Lemonade, they call it. A curious name for a venture attempting to tame the anxieties of modern life. It is not merely an insurer, but a proposition – a belief that the cold logic of algorithms can, in fact, offer a warmer hand to those seeking shelter from life’s inevitable storms. The company, barely a decade old, aims to disrupt the established order, to replace the ponderous bureaucracy of traditional insurance with the swift currents of artificial intelligence. Five offerings, they present – car, renter’s, homeowner’s, life, and pet – a modest portfolio, yet one that has already garnered the attention of nearly three million souls.

They speak of a tenfold increase in ‘in-force premium’ over the coming decade. A bold ambition, certainly. One might ask if such exponential growth is truly sustainable, or merely a phantom bloom in the springtime of venture capital. Yet, the numbers themselves are compelling. A surge in premium, a swelling tide of policyholders. It is not simply about scale, though that is undoubtedly a factor. It is about a shift in perception, a willingness to entrust one’s security to a system that prioritizes efficiency and transparency.

The market, fickle as ever, has recently cast a shadow upon Lemonade’s shares. A decline of twenty-four percent, they report. A momentary setback, perhaps, or a more profound reckoning. For the discerning investor, however, it presents an opportunity. A chance to acquire a share in this unfolding experiment for under sixty dollars. The question, as always, is whether this is a seed that will take root and flourish, or a fleeting blossom destined to wither in the algorithmic wind.

The Future Whispered in Code

The experience begins with Maya, an AI companion who crafts insurance quotes in a matter of seconds. A swiftness unheard of in the old world. And then there is Jim, who processes claims with a similar velocity, dispensing with the endless delays and frustrating phone calls that have long been the hallmarks of the industry. It is a seductive promise – instant gratification in a realm where patience has traditionally been a virtue. One wonders if this efficiency comes at a cost, if the human touch is being sacrificed at the altar of automation.

The numbers speak for themselves. Nearly three million policyholders at year’s end, a twenty-three percent increase. A surge in ‘in-force premium’ of thirty-one percent, the growth accelerating with each passing quarter. They are not merely adding customers; they are reshaping the landscape. And they are doing so with a lean operation, reducing their workforce by six percent while simultaneously expanding their reach. It is a testament to the power of automation, a glimpse into a future where machines handle the mundane, freeing up humans to focus on more complex tasks.

Behind the scenes, AI is employed to calculate risk, to ensure that premiums are accurate and fair. It is a subtle but significant shift, a move away from the opaque pricing models of the past. And the results are striking. Their loss adjustment expense ratio stands at a mere six percent, significantly lower than the industry average of nine percent. They are operating with a level of efficiency that few of their competitors can match.

A Revenue Current, Swift and Strong

Their gross loss ratio, a measure of claims paid out as a percentage of premiums received, stands at sixty-four percent. They believe that seventy-five percent represents the sweet spot for a thriving insurance business, and they are comfortably ahead of that mark. A declining loss ratio, combined with a growing ‘in-force premium,’ creates a virtuous cycle, generating more revenue and allowing for further investment.

In 2025, they reported a record revenue of $738 million, a forty percent increase from the previous year. A figure that exceeded even their own optimistic forecasts, which had already been revised upwards three times throughout the year. It is a remarkable achievement, a testament to the power of their innovative approach. One cannot help but wonder if this growth is sustainable, or if it is merely a temporary surge fueled by novelty and hype.

Their losses, while still substantial at $165.5 million, have been reduced by eighteen percent. They continue to invest aggressively in growth initiatives, a strategy that is justified as long as their ‘in-force premium’ continues to accelerate. The hope, of course, is that once they achieve sufficient scale, they will be able to rein in their operating costs and allow profits to flow more freely.

A Seed Worth Nurturing?

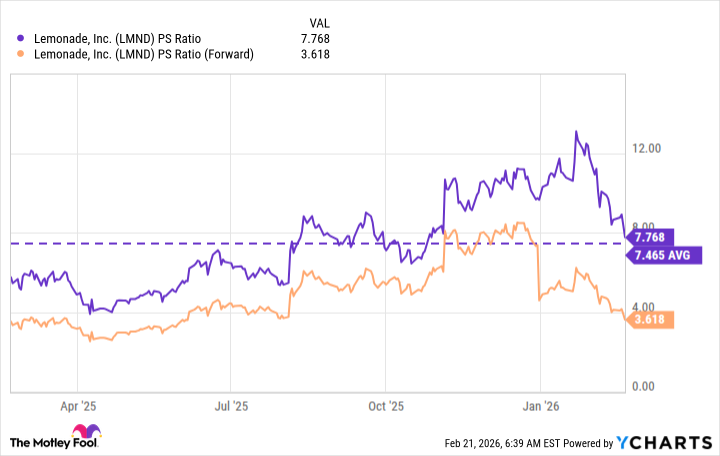

Their price-to-sales ratio peaked at thirteen last year, but the recent decline in their stock, combined with their surging revenue growth, has brought it down to seven-point-seven. A more attractive valuation, certainly. But the true potential lies in their future earnings. Management’s guidance suggests that revenue will soar by sixty-one percent in 2026, reaching $1.19 billion. This would bring their forward price-to-sales ratio down to a mere three-point-six. A compelling argument for investment, if one believes in their long-term vision.

If they deliver on that guidance, their stock is likely to end the year significantly higher than it is today. But the real rewards may come in the long term, as they aim to grow their ‘in-force premium’ to $10 billion over the next decade by expanding into high-value segments like car insurance. It is an ambitious goal, but one that, if achieved, could reshape the insurance landscape and deliver substantial returns to investors. Whether this seed will truly blossom, only time will tell. But in a world increasingly defined by algorithms and automation, Lemonade represents a fascinating experiment, a glimpse into a future where insurance is not merely a necessity, but a seamless, intelligent, and perhaps even… pleasant experience.

Read More

- Invincible Season 4 Gender Swaps Tech Jacket As Fans Question Major Comic Change

- Building Agents That Learn and Improve Themselves

- Gold Rate Forecast

- Silver Rate Forecast

- Games That Faced Bans in Countries Over Political Themes

- Trading Crypto with AI: A New Approach to Portfolio Management

- 15 Films That Were Shot Entirely on Phones

- Why Won’t It Just *Do* What You Ask? Unpacking the Quirks of AI Language

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- Unveiling the Schwab U.S. Dividend Equity ETF: A Portent of Financial Growth

2026-02-24 17:12