The noble cryptocurrency, Bitcoin, has once again dipped beneath the $90K threshold, and lo! Two of its most ardent admirers-MSTR and MARA-teeter on the brink of a fiscal calamity so dire, it would make Jeeves weep into his teacup.

Beyond MSTR’s Woes: Vaneck Analyst Flags Greater Peril at MARA

At first blush, treasury company Strategy (Nasdaq: MSTR) and mining firm Mara Holdings (Nasdaq: MARA) appear as twin peas in a cosmic pod. Both are revered names in the bitcoin community, hoarding BTC like Scrooge McDuck in a crypto-themed vault. Strategy, however, possesses tenfold the BTC of its rival, yet both employ the same strategy: hoarding the digital coin to maximize yield. But according to Vaneck’s Head of Digital Assets Research, Matthew Sigel, Mara’s financial acrobatics are far more precarious than a penguin on roller skates.

“MSTR and MARA are worth comparing because both are down ~50%+ in the last 6 weeks,” Sigel wrote on Thursday. “MARA appears extremely cheap with unusually high short interest. But dig deeper and the picture changes quickly.”

What Sigel alludes to is the difference in debt structure between the two companies. Back in August 2020, Strategy had an enormous pile of surplus cash. Chairman Michael Saylor, in a moment of inspired folly, decided to buy bitcoin, believing it would yield a higher return than traditional assets. Strategy eventually pivoted from developing business intelligence software to accumulating bitcoin, becoming the largest corporate holder of the cryptocurrency. One approach the company employed was issuing convertible debt to purchase bitcoin. The tactic was so successful that a slew of other companies followed suit, including Mara.

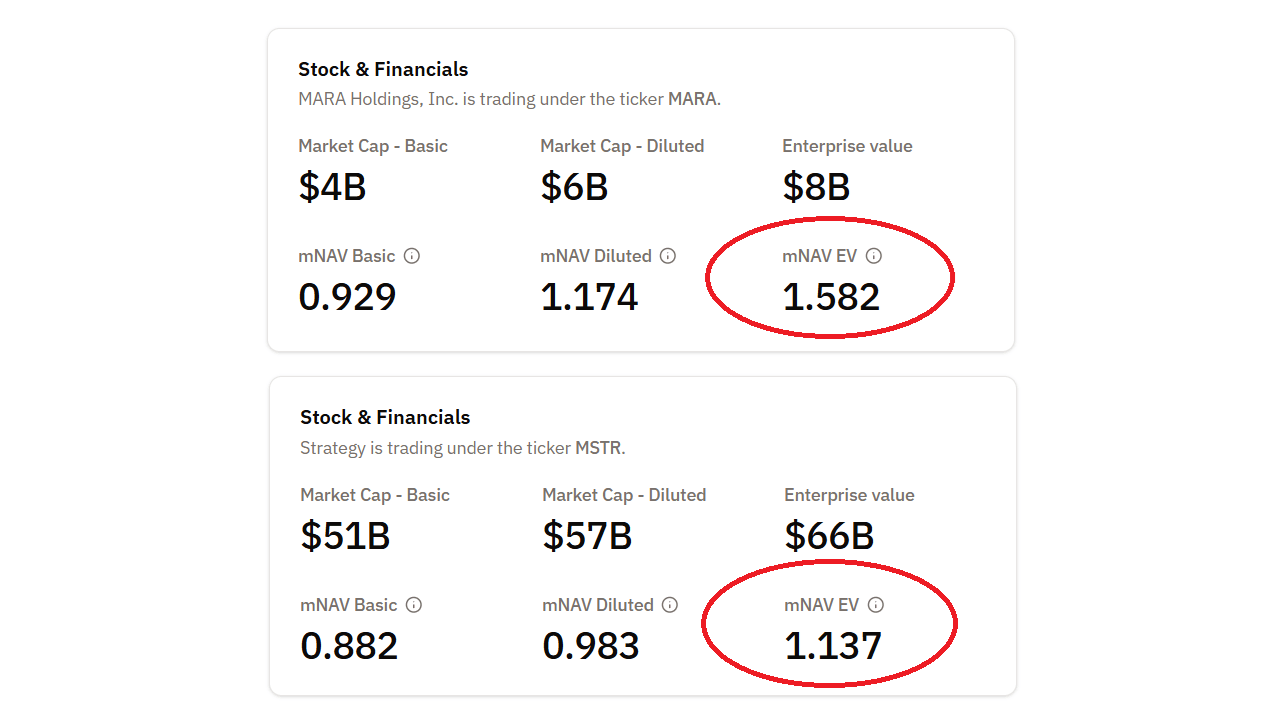

The mining firm has now issued approximately $3.3 billion in convertible bonds, according to its latest financials. This didn’t raise any alarm bells when bitcoin was rallying, but at $88K, things are starting to get a little shaky. Share price has fallen by about 50% as Sigel noted. But that doesn’t make Mara a cheap buy because its enterprise value has ballooned, thanks to the billions owed in debt. Those outstanding bonds have jacked up Mara’s mNAV, a metric that tracks enterprise value relative to the value of a company’s bitcoin holdings. In other words, investors are paying way more for Mara stock than can be justified by its BTC stash.

“MARA only screens inexpensive if you ignore its $3.3B face value of convertible debt,” says Sigel. “It’s trading at a premium once debt is included.”

To be clear, Strategy is also trading at a premium, but a much smaller one. Bitcointreasuries.net shows Mara’s mNAV at 1.59 while MSTR’s is at 1.14. Bitcoin’s shenanigans over the past few weeks have placed both firms in a precarious position. But Mara has a messier debt structure that clouds the correlation between its stock price and the value of bitcoin. And despite the current hullabaloo around Strategy’s finances, Sigel says more people should be worried about Mara.

“MARA is up 30% from the lows and running into resistance so I sold some today and added to MSTR,” Sigel said.

Overview of Market Metrics

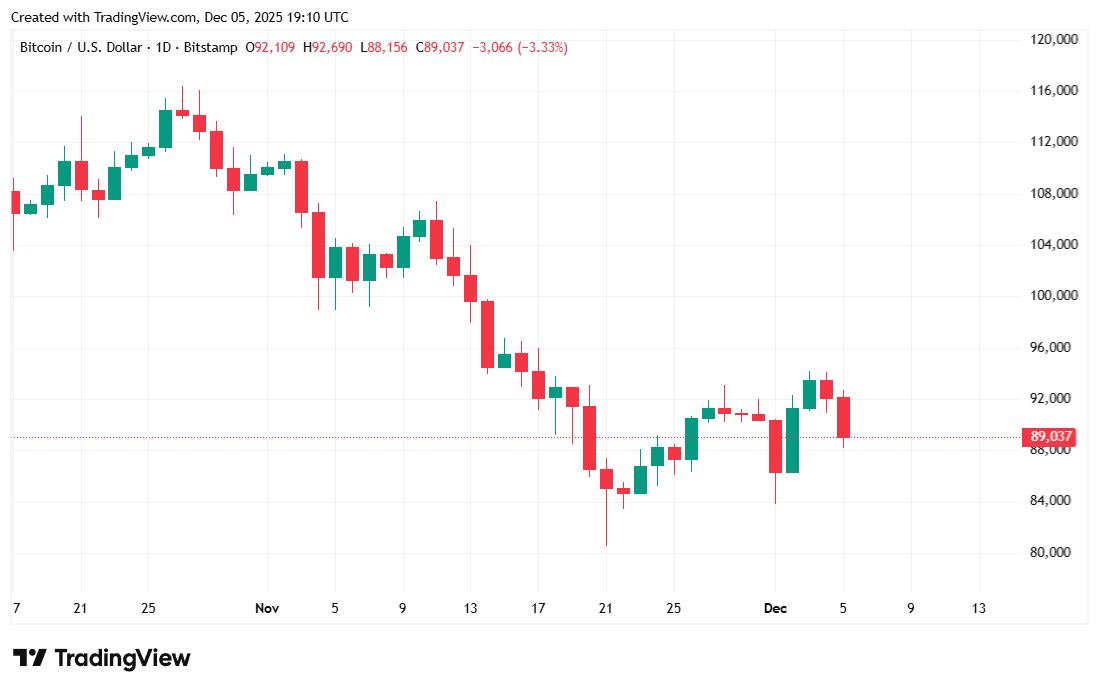

Bitcoin was priced at $89,018.14 at the time of writing, down 3.14% from yesterday’s price and also down 1.96% over seven days, according to Coinmarketcap data. The digital asset’s price fluctuated between $88,152.14 and $92,707.20 over the past 24 hours.

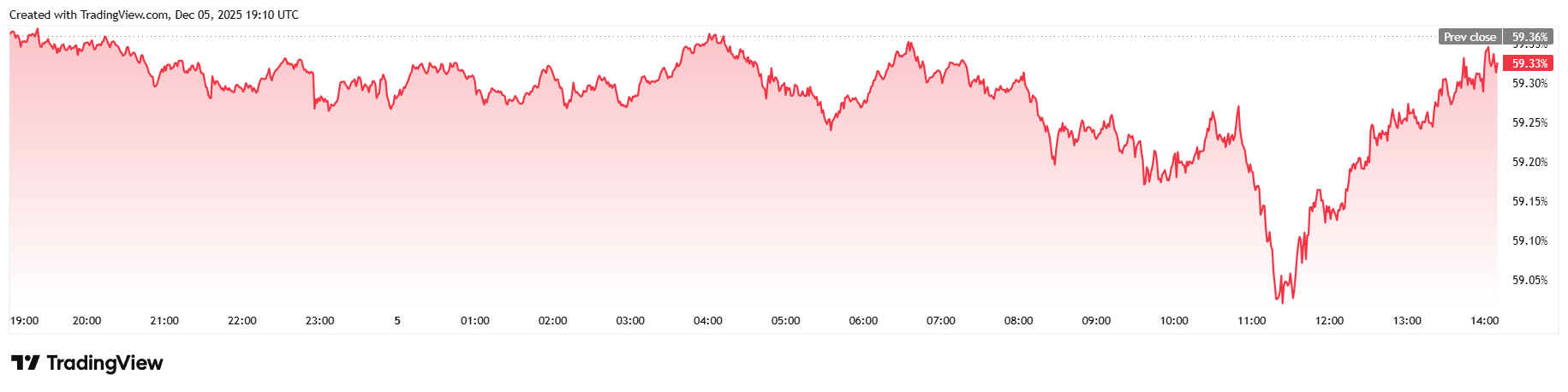

Daily trading volume was down 2.04% at $64.18 billion and market capitalization eased to $1.77 trillion. Bitcoin dominance edged lower, shedding 0.07% to reach 59.33%.

Total bitcoin futures open interest fell 3.88% to $57.40 billion, according to data from Coinglass. Total liquidations doubled over 24 hours and stood at $192.56 million at the time of reporting. Long investors dominated that amount with $170.76 million in liquidated margin. Short sellers were largely spared and only saw $21.79 million wiped out.

FAQ ⚡

- Why does VanEck’s Matthew Sigel think MARA is in worse trouble than MSTR?

Sigel argues that MARA’s $3.3B in convertible debt makes the company far riskier than it appears, especially with bitcoin now under $90K. A financial quagmire, one might say! - How does MARA’s debt affect its valuation compared to its bitcoin holdings?

Once its massive debt load is included, MARA trades at a steep premium to the value of its BTC, making it far more expensive than headline numbers suggest. A masterclass in misdirection! - Why is MSTR considered a cleaner bet on bitcoin than MARA?

MSTR holds more BTC with a simpler capital structure, giving it a higher correlation to bitcoin and fewer distortions from leverage. Simplicity, thy name is MSTR! 🎩 - What does Sigel recommend based on current market conditions?

Sigel says he is reducing exposure to MARA and adding to MSTR, calling MARA’s rally “resistance” and warning that its risks are underappreciated. A prudent move, or a ploy to confuse the masses? Only time will tell. 🕵️♂️

Read More

- Gold Rate Forecast

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- 15 Films That Were Shot Entirely on Phones

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Brent Oil Forecast

- New HELLRAISER Video Game Brings Back Clive Barker and Original Pinhead, Doug Bradley

- Superman Flops Financially: $350M Budget, Still No Profit (Scoop Confirmed)

- 14 Movies Where the Black Character Refuses to Save the White Protagonist

2025-12-06 00:45