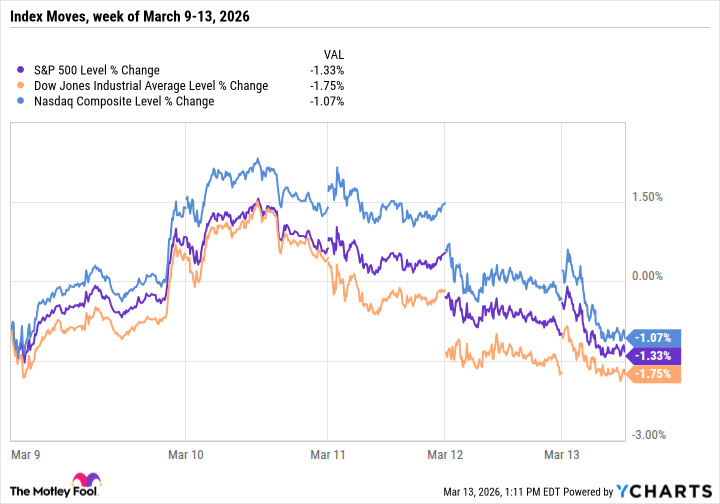

The indices, as they are permitted to be called, have concluded the week in a state of diminished vitality. A momentary elevation on Monday and Tuesday, predicated on the naive assumption of a swift resolution to the disturbances in the region, proved illusory. The conflict, rather than abating, has metastasized, culminating in a restriction of maritime traffic through the Strait, a constriction which, predictably, has induced a corresponding inflation in the price of crude oil. It is a familiar pattern, one observed with a weary inevitability.

This is, of course, unwelcome news, particularly when one considers the insatiable appetite of the data repositories – the so-called AI centers – for electrical power. These structures, monuments to an abstract progress, consume energy at a rate that is, in itself, a source of quiet desperation, often relying on the combustion of the very resources now subject to increased cost. The confluence of demand and limitation raises questions – not of policy, or of economic theory, but of the fundamental order of things. The effect, naturally, extends to all sectors, from the manufacturers of commonplace goods to the custodians of wealth. The energy producers, predictably, benefit, a minor alleviation in a larger, inescapable decline.

The Illusion of Sectoral Strength

As was to be anticipated, the majority of indices have descended into a state of lower valuation. The energy sector, operating with limited exposure to the immediate geographic instability, has experienced a degree of elevation. However, this is merely a localized phenomenon, insufficient to counterbalance the broader, systemic pressures. It is as if a single, flickering candle were to be expected to illuminate a vast, encroaching darkness.

The energy sector, one notes, constitutes a mere 3.4% of the total market capitalization of the S&P 500 (^GSPC 0.55%). Its presence on the Nasdaq Composite (^IXIC 0.97%) is even more negligible, accounting for a scant 1%. The Dow Jones Industrial Average (^DJI 0.15%) is burdened, or perhaps merely accompanied, by a single energy concern, Chevron (CVX 0.37%), whose influence, despite its considerable size, is constrained by the index’s weighting methodology. Even a substantial appreciation in Chevron’s valuation would barely register on the overall calculation. The mechanisms, one observes, are designed to absorb, to dilute, to render inconsequential.

The Descent of the Designated Leaders

The valuation of the Dow has been impacted by a decline in the price of Goldman Sachs (GS 0.66%) and Home Depot (HD +0.15%). The S&P 500 and Nasdaq Composite have followed suit, guided by the performance of a select group of entities – the so-called Magnificent Seven – each experiencing a diminution of market capitalization exceeding one hundred billion units of currency. It is a predictable unraveling, a slow erosion of perceived value.

Amazon (AMZN 1.32%) has been particularly affected, its market capitalization shrinking by a considerable sum. This is directly attributable to its investment in data centers, a commitment that necessitates ever-increasing consumption of electrical power. The connection, though obvious, is rarely acknowledged. The logic of the system demands a perpetual expansion, regardless of the consequences.

The disturbances in the region will likely continue to exert a controlling influence on market sentiment. It does not yet constitute a bear market, merely a protracted period of diminished returns. The indices remain within a relatively narrow range of their recent peaks, the declines remaining below the two percent threshold. However, the storm clouds are gathering, centered around the Strait of Hormuz. It is premature to issue warnings, but a degree of preparedness is advisable. One should not anticipate a swift resolution, merely a continuation of the prevailing uncertainty. The system, after all, is designed to perpetuate itself, regardless of the external pressures.

Read More

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Celebs Who Narrowly Escaped The 9/11 Attacks

- Transformers Under the Microscope: What Graph Neural Networks Reveal

- Top 20 Dinosaur Movies, Ranked

- Trading on Thin Air: AI Agents Conquer Crypto Volatility

- Silver Rate Forecast

- Gold Rate Forecast

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Every Notable ‘Star Trek: The Original Series’ Actor Who Died

2026-03-13 21:02