One trusts they have done their due diligence, of course. Though one does harbor certain reservations regarding the collective wisdom of the financial community.

Given the attractive valuation and potential upside, buying Microsoft stock hand over fist might seem tempting. However, there’s always a degree of execution risk. This infrastructure build-out requires careful management, and there’s no guarantee it will translate into tangible benefits for Azure, or indeed, other parts of the Microsoft ecosystem. One prefers to maintain a degree of skepticism.

Therefore, one would cautiously buy the dip, but wouldn’t mortgage the manor. The sell-off seems rather overblown, and taking advantage of the depressed price action could prove to be a savvy move in the long run. Though, naturally, one wouldn’t want to be caught with one’s trousers down. A little prudence never goes amiss.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- Silver Rate Forecast

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- The Best Directors of 2025

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

2026-02-15 15:32