They say eighty percent of Americans are worried about a recession. Eighty percent. Which, statistically, means my Aunt Mildred, who stockpiles canned peaches and believes pigeons are government drones, is probably in that number. And honestly, good for her. Someone needs to be prepared. I, myself, mostly just feel a low-grade, persistent dread, like I’ve forgotten to turn off the iron, but on a national economic scale.

The financial news keeps mentioning something called the “Shiller CAPE Ratio,” which sounds less like an indicator of economic health and more like a cocktail I’d accidentally order at a particularly pretentious bar. Apparently, it’s high. Very high. Which, if I understand correctly (and I rarely do), means things are…overvalued. It reminded me of the time I bought a ceramic cat for $45 at a flea market, convinced it was a rare collectible. It wasn’t. It was just a ceramic cat.

Everyone keeps saying “past performance doesn’t predict future returns.” Which is true, of course. But it’s also the kind of thing people say right before everything goes horribly wrong. Like a flight attendant cheerfully announcing, “Turbulence is possible, but statistically unlikely!” I’m not sure that makes me feel better. I’m also fairly certain that statistics have a personal vendetta against me.

A Long-Term Strategy (Or, How to Avoid My Aunt Mildred’s Peach Collection)

My portfolio, such as it is, will almost certainly lose value if stock prices decide to take a nosedive. It’s just the natural order of things. But staying invested, they say, is the key. The problem is, my attention span is roughly equivalent to that of a goldfish. I find myself checking the market every fifteen minutes, which is about as helpful as trying to bail out the ocean with a teaspoon. My therapist suggests mindfulness. She doesn’t understand the allure of panic-selling.

Apparently, since 1929, bear markets last around 286 days. Just under 9.5 months. Bull markets, however, last over 1,000 days. Nearly three years. Which means, statistically, I’ll be miserable for a shorter period of time than I’m successful. That’s…comforting, in a deeply unsettling way.

The experts say if you panic-sell, you lock in losses. Which feels intuitively correct, but also assumes I have the discipline to resist the urge to throw my money at something, anything, that promises immediate relief. Like a timeshare in Florida.

History, Repeating Itself (And My Bad Decisions)

They say the market always recovers. Always. Which is a lovely thought. But it doesn’t account for the emotional toll of watching your savings dwindle. It’s like being on a diet and constantly surrounded by cupcakes. Eventually, you break.

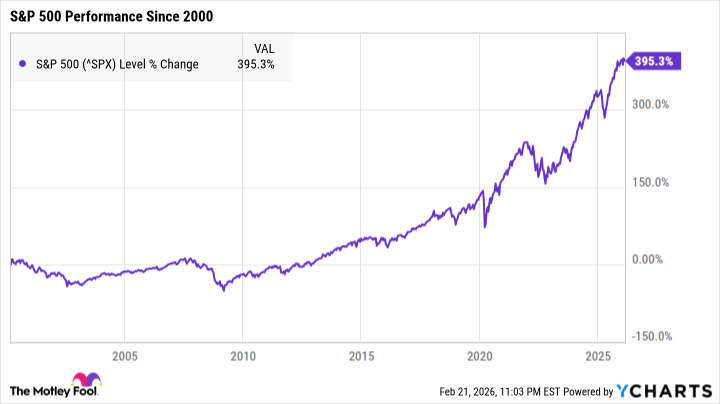

The S&P 500 is up 45% since January 2022. And up 400% since the dot-com bubble burst. Which is impressive, I suppose. But it also highlights my own consistent inability to time the market. I bought high in 2008. And again in 2017. I’m a trendsetter, but not in a good way.

Nothing is guaranteed in the stock market. Which is a profoundly depressing thought. But it’s also true. So, if there’s one thing I’m going to do, it’s stay invested. Even when every fiber of my being tells me to run screaming into the wilderness. Because honestly, that wilderness probably has a better return on investment right now.

The longer you keep your money in the market, the better your chances of earning a positive return. That, and maybe avoiding eye contact with my Aunt Mildred. She’s starting to look at my canned goods with suspicion.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Trading Crypto with AI: A New Approach to Portfolio Management

- Silver Rate Forecast

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- Thinking Before Acting: A Self-Reflective AI for Safer Autonomous Driving

2026-02-24 11:03