![]()

The recent performance of Micron Technology, with its considerable gains, is less a testament to ingenuity than to the predictable rhythms of a cyclical industry. The company prepares to report its quarterly figures on March 18th, and the market, as is its habit, anticipates further escalation. The underlying cause is not miraculous, but a simple imbalance: demand for memory chips exceeding supply. A temporary condition, to be sure, but one which currently sustains inflated prices and encourages speculation.

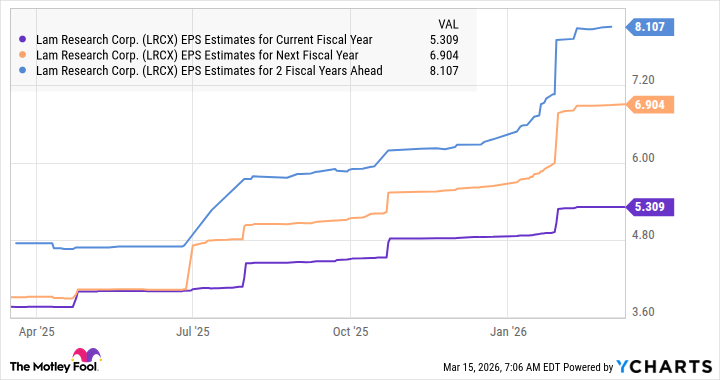

However, to focus solely on Micron is to mistake the symptom for the cause. The true beneficiary of this present surge is not the manufacturer of memory itself, but the provider of the machinery which makes it possible. Lam Research, a name less familiar to the casual investor, stands to gain considerably from the current climate. Its recent increase in share value – a rise of 81% in six months – is a more reliable indicator of the industry’s direction than the volatile price of memory chips.

Lam Research: The Engine of Expansion

Lam Research’s business is not in the creation of memory, but in the tools used to make memory. Approximately 34% of its revenue derives from the provision of equipment for this purpose. The company reported record revenue from the sale of DRAM manufacturing equipment, driven by a surge in demand for High-Bandwidth Memory (HBM). HBM, it is claimed, is essential for the functioning of artificial intelligence data centers, allowing for the rapid processing of vast quantities of data. This, of course, is the current mantra, and one should approach such pronouncements with a degree of skepticism.

Bank of America projects a 58% increase in the HBM market this year, reaching almost $55 billion. Micron itself anticipates $100 billion in revenue by 2028. Such figures are presented as evidence of unstoppable growth, but they mask a fundamental truth: the prioritization of certain markets over others. The demand for HBM is, in effect, diverting resources from the production of memory for more commonplace applications – smartphones and personal computers. This is not a failure of supply, but a deliberate allocation of it.

The consequence of this prioritization is predictable: higher prices for consumers and a potential slowdown in the sales of everyday electronics. HBM requires significantly more wafer capacity than traditional DRAM, and manufacturers are understandably focusing on the more lucrative data center market. This is not a matter of technological progress, but of simple economics. The pursuit of profit, as always, dictates the flow of resources.

Micron has announced a planned increase in capital expenditure – a rise to $20 billion – to expand its HBM capacity. Samsung and SK Hynix are following suit. This investment, while presented as a response to demand, is also a means of solidifying market position and ensuring future profitability. It is a game of capital, played by a few powerful players.

The Machinery of Growth

Lam Research’s recent earnings reflect this dynamic. In the quarter ending December 2025, earnings jumped by almost 40% year-over-year. Revenue increased by 22%. The company appears well-positioned to exceed analyst expectations. This is not a matter of luck, but of being in the right place at the right time – or, more accurately, of providing the tools that enable others to be in the right place.

Analysts are, predictably, bullish about Lam Research’s prospects. They anticipate further earnings growth, driven by increased investment in manufacturing capacity. This is a self-fulfilling prophecy, fueled by optimism and the desire for short-term gains. The long-term consequences, as always, are less certain.

McKinsey estimates that semiconductor companies will invest a staggering $1 trillion in new fabrication plants through 2030. Lam Research, with 59% of its revenue derived from equipment sales to foundries such as Taiwan Semiconductor Manufacturing, Intel, and Samsung, is poised to benefit from this expansion. This is not a revolution, but a continuation of the established pattern: the relentless pursuit of efficiency and profit, masked by the rhetoric of innovation.

Lam Research, therefore, appears to be a relatively safe investment, at least in the short term. It is a company that provides the essential infrastructure for the semiconductor industry, and it is well-positioned to capitalize on the current wave of investment. However, one should remember that all cycles eventually turn. The current boom will not last forever, and those who profit from it today may face challenges tomorrow. The history of industry is littered with the wreckage of companies that failed to adapt to changing circumstances.

Read More

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Silver Rate Forecast

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 15 Films That Were Shot Entirely on Phones

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

- ONE PIECE Season 2 Confirms Sanji’s OTHER Backstory in the Live-Action

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- Top 10 Coolest Things About Jared Leto

2026-03-18 17:03