Right then. Let’s talk about Marvell Technology. Not because it sounds like a particularly enthusiastic comic book hero, but because it’s currently building the digital plumbing for the coming age of… well, let’s call it ‘Intelligent Dust’.1 That is to say, Artificial Intelligence. Everyone’s building it, of course. The Guild of Alchemists – or, as they’re known in less fanciful circles, ‘Hyperscalers’ – are throwing mountains of gold at it. Alphabet, Amazon, Meta, Microsoft… they’re all vying to be the first to build a truly self-aware server farm.2 And that, my friends, requires chips. Lots and lots of chips.

The current projections suggest these Alchemists will collectively spend some $650 billion this year on the infrastructure. That’s a figure that makes even the most seasoned accountant reach for the smelling salts. Last year it was ‘only’ $410 billion. Not that ‘only’ applies to sums that could fund a small kingdom. OpenAI and Anthropic are also getting in on the act, as are newer players like CoreWeave and Nebius, all desperate to build more and more ‘compute capacity’ – a phrase that sounds suspiciously like hoarding magical energy. It’s a bit like a dragon collecting gold, really. Except the gold is silicon, and the dragon is a data center.

Which brings us back to Marvell. They don’t quite forge the dragon’s scales, but they do design a good portion of the intricate workings inside. Custom AI processors and networking chips, you see. The sort of thing that makes the whole ‘intelligent dust’ operation actually, well, operate. And they’re doing rather well out of it. Not that ‘rather well’ quite captures the magnitude. Their latest quarterly results show a 42% jump in revenue, hitting $8.2 billion. Earnings are up 81% to $2.84 per share. These aren’t the numbers of a company merely surviving; they’re the numbers of a company actively thriving in the digital age.

Marvell Technology: Clocking Outstanding Growth Thanks to AI

The real engine of this growth is their data center business, which has surged by 46% to over $6 billion. Demand for their data center interconnects, switching, storage, and custom chips is, shall we say, enthusiastic. Particularly those custom processors. It appears the Alchemists have realized that off-the-shelf components simply won’t do when you’re trying to coax sentience out of a pile of sand.3

Bloomberg reports that Marvell is designing these custom processors for Amazon and Microsoft, and they’re expected to capture a significant chunk of the market – 20% to 25% in the long run. That’s up from less than 5% in 2023. They plan to do this by securing more business from the big four Alchemists and, crucially, by attracting the attention of the newer cloud infrastructure companies. Marvell’s management anticipates a 40% spike in data center revenue next year and an overall revenue growth of 34% to $11 billion. They’re talking about $15 billion in revenue the year after that, fueled by over 20 new chip designs. It’s a bold claim, but in this business, boldness is often rewarded.

Counterpoint Research suggests the market for these application-specific integrated circuits (ASICs) will triple between now and 2027. That’s a lot of chips. And a lot of potential profit. Analysts are starting to take notice, and their projections are becoming increasingly bullish. Add in a relatively attractive valuation, and you have a stock that looks poised for some serious gains.

Why the Stock Seems Primed for a 50% Jump in 2026

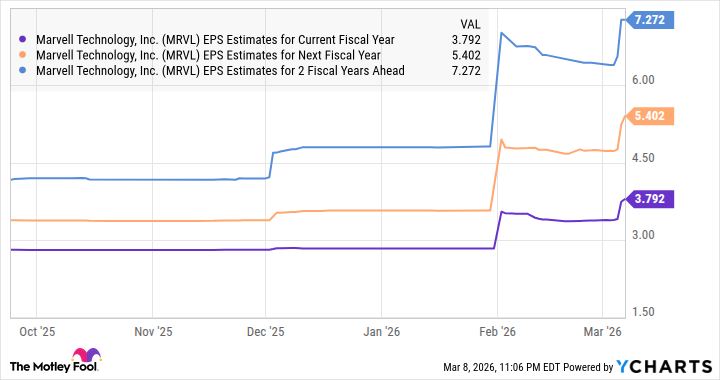

Let’s assume you have $10,000 burning a hole in your pocket, after paying the bills, saving for a rainy day, and settling any outstanding debts. You’re looking for a growth stock to add to your portfolio. Marvell could be a smart move. Analysts predict a 33% increase in earnings this year, to $3.79 per share, followed by a stronger 42% jump next year. If Marvell manages to hit those targets and trades at a multiple of 39 – the average for the US tech sector – the stock could jump to $148. That’s a potential 66% increase from current levels. So, yes, this AI stock could indeed turn $10,000 into at least $15,000 by 2026. And with the continued earnings growth expected over the next few years, there’s potential for even greater upside.

Now, I’m not saying it’s a sure thing. Nothing ever is. But in a world increasingly reliant on ‘intelligent dust’, a company that builds the tools to make it work is a pretty good place to be. It’s a bit like investing in pickaxes during a gold rush. Except the gold is data, and the pickaxes are… well, you get the idea.

1 ‘Intelligent Dust’ is, of course, a metaphor. Although, one does wonder what would happen if you did manage to imbue dust with sentience. It would probably demand better working conditions.

2 The Alchemists, naturally, deny any intention of creating artificial sentience. They claim they’re merely building ‘more efficient data processing systems’. But then again, they would, wouldn’t they?

3 The inherent irony of building machines to simulate intelligence while simultaneously ignoring the intelligence of those building them is not lost on me.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Top 20 Dinosaur Movies, Ranked

- Silver Rate Forecast

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- Gold Rate Forecast

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

2026-03-13 16:24