The matter of Micron Technology (MU 6.68%) has presented itself, as these things invariably do, through the labyrinthine channels of data center architecture. It is a component manufacturer, ostensibly, though the term feels insufficient when considering the sheer volume of calculations – and, by extension, dependencies – that rest upon its high-bandwidth memory (HBM). Nvidia and Advanced Micro Devices, the acknowledged arbiters of graphical processing, source this HBM from Micron, a relationship that resembles, more than anything, a complex and largely unacknowledged contract with an unseen authority.

The current demand, described as ‘astronomical’ by those in positions to quantify such things, feels less like organic growth and more like a frantic accumulation. Revenue and earnings, predictably, have surged, and the stock has experienced a… fluctuation. 323% in twelve months. A figure that, upon closer inspection, appears not as a triumph of enterprise, but as a temporary reprieve from the inevitable entropy of the market. One anticipates a correction, though the timing, as always, remains obscured by the fog of speculation.

The Essential Fragility of Memory

The operation of these ‘artificial intelligences’ – a phrase that carries an unsettling weight – is predicated upon a constant, uninterrupted flow of data. The GPUs require it, demand it, as a patient demands sustenance. HBM functions as a holding reservoir, a temporary reprieve from the infinite calculations. A deficiency in capacity creates a bottleneck, a momentary pause in the processing, a silence that echoes with the potential for systemic failure. It is a precarious arrangement, this reliance on a single component. A single point of failure, if you will, in a system designed to be infallible.

Micron’s HBM3E, we are told, offers a 50% increase in capacity while simultaneously reducing energy consumption by 30%. This is presented as a benefit, of course, but it feels more like a temporary mitigation of an inherent instability. The forthcoming HBM4E, promising a further 60% increase in capacity and a 20% reduction in energy, merely postpones the inevitable. It is a cycle of incremental improvements, each one masking the underlying fragility of the entire system. This new iteration is slated to power Nvidia’s Vera Rubin chips, which, according to projections, will be the most powerful in the world. A claim that feels less like a statement of fact and more like a bureaucratic decree.

The entirety of Micron’s 2026 data center HBM supply is, predictably, already sold out. The market, currently valued at $35 billion, is projected to grow by 40% annually, reaching $100 billion. These figures are presented as evidence of success, but they feel less like a triumph of enterprise and more like a confirmation of our collective dependence on these increasingly complex and opaque systems.

The Eighteenth of March: A Date of Uncertain Significance

Micron’s fiscal second quarter concluded at the end of February, and the results are scheduled for release on the eighteenth of March. Preliminary guidance suggests a record revenue of $18.7 billion, a 132% increase year-over-year. This acceleration, from a previous growth rate of 56%, feels less like a sign of health and more like a desperate attempt to maintain momentum. The cloud memory segment, responsible for data center HBM sales, nearly doubled year-over-year to $5.3 billion. One anticipates a further increase, though the precise figure remains, as always, shrouded in uncertainty.

Earnings are expected to explode, increasing by 480% year-over-year to $8.19 per share. This, too, represents an acceleration, from a previous growth rate of 175%. These numbers, while impressive on the surface, feel less like a validation of Micron’s business model and more like a temporary distortion of the market. Earnings, after all, are merely a reflection of past performance, and the future, as always, remains uncertain. The market, predictably, will respond to these figures, and the resulting fluctuations will, inevitably, dictate the fate of Micron shareholders.

The Question of Ascent: How Much Higher?

The semiconductor industry, historically cyclical, operates on a predictable pattern of expansion and contraction. The advent of artificial intelligence, however, has disrupted this pattern, shortening the upgrade cycle to twelve months, or less. Data center operators are, therefore, in a perpetual state of expenditure. This feels less like a sign of economic health and more like a symptom of a deeper, more fundamental instability.

Nvidia’s CEO, Jensen Huang, believes data center operators will spend up to $4 trillion annually on AI infrastructure by 2030. A staggering figure, and one that feels, upon closer inspection, less like a realistic projection and more like a self-fulfilling prophecy. A significant portion of this expenditure will flow to chipmakers, and Micron, given its role in supplying HBM, stands to benefit. This, however, is contingent upon Nvidia’s continued success, and the fate of Micron is, therefore, inextricably linked to the fortunes of a single, powerful corporation.

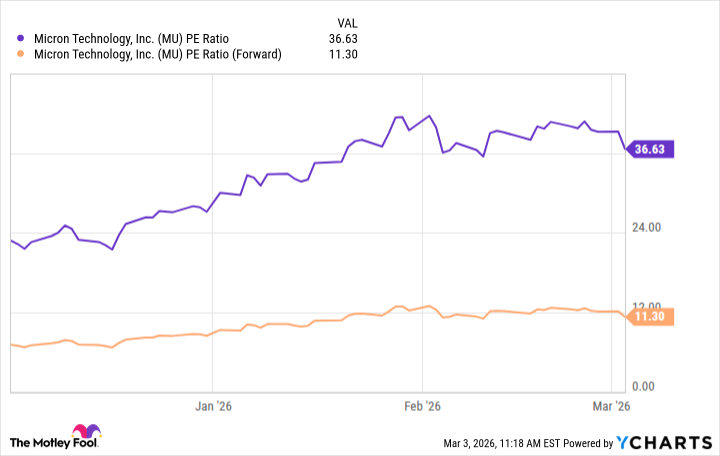

Micron’s trailing twelve-month earnings of $10.52 per share place its stock at a price-to-earnings (P/E) ratio of 36.6, roughly in line with Nvidia’s. From this perspective, the stock appears fairly valued. However, Wall Street’s consensus estimate suggests full-year fiscal 2026 earnings of $34.16 per share, placing the stock at a forward P/E ratio of just 11.3. A discrepancy that feels, upon closer inspection, less like an opportunity and more like a warning.

To maintain its current P/E ratio of 36.6, the stock would have to increase by 223% over the next six months. A scenario that feels, upon closer inspection, less like a realistic possibility and more like a delusion. There are, inevitably, risks on the horizon. OpenAI, for example, has recently reduced its planned infrastructure spending. If this becomes a widespread phenomenon, Huang’s forecast may prove overly optimistic.

Nevertheless, there is room for upside in Micron’s stock. It may not triple over the next six months, but it is unlikely to decline significantly. The future, however, remains uncertain, and the fate of Micron, like the fate of all things, is ultimately beyond our control.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Gold Rate Forecast

- Spotting the Loops in Autonomous Systems

- Silver Rate Forecast

- The 10 Most Underrated Jim Carrey Movies, Ranked (From Least to Most Underrated)

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- The Best Directors of 2025

2026-03-08 01:42